This document provides an introduction and overview of India's GST composition scheme. Key points include:

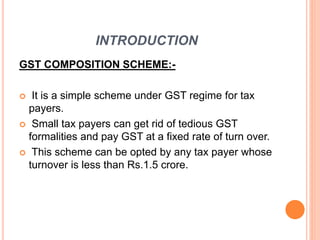

- The composition scheme is a simple alternative for small taxpayers with turnover less than Rs. 1.5 crore to pay GST at a fixed rate instead of going through regular GST procedures.

- As of 2019, service providers can now opt for the composition scheme if their turnover is below Rs. 50 lakhs.

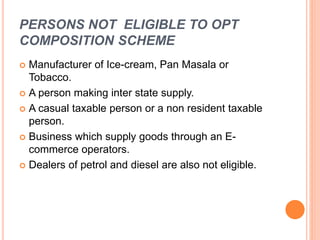

- To be eligible, total turnover from all businesses with the same PAN must be below Rs. 1.5 crore, and some business types like manufacturers of specific goods are excluded.

- Opting for the composition scheme means no input tax credit can be claimed but