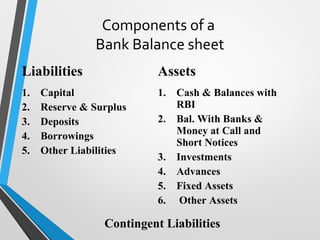

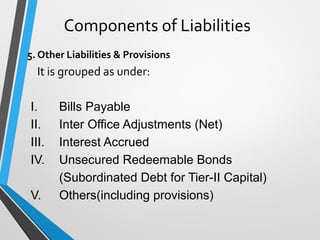

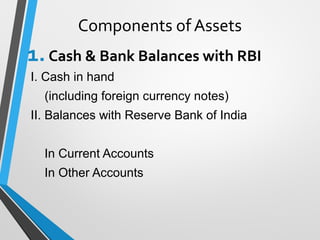

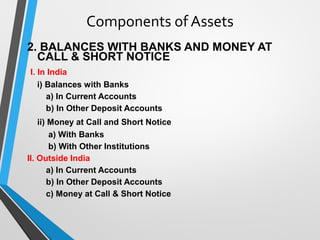

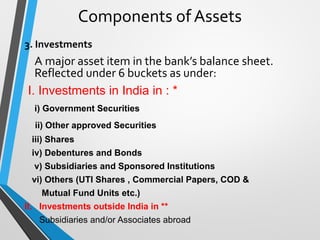

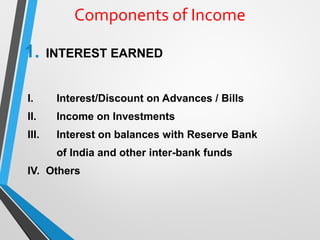

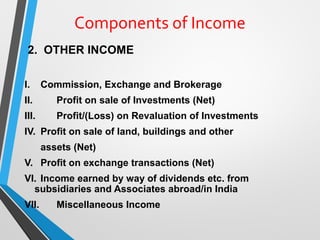

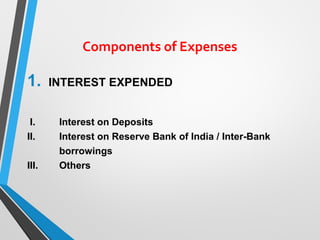

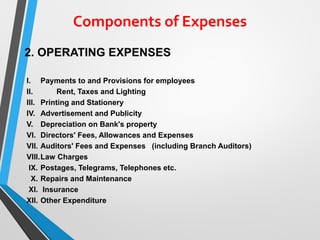

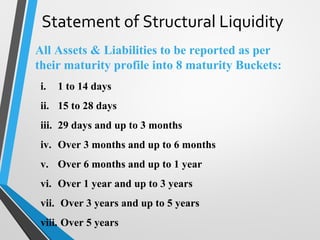

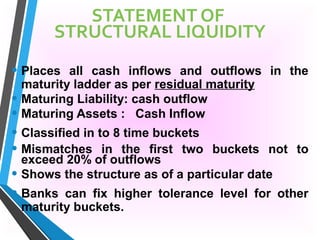

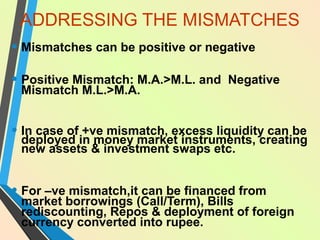

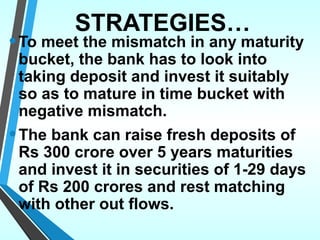

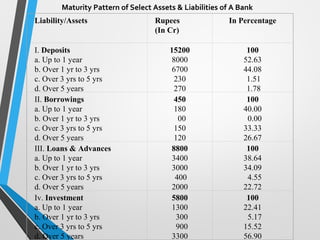

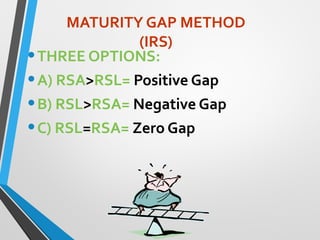

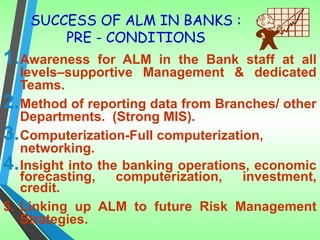

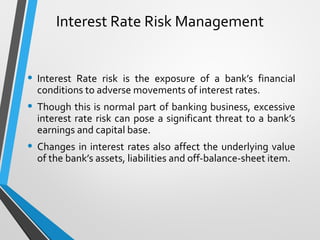

The document provides an overview of the key components of a bank's balance sheet, including assets and liabilities. It discusses the various line items under assets (such as cash, investments, advances) and liabilities (such as capital, reserves, deposits, borrowings). It also summarizes the components of a bank's profit and loss statement and provides details on liquidity management, asset liability management and interest rate risk management. The document is intended as a presentation on managing a bank's assets, liabilities, liquidity and interest rate risk.