Downloaded 51 times

![Health & Wellness

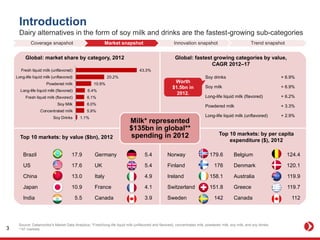

Organic innovation remains slow in the milk sector

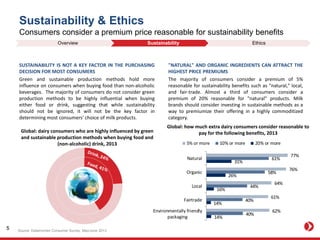

PRICE IS A MAJOR BARRIER TO ORGANIC CONSUMPTION

Product development in organic milk has increased since 2008, but at

a very slow rate. In 2008, 10% of new milk launches were organic,

compared to 12% in 2012. Lack of innovation can be attributed to

reluctance by consumers to pay a premium for organic products,

particularly in a category characterized by habit and convenience.

More than half of dairy consumers cite "too expensive" as a major

drawback to organic products. The challenge for organic milk

producers is to convince consumers it is worth paying more for by

finding ways to add value. ShopRite organic rice milk (US), for

example, is enriched with vitamins and calcium for added health

benefits.

0%

2%

4%

6%

8%

10%

12%

14%

2008 2009 2010 2011 2012

Nature's Promise organic 2%

milk

US

ShopRite original organic rice

milk

US

Global: new milk products tagged "organic," as a

proportion of all new milk launches, 2008–12

Source: [1] Supermarket News, January 2012; Datamonitor's Product Launch Analytics

Global: dairy consumers who consider the following to be

major drawbacks of organic products, 2013

Overview Positive nutrition Low fat Sports nutrition Organic

4](https://image.slidesharecdn.com/consumer-innovation-trends-milk-140426101631-phpapp01/85/Consumer-and-Innovation-Trends-in-Milk-4-320.jpg)

This document discusses trends in the milk industry from 2013. It covers topics like health and wellness, sustainability, evolving consumer landscapes, and more. Some key points include that organic milk innovation has been slow, with only 12% of new milk launches in 2012 being organic. Consumers consider premium pricing reasonable for sustainability benefits like products being natural or local. Also, aging populations around the world present opportunities to develop products catering to the needs of seniors by promoting milk's natural health benefits.