Downloaded 178 times

This document provides an overview of input tax credit under the GST Act. It defines input tax and input tax credit, outlines the eligibility and conditions for claiming ITC, and discusses the time limit. It also covers apportionment of credit and blocked credits, availability of credit in special circumstances like new registration or exempt supplies becoming taxable. The document discusses ITC on capital goods, distribution of credit by an Input Service Distributor, and recovery of excess credit distributed. Overall it serves as a comprehensive guide to the key aspects of input tax credit under Indian GST law.

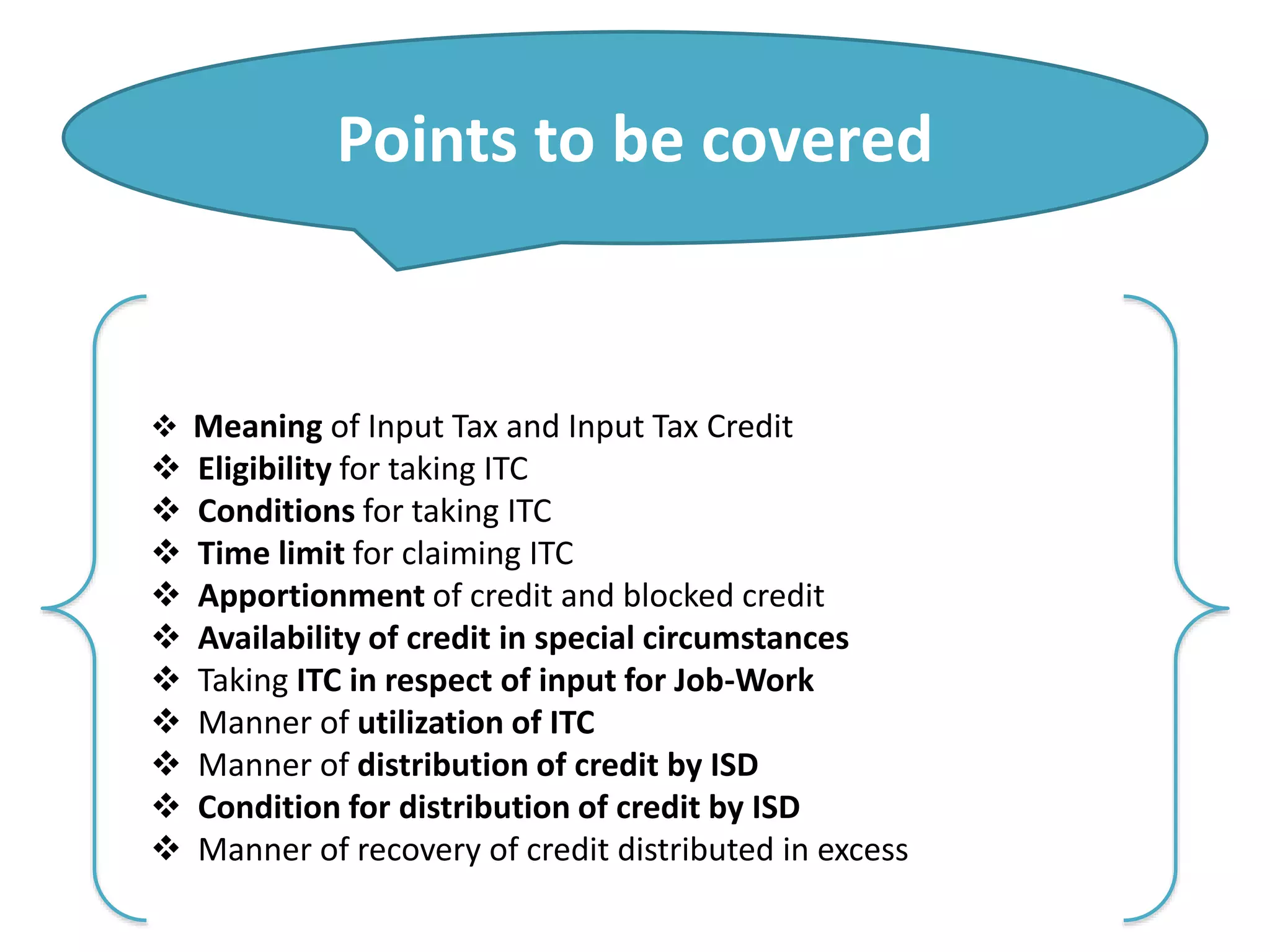

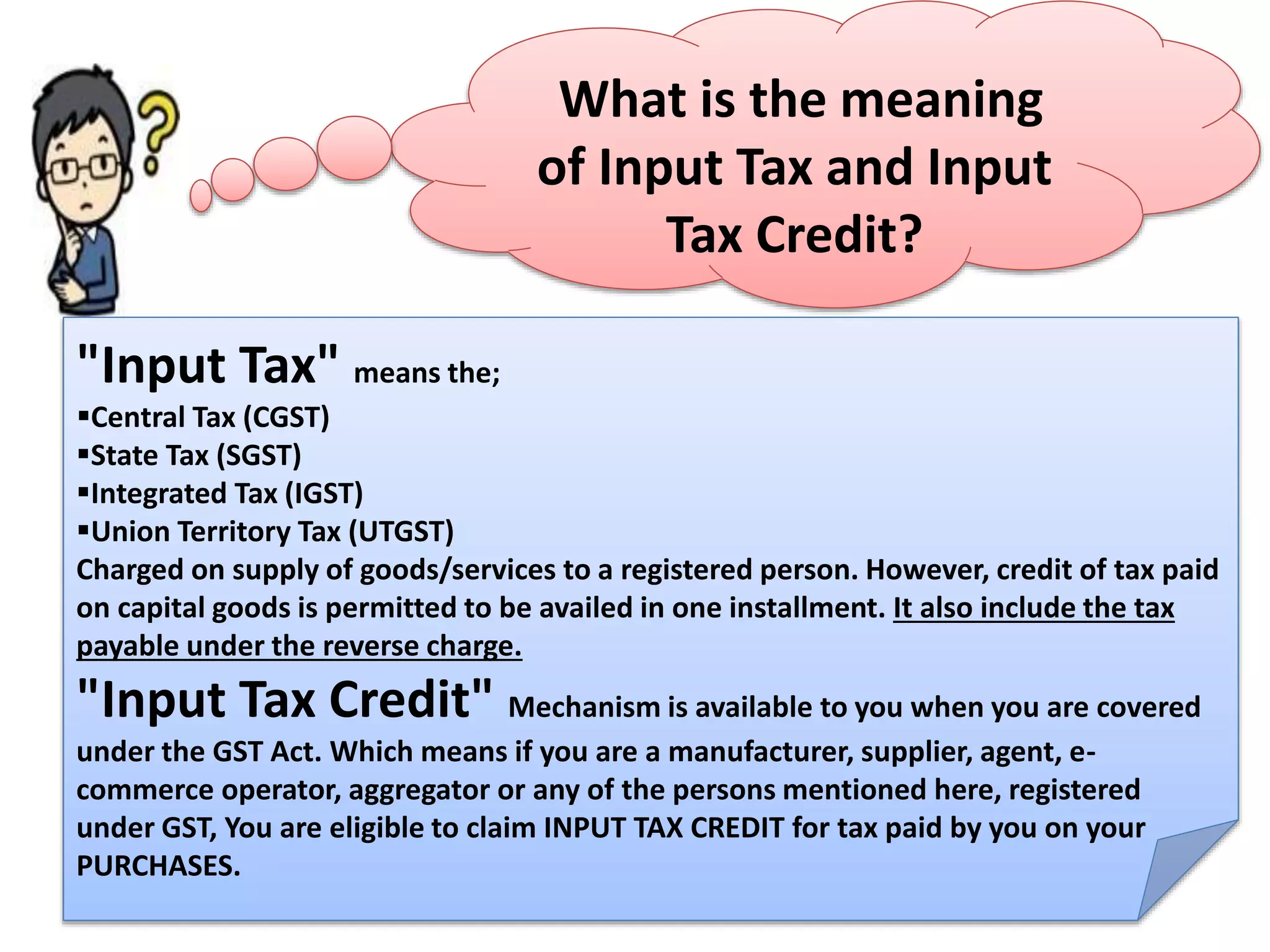

Introduces Input Tax Credit (ITC) under GST, eligibility, and definition of terms.

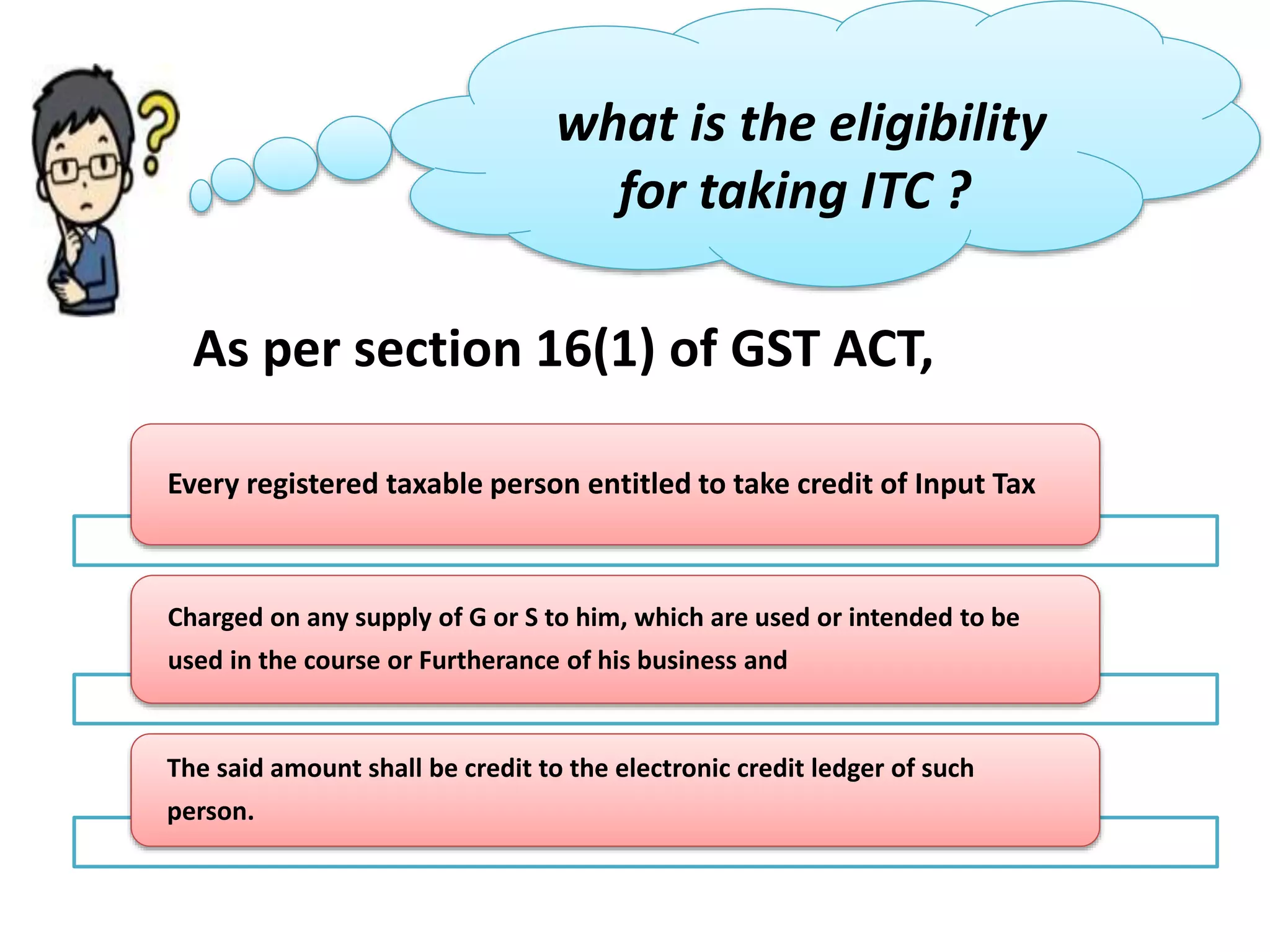

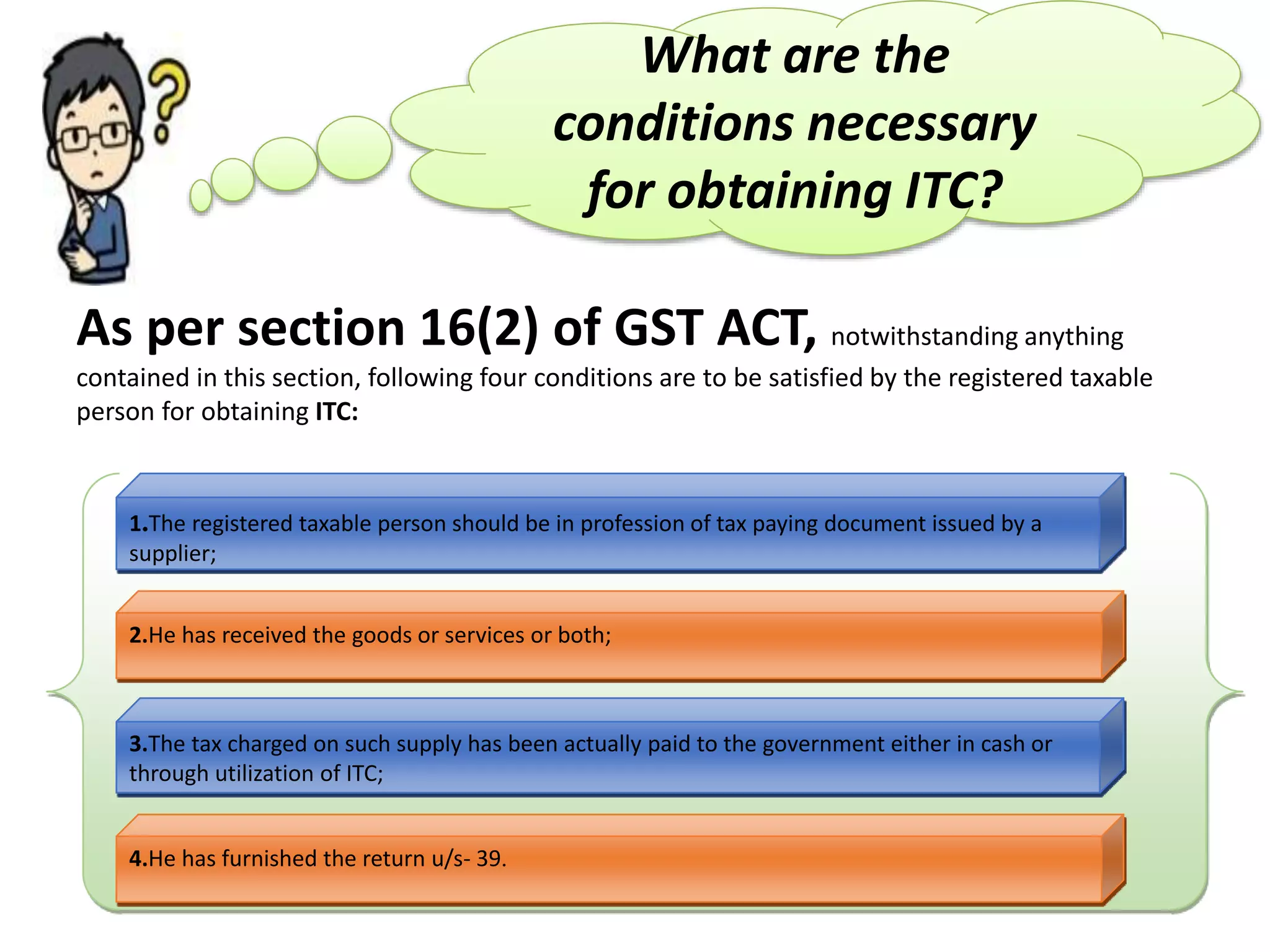

Discusses eligibility criteria and necessary conditions for availing ITC, including key compliance.

Explains restrictions on ITC for capital goods and time limits for claiming ITC.

Covers apportionment rules for ITC, blocked credits, and items where ITC is not admissible.

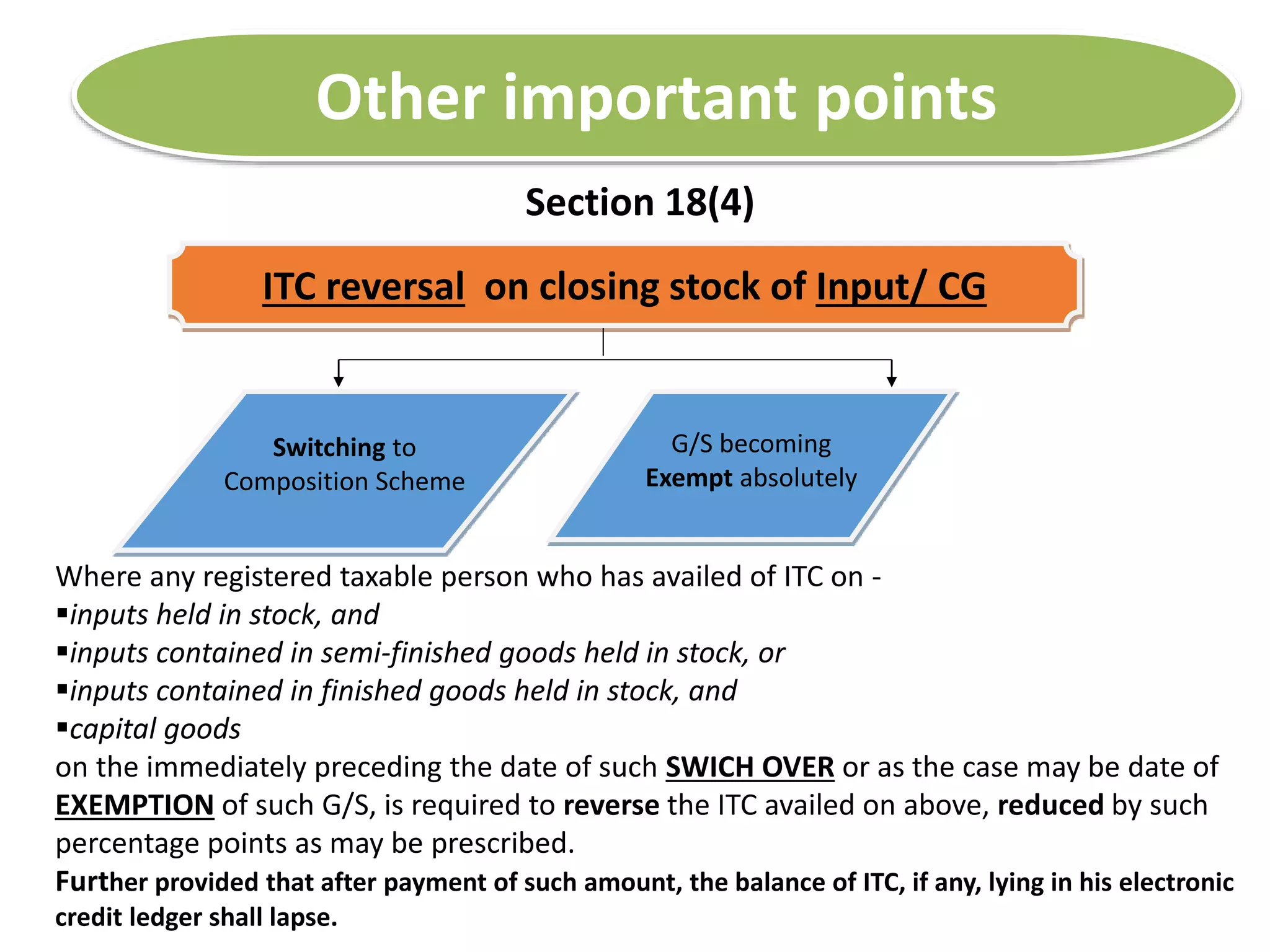

Discusses ITC regarding opening stock at registration and conditions for switching schemes.

Outlines rules for taking ITC on inputs and capital goods sent for job work.

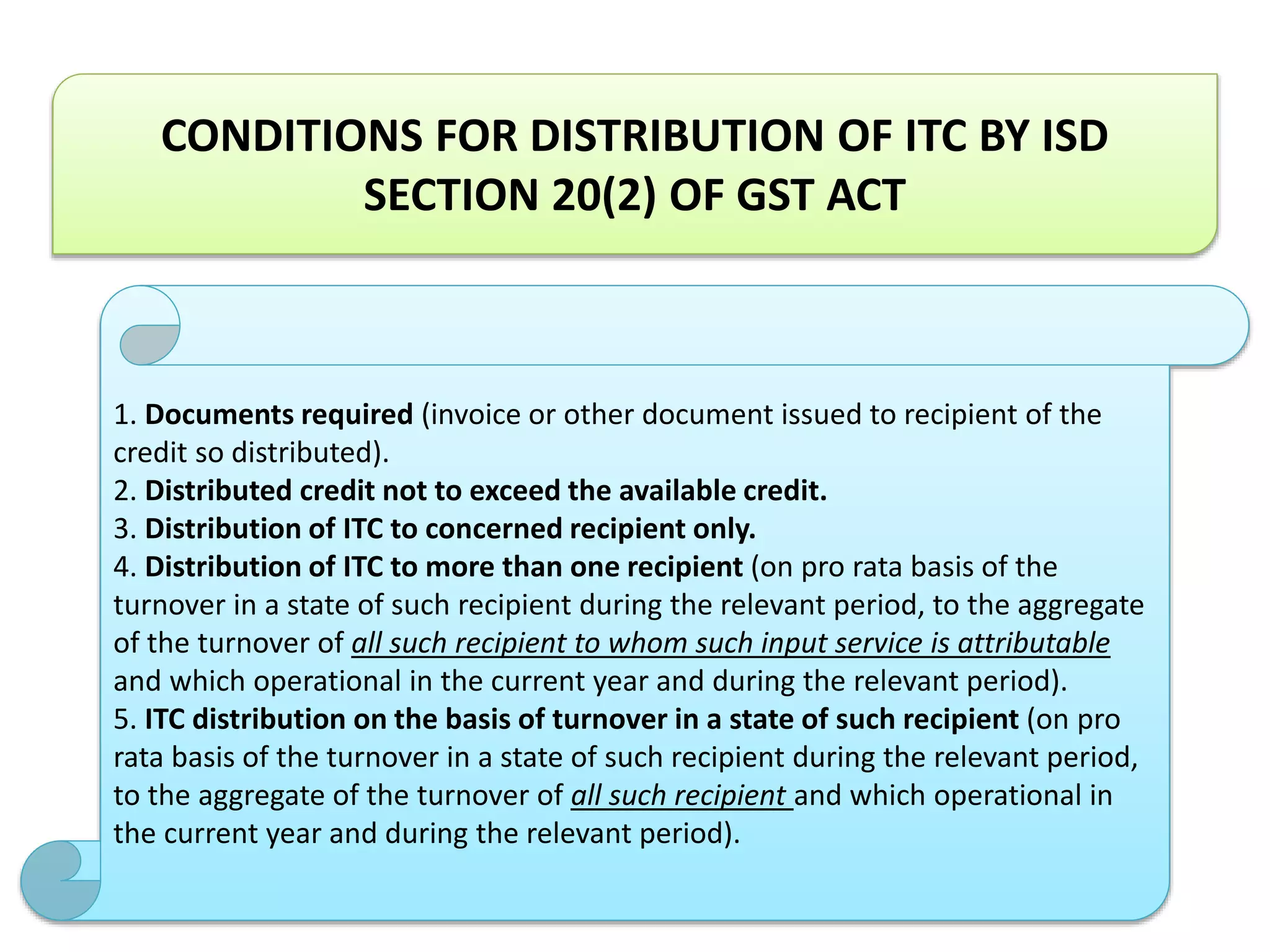

Explains utilization order of ITC and conditions for distribution by Input Service Distributor (ISD).

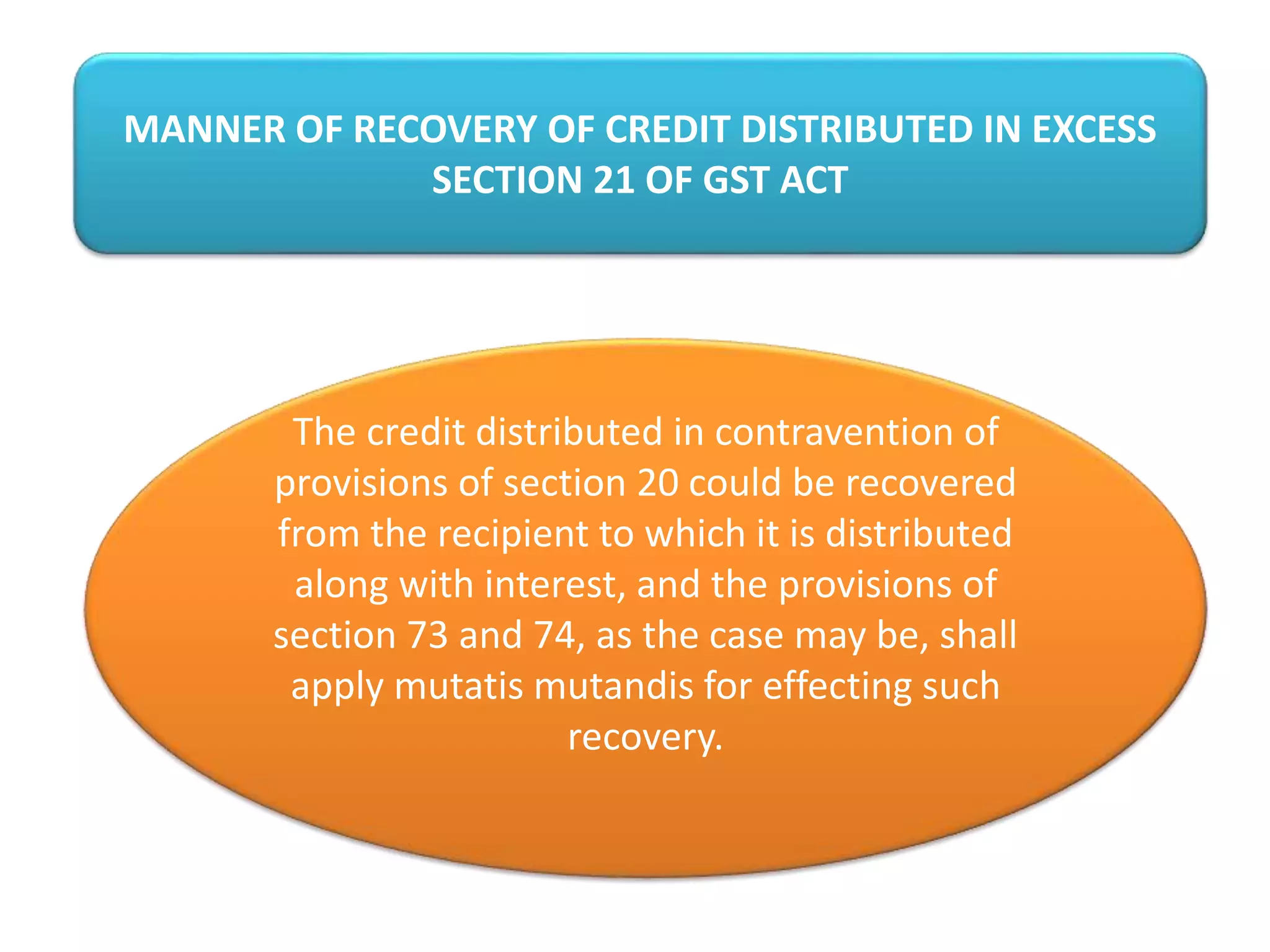

Describes processes for ITC matching and identifies situations leading to mismatching.

Concludes the presentation and acknowledges the audience.

![GST RETURNS [ TAXATION ]](https://cdn.slidesharecdn.com/ss_thumbnails/taxationgstreturns-210303051831-thumbnail.jpg?width=640&height=640&fit=bounds)