Downloaded 15 times

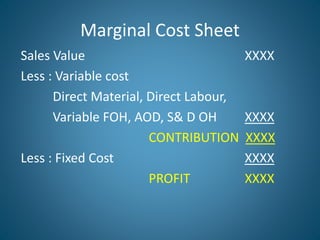

Marginal costing is a technique that separates total costs into fixed and variable costs. It helps management make decisions by calculating indicators like profit volume ratio, break-even point, margin of safety, and indifference point. The document provides an example problem demonstrating how to use marginal costing to calculate these indicators and make decisions. It also discusses how marginal costing varies from other costing techniques.