Downloaded 244 times

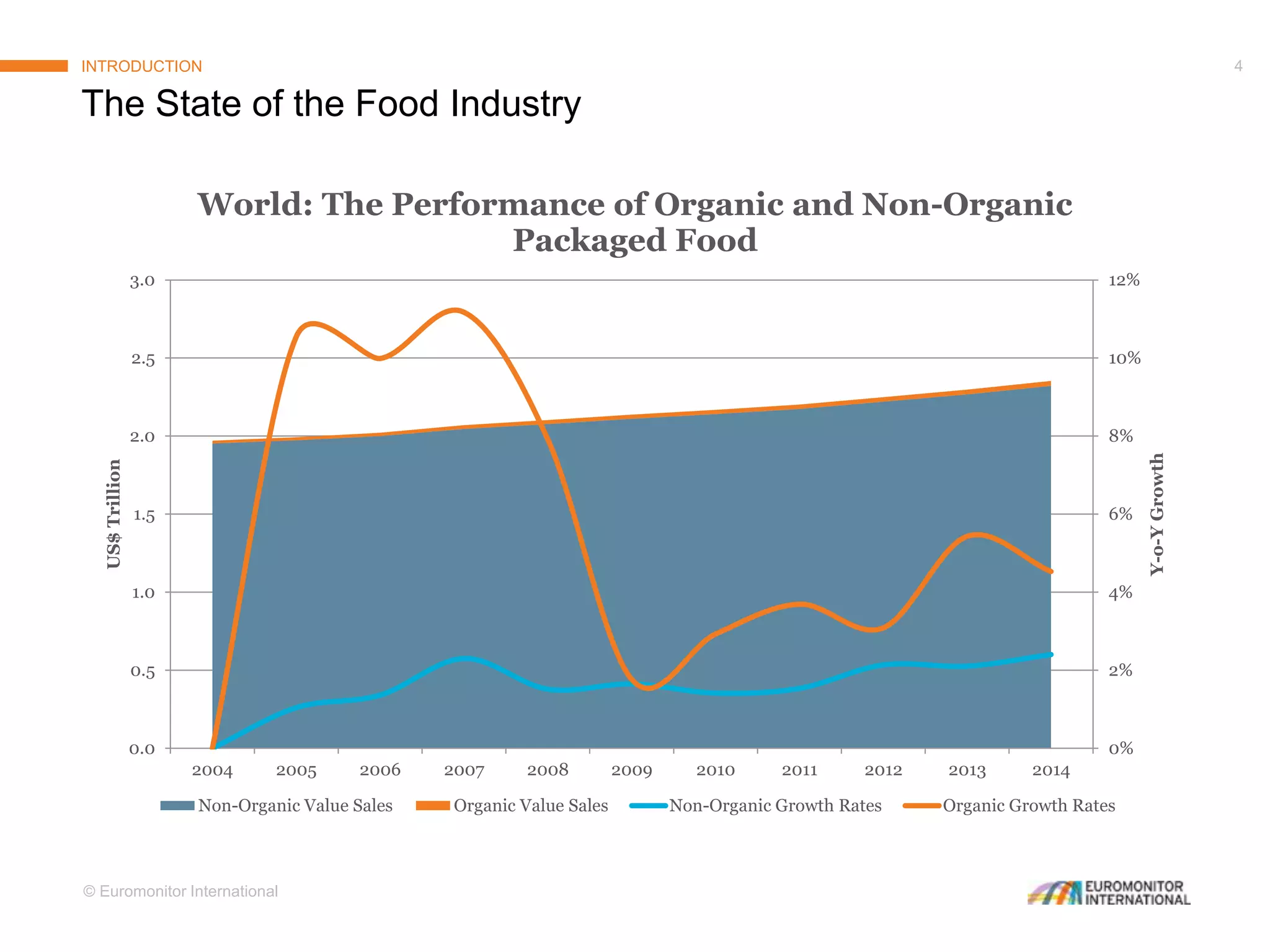

The document analyzes changing consumer attitudes towards organic food, highlighting significant global variations in acceptance and pricing. It identifies four primary consumer types and discusses the implications for the packaged food industry, including the low penetration of organic products among major food companies. The report suggests that while organic food faces challenges in growth and market perception, opportunities remain for brands that can adapt to evolving consumer demands.