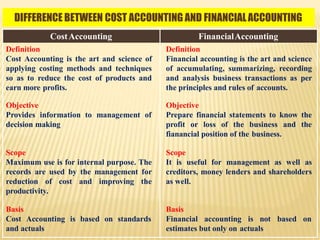

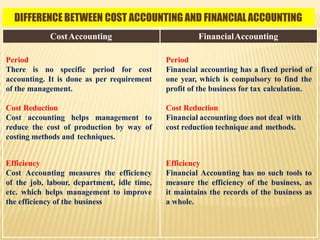

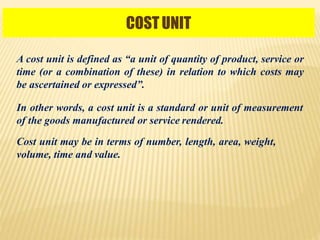

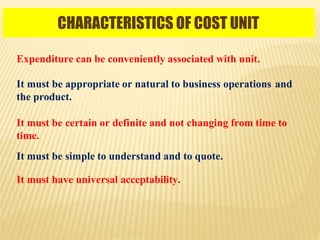

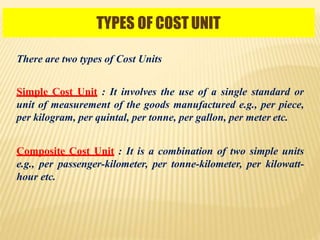

The document discusses cost accounting and its importance in measuring and managing costs within an organization, highlighting the differences between cost accounting and financial accounting. It explains the goals, advantages, and disadvantages of cost accounting, its role in decision-making, budgeting, and efficiency improvement. The document also outlines the responsibilities of a cost accountant, including cost ascertainment, comparison, analysis, reduction, and control.