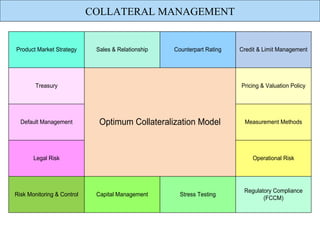

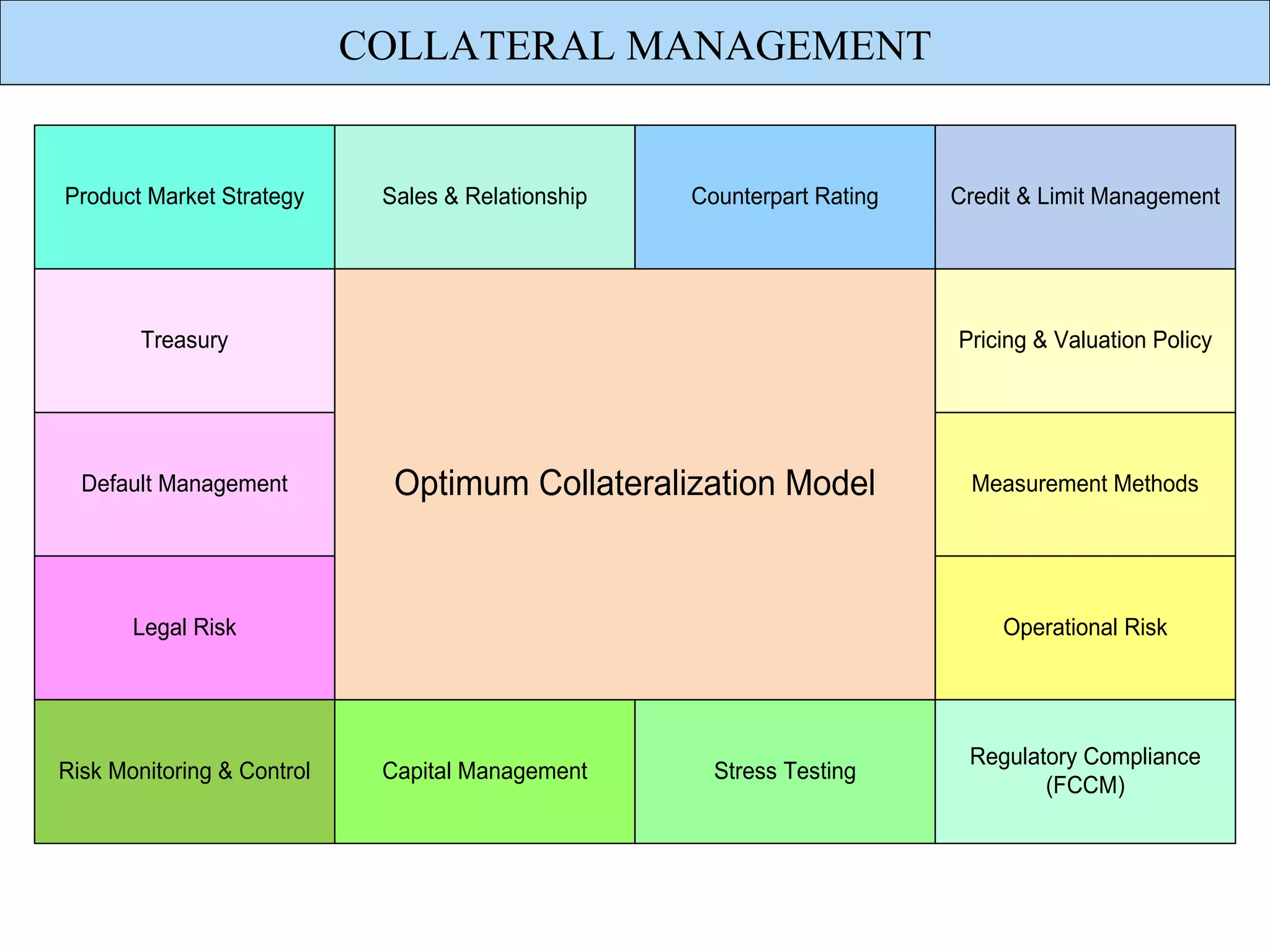

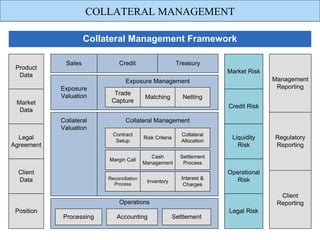

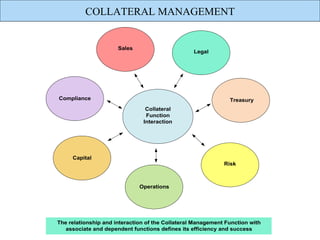

The document discusses collateral management and its key functions. Collateral management focuses on credit risk mitigation and reducing loss given default through improved recovery rates. Efficient collateralization can lower expected losses and allow reductions in economic and regulatory capital. However, collateralization also introduces legal and operational risks. Traditionally located within operations or credit, collateral management interfaces with various functions like sales, risk, and treasury. The selection of collateral assets and accurate exposure measurement are critical factors for collateral management success.