Kaizen

•Download as PPT, PDF•

2 likes•387 views

This document contains a summary of a Kaizen sheet from a manufacturing plant. The Kaizen sheet describes a problem where two workers were engaged cleaning oil from center bolt cut lengths using saw dust, creating waste. The countermeasure was to use wet cotton waste instead of excess oil flow to reduce oil and eliminate saw dust cleaning, saving over Rs. 77,000 per year in expenses. The implementation was successful in eliminating the saw dust cleaning process. The document provides details on expenses before and savings achieved after the countermeasure.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Kaizen

Similar to Kaizen (20)

More from Jitesh Gaurav

More from Jitesh Gaurav (20)

Recently uploaded

Recently uploaded (20)

Kaizen

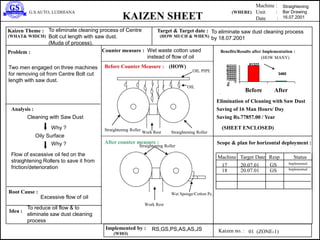

- 1. Straightening Bar Drawing 16.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Two men engaged on three machines for removing oil from Centre Bolt cut length with saw dust. To eliminate cleaning process of Centre Bolt cut length with saw dust. (Muda of process). Oily Surface Flow of excessive oil fed on the straightening Rollers to save it from friction/deterioration Why ? Why ? 3465 81322 0 1000020000 30000 40000 5000060000 70000 80000 Before After Rs. Cleaning with Saw Dust Wet waste cotton used instead of flow of oil Excessive flow of oil To reduce oil flow & to eliminate saw dust cleaning process StatusMachine Target Date Resp RS,GS,PS,AS,AS,JS To eliminate saw dust cleaning process by 18.07.2001 01 (ZONE-1) . OIL PIPE OIL Straightening Roller Straightening RollerWork Rest Straightening Roller Wet Sponge/Cotton Pc. Work Rest Elimination of Cleaning with Saw Dust Saving of 16 Man Hours/ Day Saving Rs.77857.00 / Year (SHEET ENCLOSED) 17 18 20.07.01 20.07.01 GS Implemented ImplementedGS

- 2. BEFORE 1. OIL (DIESEL) CONSUMPTION / DAY : 5 LITRES PRICE / LITRE (RS.) : Rs.16.66 COST OF OIL/DAY (16.66 x5) : Rs. 83.30 COST OF OIL/MONTH (83.30 x26) : Rs. 2165.80 COST OIL OIL / YEAR (2165.80 x12) : Rs.25989.60 2. SALARY OF 2 PERSONS/ YEAR : Rs.48000.00 3. SAW DUST CONSUMPTION / DAY : 23.3 KGS SAW DUST COST/BAG : Rs.21.00 MONTHLY EXPENSES OF SAW DUST (21.00x26) : Rs.546.00 YEARLY SAW DUST EXPENSES (546.00x12) : Rs. 6552.00 4. MONTHLY ELECTRICITY EXPENSES : Rs.65.00 YEARLY ELECTRICITY EXPENSES : Rs. 780.00 TOTAL EXPENSES PER YEAR (25989.60 + 48000+6552+780) : Rs. 81322.00 AFTER YEARLY EXPENSES OF OIL (0.7 LTR/DAY x26 x 12) : Rs. 3465.00 TOTAL SAVING/YEAR (81322.00 -3465.00) : Rs. 77857.00 ANNEXURE: KAIZEN-1

- 3. Facing M/Cs BRD 01.08.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Extra movement of Facing Operators To eliminate the movement of operator at Centre Bolt cut length facing machines (Muda of movement & Muri) Distance between facing & Straightening M/c was 14’ & 11’ respectively Why ? 0 386 0 100 200 300 400 Before After Operator goes to Straightening M/c to pick up cut length for facing (80 times in a day) 2 Facing machines shifted near Straightening M/Cs Improper Layout To eliminate Muda of Movement & Muri StatusMachine Target Date Resp GS, AK, PS, AS To eliminate operator movement & Muda before 07.08.2001 03 (ZONE-1) 01 03 02 01 02 03 Straightening Machines Facing M/Cs 14 Feet 5 Feet 11 Feet Tray Facing M/Cs Straightening M/Cs 01 02 03 01 02 03 3 Feet 5 Feet 3 Feet Operator Movement :386 Km/Year Man Hours Saved (386/5) : 77 Hours Wages saved / Hour : Rs. 10.00 Wages/Year (77x10) : Rs. 770.00 (Total cost reduction) Operator Fatique Reduced Why ? Improper Layout Picking & operation within operator’s arm distance

- 4. Facing M/Cs CFG & NT3 07.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Extra movement of Material To reduce Muda Of Transportation from Cold Forging to Nut-3 Sec. Facing & Chamfering M/Cs are not available in Cold Forging Section (M/c Layout constraint) Why ? 1297 5100 0 1000 2000 3000 4000 5000 Before After Material movement from Cold Forging after cutting & One side reducing to Nut-3 for Chamfering & Facing, then again comes back to Cold Forging for 2nd side reducing, then again returned to Nut-3 for stamping & threading Facing M/Cs installed in Cold Forging Section Due to non-availability of facing M/Cs in Cold Forging Section Install S.P.M. Facing machines in Cold Forging Section StatusMachine Target Date Resp AK, GS, PS, AS, JS To reduce material movement by 10.07.01 04 (ZONE-1) Cold Forging Nut-3 Cold Forging Nut-3 Auto Black Packing 195.5 m 195.0 m 195.0 m 154.95 m 94.0 m Total : 834.45 m COLD FORGING AUTO- BLACK PACKING 118.0 M 94.0 M TOTAL : 212.0 M SAVING/YEAR : Rs. 5100.00-1297.00 = 3803.00 (SHEET ENCLOSED)

- 5. ANNEXURE : KAIZEN-04 BEFORE COUNTER MEASURE Distance covered/Day : 834.45 M Distance covered/Year : 2553.4Km (834.45x306 Days) Average distance covered by man/Hr : 5.000 Km Man Hrs(2553.4/5) : 510 Wages/Hour (Rs.) : 10.00 Total Wages/Year : 5100.00 (510Hrs x Rs.10.00) AFTER COUNTER MEASURE Distance covered/Day : 212 M Distance covered/Year 648.72Km (212 M x 306 Days) Average distance covered by man/Hr : 5.000 Km Man Hrs(648.72/5) : 129.74 Wages/Hour (Rs.) : 10.00 Total Wages/Year : 1297.00 (129.7 Hrs x Rs.10.00) SAVING/YEAR : 3803.00

- 6. Hot Bending UBT 02.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Gap controlled manually M/c is not capable to control the gap Why ? Why ? 208320 312480 0 1 0 0 0 0 0 2 0 0 0 0 0 3 0 0 0 0 0 Before After Rs. Material Overheating M/c to be modified by Machine design error To avoid overheating during Bending StatusMachine Target Date Resp BS,JS,RS,BS,DS 30% Electrical Energy saving at Hot Bending process by 30.07.2001 01 (Zone-2) Why ? Machine Design error Saving of Electrical Energy on Hot Bending Process More Electric Energy consumed for Induction Heating the U.Bolts e.g. Rs.26,040.00/ Month providing taper attachment to control the gap Heating Time : 15 Seconds for 20mm dia Heating time : 10 Seconds for 20mm dia SAVING/YEAR (Rs) : 1,04,160.00 (SHEET ENCLOSED) Taper attachment Follower Adjusting Screw Bending Die Bending Roll

- 7. ANNEXURE: KAIZEN-01 (ZONE-2) BEFORE ELECTRIC LOAD /HOUR : 40 AMPS ENERGY COST/HR.(40 x Rs.3.90) : 156.00 ENERGY COST/SEC(Rs.156/60x60)Rs. : 0.0434 HEATING TIME/PIECE : 15 Seconds ENERGY COST/PIECE (15x0.0434)Rs. : 0.651 MONTHLY PRODUCTION : 40,000 PCS MONTHLY ENERGY COST(40000x0.651): 26,040.00 YEARLY ENERGY COST(26040.00x12) : 3,12,480.00 AFTER ELECTRIC LOAD /HOUR : 40 AMPS ENERGY COST/HR.(40 x Rs.3.90) : 156.00 ENERGY COST/SEC(Rs.156/60x60)Rs. : 0.0434 HEATING TIME/PIECE : 10 Seconds ENERGY COST/PIECE (10x0.0434)Rs. : 0.434 MONTHLY PRODUCTION : 40,000 PCS MONTHLY ENERGY COST(40000x0.434): 17360.00 YEARLY ENERGY COST(17360.00x12) : 2,08,320.00 SAVING/ YEAR (312480.00-208320.00) : 1,04,160.00

- 8. 38 SPG.PIN 20.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Operator moves 4 meters to unload the Bar & places it on the floor Reduce Operator Movement at Bar Turning Process (M/c No.31) (Muda of Movement) Operator has to hold 5 meter long bar from the end Bar stand not available Why ? Why ? Operator movement & placing on the floor Rack provided at machine height level Bar stand not available To eliminate muda of movement & Muri Status 12.08.01 Machine Target Date Resp SS35 JS, GS, DS, SS Reduce the operator movement & fatique 50% before 05.08.2001 (HOW MANY) 5000 Before After 1008 4032 0 1000 2000 3000 4000 Rs. 02 ( Zone-02) 36 12.08.01 SS Implemented Implemented Turning Bars BAR TURNING M/C Support Turning Bars BAR TURNING M/C Rack Time Consumed(Unloading) Time Consumed Daily (20x4) = 80 Min. Daily(20x1)= 20 Min. Monthly(80x25) = 2000 Monthly(20x25)=500 Monthly Cost (2000x0.168) Monthly Cost(500x0.168 =Rs.336.00 = Rs. 84.00 Yearly Cost (336x12) Yearly Cost(84.00x12) =4032.00 =1008.00 SAVING/YEAR(4032.00 - 1008.00) = 3,024.00

- 9. 08 CBT 04.08.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : One extra worker being used for filing operation, who removes the burr (Burr developed at the head milling operation). Save one worker at Filing operation (Muda of Waiting) Material received from milling m/c having burr Milling operator was overlooked the burr Why ? Why ? 6000 8000 0 2000 4000 6000 8000 Before After Rs. Milling operation is done by one worker & developed burr is removed by second worker by filing operation Worker used for filing Awareness/ Training given to operator to utilize his idle time for filing Lack of awareness/ Training To eliminate Muda of Waiting Milling & filing operations will be performed by one worker ( During waiting time for milling process, same worker removed the burr) so, the second worker to be saved Status 25.08.01 Machine Target Date Resp PS29 H.S., R.P., B.S., P.S.,B.S. One worker will be saved by 05.08.2001 01 ( ZONE-03) Why ? 1000 Pcs made by 3 Milling +1 Filing operator Salary of 4 Operators (2000x4) : 8000.00 (Rs) Salary of 3 Operators (2000x3) : 6000.00 (Rs) Saving/ Month (8000-6000) : 2000.00 (Rs) Saving/ Year (2000x12) :24000.00(Rs. Milling operator not used his idle time for filing the burr Why ? Lack of awareness/ training

- 10. 06 SBT 26.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Wastage of electric power (when the process is completed) but the 2 motors of M/c & Coolant Pump run continuously during idle time To save electric power by installing limit switch on m/c no.06 (Milling M/c) Power consumed by 2 Motors in idle time No provision available to stop the M/c in idle time Why ? Why ? 220 393 0 200 400 Before After Rs. Wastage of power on machine Limit switch provided No provision to stop the m/c when m/c is not carrying out the process Save electric power by installing limit switch on the machine StatusMachine Target Date Resp H.S., R.P., B.S., P.S.,B.S. Save electric power on m/c No.06 up to 28.07.2001 Earlier power consumption/shift : 4.77 Units Price for the same (4.77 x Rs.3.30) : 15.74 Cost / Month (Rs.15.74 x 25 Days) : 393.00 Now Power consumption/Shift : 2.67 Units Price for the same (2.67 x Rs.3.30) : 8.81 Cost / Month( Rs.8.81x 25 Days) : 220.00 Saving/Month (Rs.393-200) : 173.00 Saving/Year (Rs.173x12 months) : 2076.00 2 MOTORS ARE RUNNING REGULARLY (MAIN MOTOR OF M/C & MOTOR OF COOLANT PUMP) IN IDLE TIME ALSO. SO THE WASTAGE OF ELECTRIC POWER IS OBSERVED THE 2 MOTORS STOPPED IN IDEL TIME BY PROVIDING LIMIT SWITCHES ( SAVE OF ELECTRIC POWER) 05 20.07.01 HS,RP Implemented 21 22 25.08.01 26.08.01 HS,RP HS,RP Why ? Lack of awareness / training 02 (ZONE-03)

- 11. 30.31,32 NUT-1 16.07.01KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Nut Tapping machines 30,31,32 are being operated by 3 operators ( one operator for each machine) Manpower reduction and space recovery in Nut-1 Section Distance between m/c is 5 Feet Improper layout Why ? Why ? 73260 24420 0 20000 40000 60000 Before After Rs. 3 Operators at 3 Machines LAYOUT CHANGED Distance between M/Cs is too large & improper layout Layout of M/Cs to be changed StatusMachine Target Date Resp JS,CS, RC, GS & HS One operator will operate 3 machine by 21.07.01 01 (ZONE-4) 31 30 32 5 FEET 5 FEET 3 MACHINES, 3 OPERATORS 31 30 32 31 2 Feet 2 Feet 3 MACHINES, 1 OPERATOR 3 Operators Salary/ Year (Rs) : 73260 1 Operator salary / Year (Rs) : 24,420 Net Saving / Year: 73260-24420 (Rs) : 48840

- 12. 28 NUT-1 05.07.2001KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Operator fatigue is more on Tapping M/c No.28 After tapping oily Nuts are kept in trolley on wire mesh and oil from these Nuts is collected into trolley which is again re-filled in the M/c oil tank by lifting the trolley manually 3-4 times in a shift. Time wastage = 30 Minutes/Shift Oil Wastage = 200 ML/Shift= Rs.7.80 Operator fatigue is more on Tapping M/c No.28 (MURI & Muda of Movement) Trolley is being lifted by Operator 3-4 times in a shift to re-fill the oil in M/c oil tank through drum Absence of direct oil passage from trolley to oil tank Why ? Why ? 0 8280 0 2500 5000 7500 10000 Before After Rs. Operator fatigue/ time wastage/ Oil wastage Oil Passage provided Absence of oil passage To eliminate Muri & Muda of Movement Status 18.07.01 Machine Target Date Resp CS,GS25 CS,RC,GS,HS Trolley & oil tank to be connected with plastic pipe for direct oil passage by 10.07.2001 02 (ZONE-4) Oil wastage eliminated Oil re-filling time saved Operator Fatigue eliminated Net Saving/Year/Shift:2340+1800 = Rs.4140.00 Net saving/year/day: 4140.00x2 =Rs.8280.00 Implemented MACHINE OIL TANK NUTS TROLLEY DRUM MACHINE OIL TANK NUTS TROLLEY PIPE PLASTIC 30 31 32 20.07.01 26.07.01 28.07.01 CS,RC CS,GS CS,RC Implemented Implemented Implemented

- 13. ANNEXURE: KAIZEN NO. 02 ( ZONE-4) BEFORE COUNTER MEASURE OIL REFILL QUANTITY = 20 LITRES/SHIFT OIL WASTAGE/MONTH/Shift (Rs) = 195.00 (Rs.7.80 x 25days) OIL WASTAGE/YEAR/Shift (Rs) = 2340.00 (A) (Rs.195.00 X 12 months) TIME WASTAGE/MONTH/Shift (Rs) = 150.00 (30 Min x 25 = 750 Min(12.5 Hrs) Time wastage/Year/Shift (Rs.) = 1800.00 (B) (150.00x12) Total Wastage/ Year/Shift (A+B) Rs. = 4140.00 Total Wastage/Year/Day(4140x2) Rs. = 8280.00 AFTER COUNTER MEASURE • OIL WASTAGE ELIMINATED NET SAVING/ YEAR/Shift (Rs) = 2340.00 • TIME WASTAGE ELIMINATED •NET SAVING /YEAR/Shift (Rs) =1800.00 •TOTAL SAVING/YEAR/SHIFT (2340+1800.00)(Rs) =4140.00 •TOTAL SAVING/YEAR/DAY(4140x2) (Rs.) =8280.00

- 14. FRG. 21 Hot Forge Shop 27.07.01KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : Muda of Movement & counting process. To eliminate the movement & counting of material from trolley to tray on m/c no. 21 trimming Wheeled trolley size is big & Height is less from reqd size Generic trolley not suitable for trimming m/c Why ? Material moves from Trolley to tray ? TWO WHEELED TROLLEYS PROVIDED ON MACHINE & COUNTER TO BE INSTALLED Fixed tray is with m/c Fixed tray to be replaced with wheeled trolley of same size & Counter to be installed on m/c StatusMachine Target Date Resp Hamir Singh, Lakhwant Singh, Rattan Singh Moveable trolley to be made Before 30.07.01 04 ( V) TIME Saving = 1.5 Hour/Day/M/c = 450 Hour/Year/M/c =56Man Days/M/c Time saving on 2 Machines = 112 Man days/year = 3.7 Months Yearly Saving = 3.7x2500=Rs. 9250/- FRG. 22 13.08.01 ImplementedH.S, S.S 2300 2700 2000 2200 2400 2600 2800 BEFORE AFTER PRODUCTION PERM/C Why ? Why ? Lack of awarenes/training COUNTER YET TO BE INSTALLED

- 15. - COLD FORGING 30-4-01KAIZEN SHEET G.S.AUTO, LUDHIANA Machine : Unit : Date : Kaizen Theme : Target & Target date : Problem : Before Counter Measure : Benefits/Results after Implementation : Analysis : After counter measure : Scope & plan for horizontal deployment : (WHAT& WHICH) (HOW MUCH & WHEN) (WHERE) (HOW MANY) Implemented by : (WHO) Kaizen no. : (HOW) Root Cause : Idea : Counter measure : PRODUCTION OF STEP TURNING IS LESS AS COMPARED TO STEP REDUCING OPERATION & TURNING IS FOLLOWD BY GRINDING OPERATION & CYCLE TIME MORE e.g.62 HOURS FOR TURNING & GRD OPERATION TO ELIMINATE THE GRINDING PROCESS IN MBJT-228 (MUDA OF PROCESS) TURNING IS DONE TO MAINTAIN ANGLE 30 DEG & TURNING OPERATION IS NOT CAPABLE TO MEET REQD THE PRE THRD ROLL DIA . Why ? 1 BLANK CUTTING 2 HEAD FORGING 3 STEP TURNING 4 STEP GRINDING 5 THREADING THREADED R.D.IS BEING MADE BY TURNING AND THEN BY GRD OPERATION NON THREADED DIA TO BE CHANGED SAME AS OF PRE THREAD ROLL DIA END APPLICATION HAS NO MEANING OF ANGLE 30 DEG CUSTOMER TO BE APPROACHED FOR REVIEW OF SPECIFIACTION 1 BLANK CUTTING 2 STEP REDUCING 3 HEAD FORGING 4 THREADING Status 20.9.01 PART No Target Date Resp A.K./JSMBJT-226 HAMIR SINGH,ASHOK KUMAR, JATINDER SINGH,PARAMJIT SINGH DRAWING WITH ANGLE 15 DEG TO BE SENT TO CUSTOMER FOR APPROVAL 05 (V) REDUCTION IN WT/PC=11 gms MAT.SAVING = 33 Kg/MONTH REDUCTION IN OPERATION COST=Rs 0.42/PC MONTHLY SAVING IN 3000PCS=690+1260 YEARLY SAVING = Rs 23400/-. 16230 14280 13000 13500 14000 14500 15000 15500 16000 16500 BEFORE AFTER COSTINRs CYCLE TIME IS MORE WHY?