Download to read offline

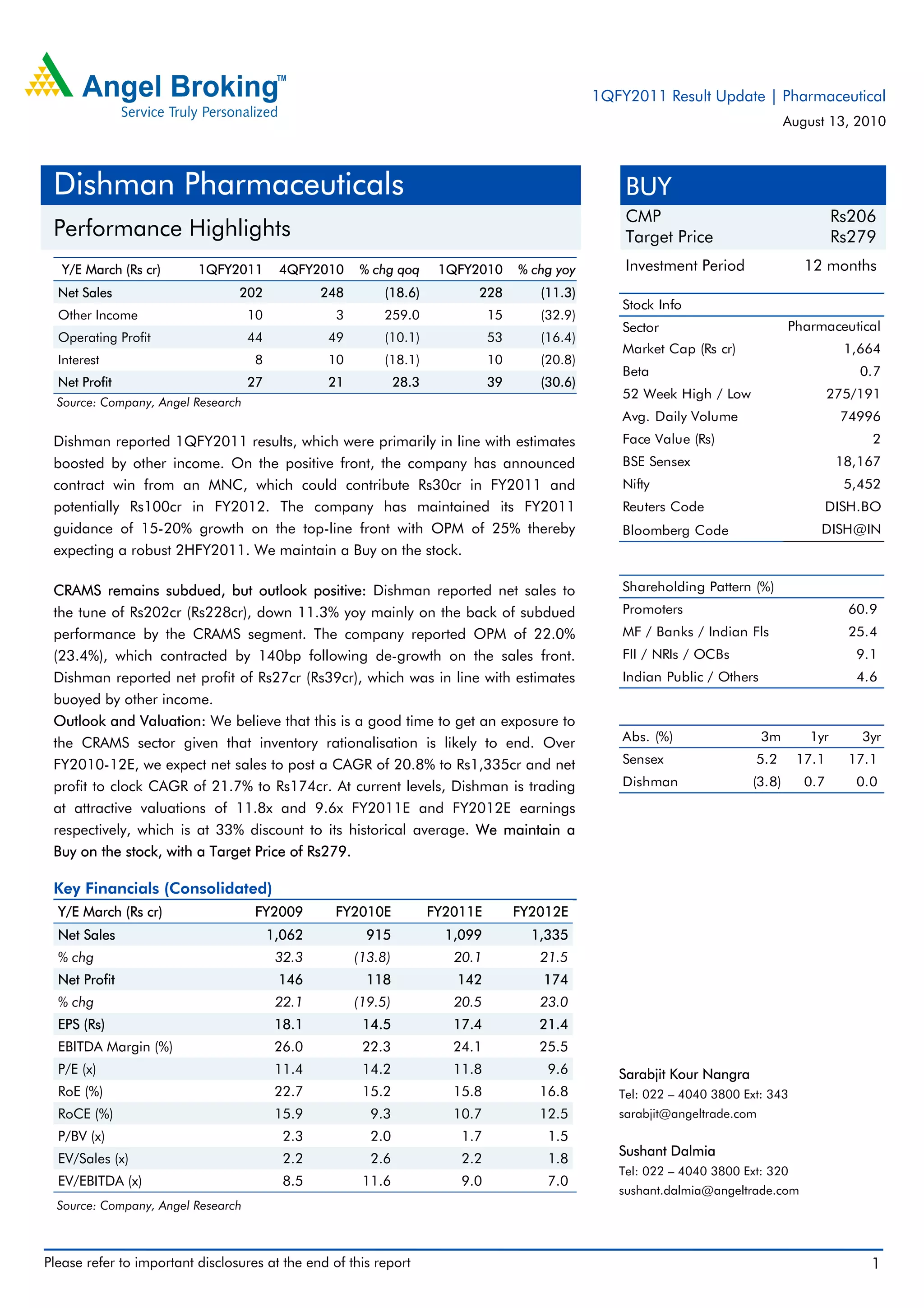

- Dishman reported 1QFY2011 results which were primarily in line with estimates, boosted by higher other income. Net sales were down 11.3% YoY due to subdued CRAMS segment performance. - Operating profit margin contracted 140bps to 22% due to sales de-growth. However, net profit was maintained due to higher other income. - The company maintained FY2011 guidance of 15-20% top-line growth and 25% operating margin, expecting a robust second half of FY2011.