Downloaded 136 times

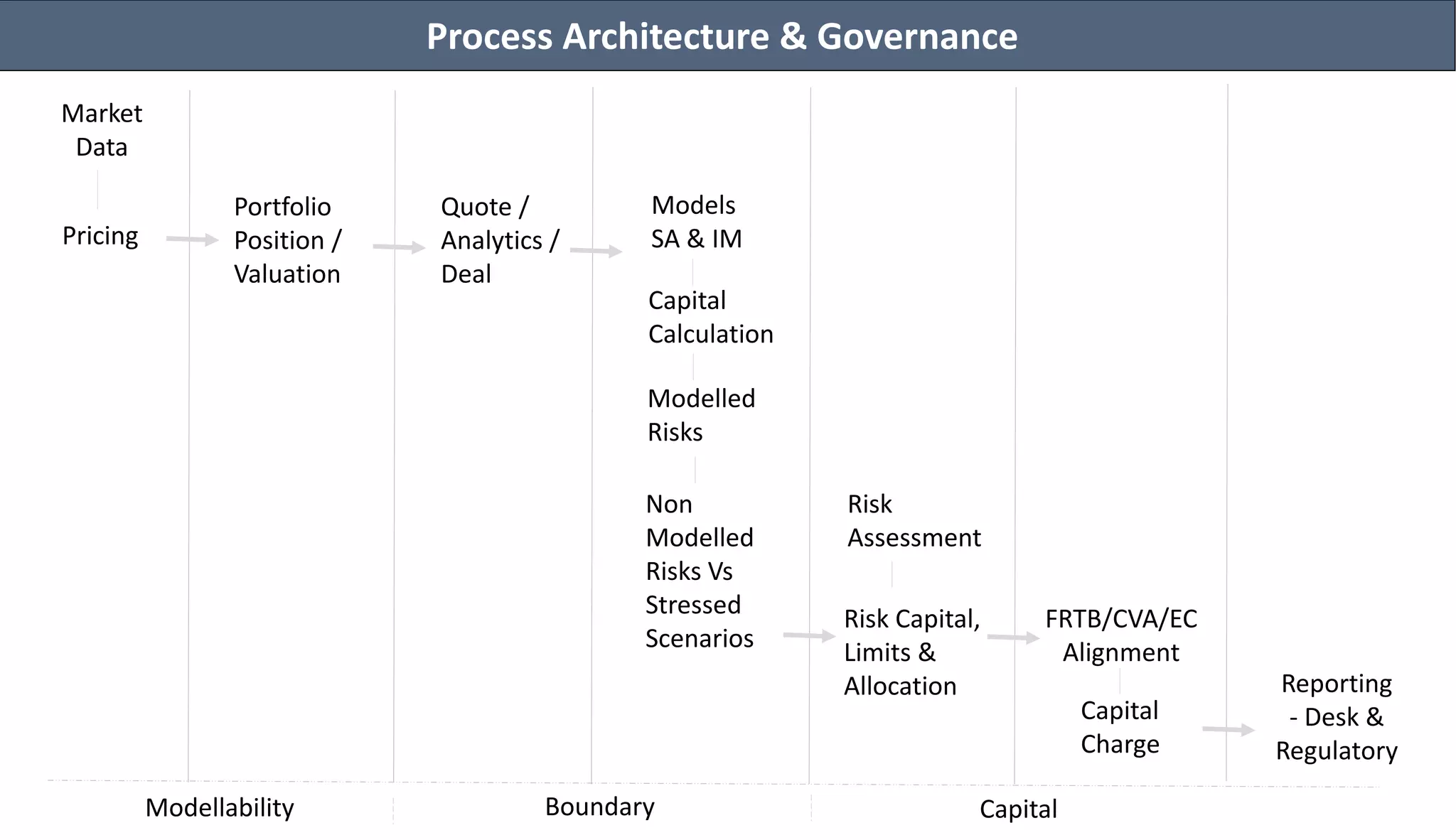

1. The revised FRTB framework aims to address weaknesses in capital requirements and distinguish between trading book and banking book holdings by requiring higher capital for trading book assets. 2. Firms seek to move assets between books to minimize capital requirements based on liquidity and profitability as positions change. 3. Key impact areas of FRTB include OTC derivatives, securitization, and more complex instruments. Firms will need new business models and technology to implement FRTB.