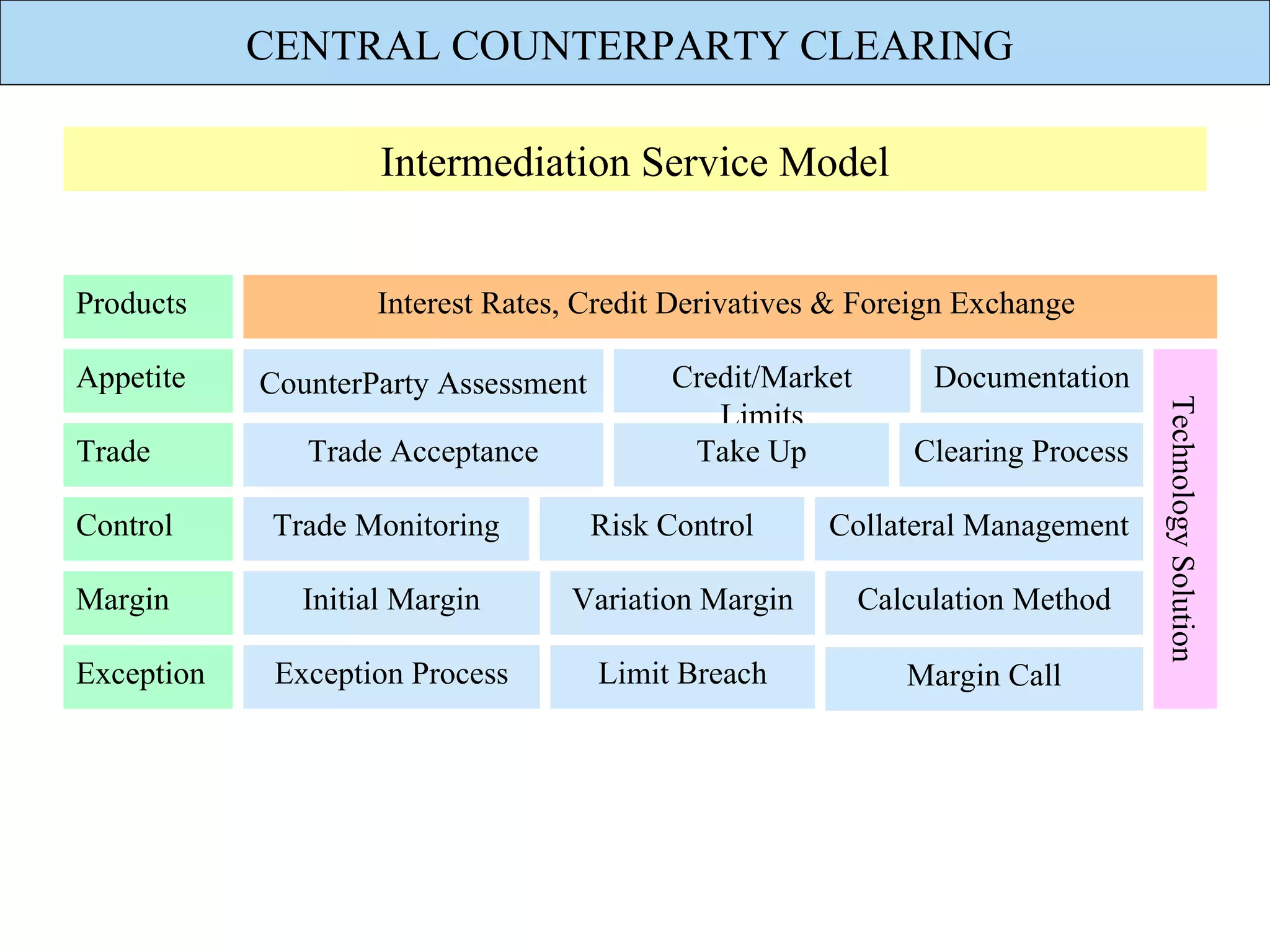

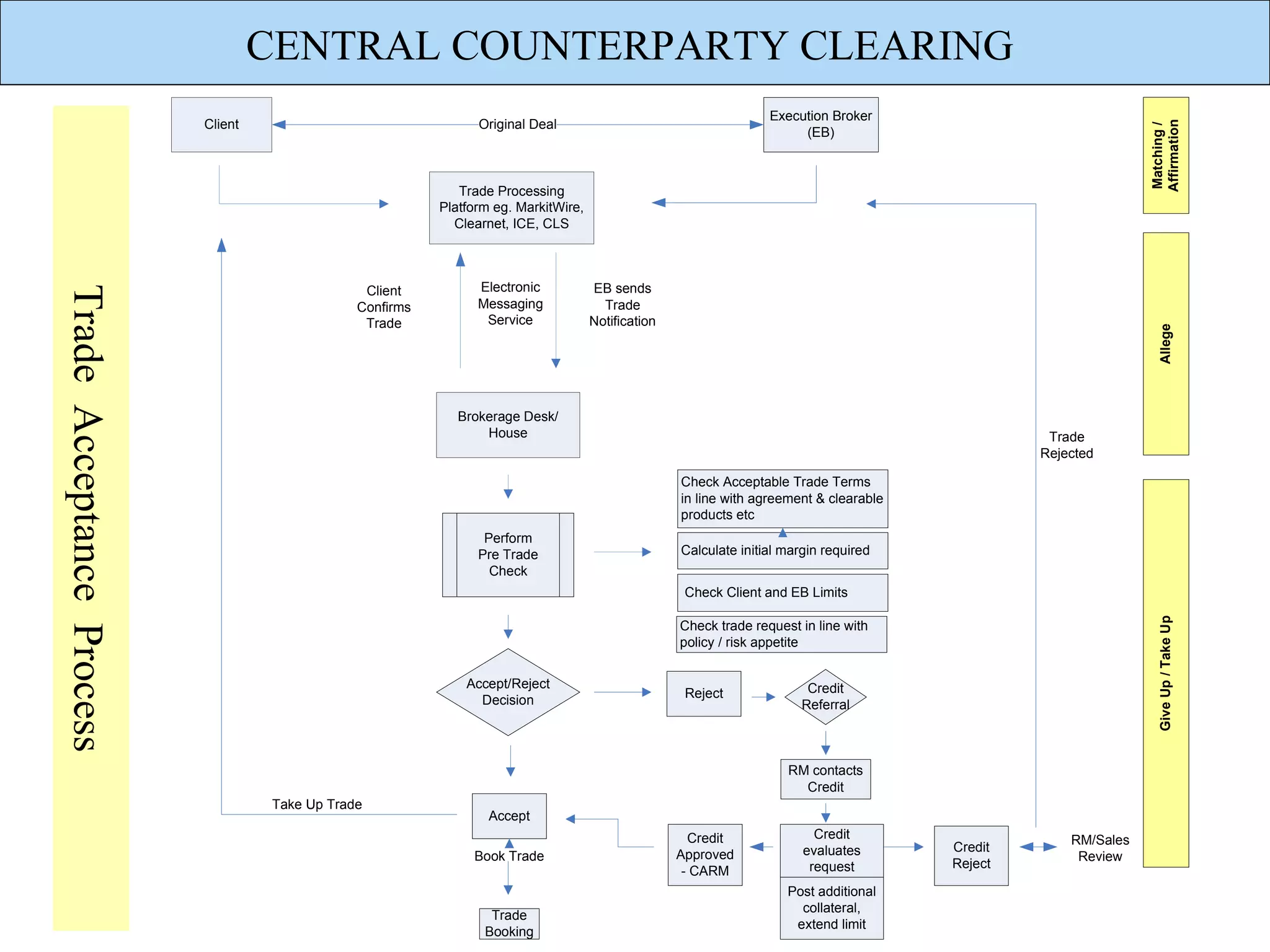

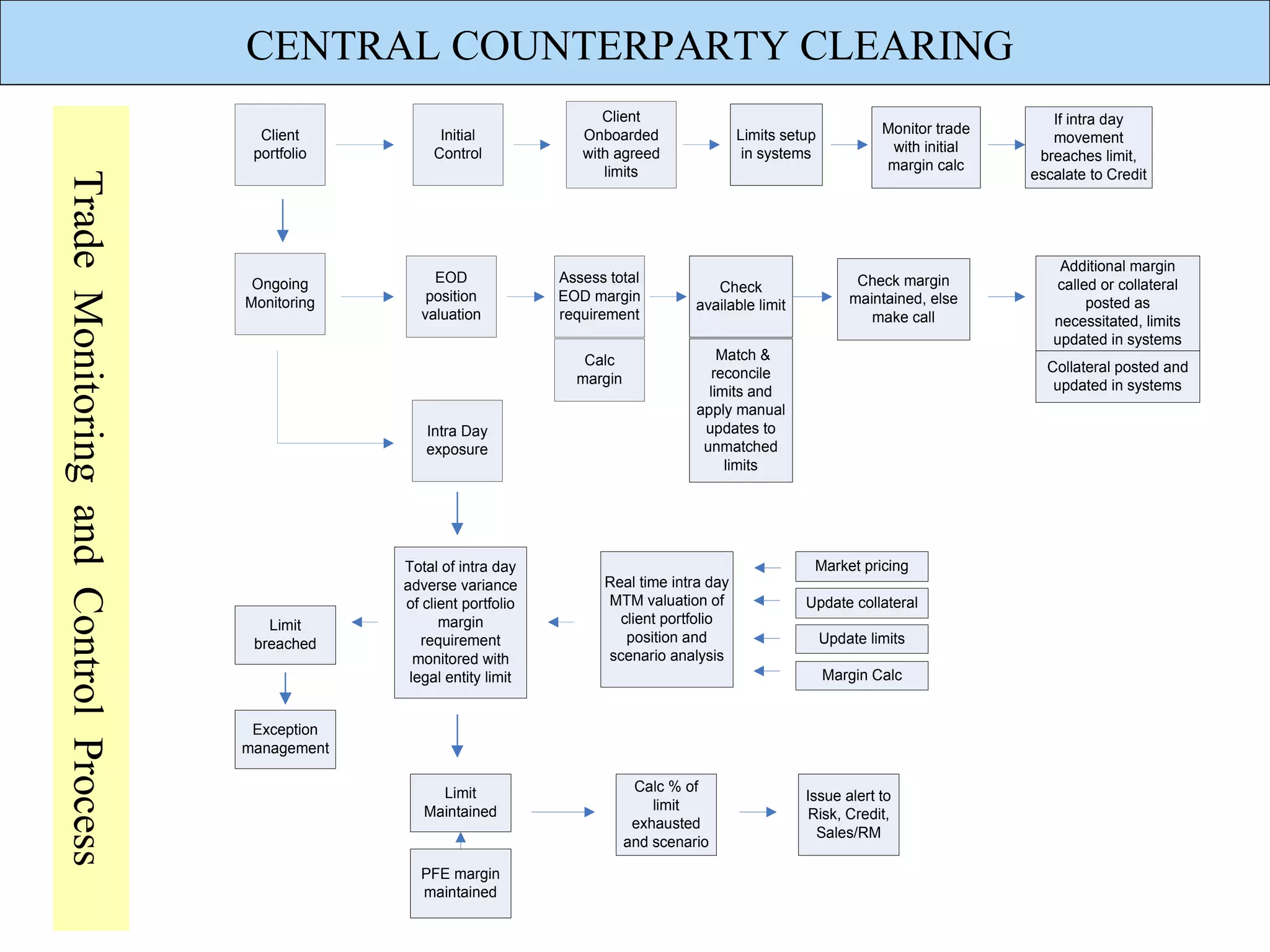

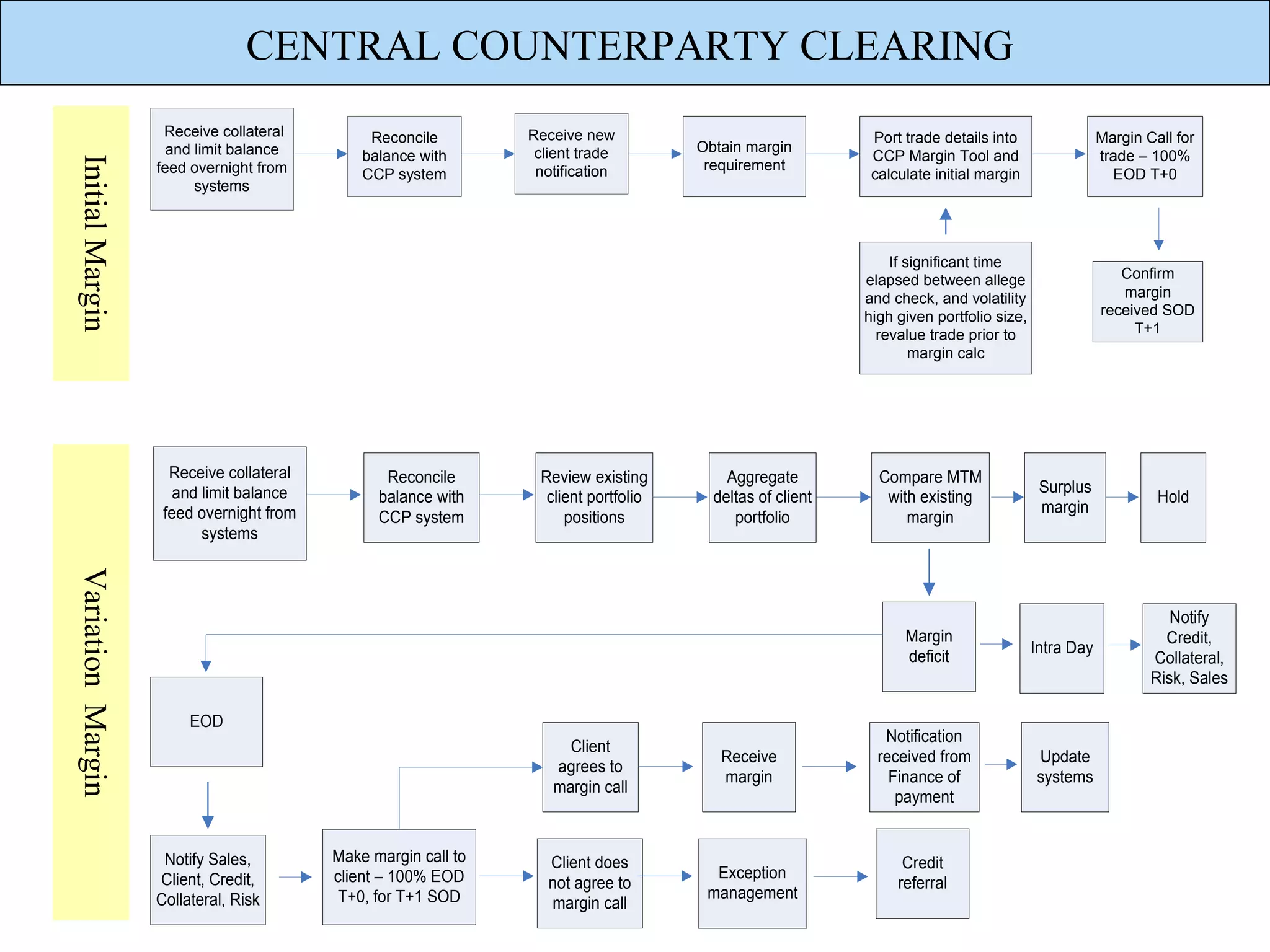

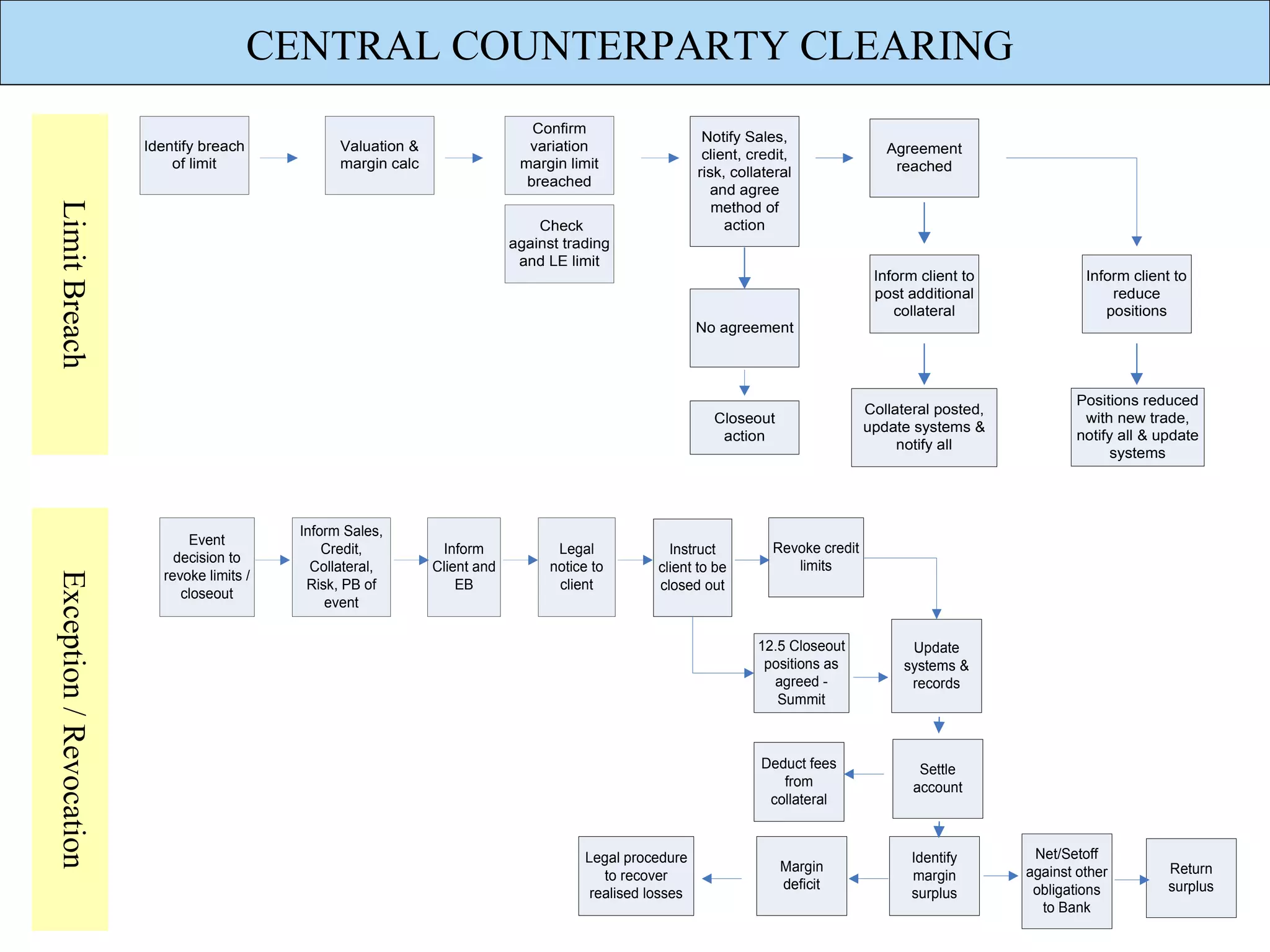

Central counterparty clearing involves: 1) Accepting and clearing trades of interest rates, credit derivatives, and foreign exchanges. 2) Monitoring trades, calculating initial and variation margin requirements, and managing collateral and limits. 3) Handling exceptions such as breached limits through actions like margin calls, reducing positions, revoking limits, or closing out trades.