Exposure Measurement

•

0 likes•638 views

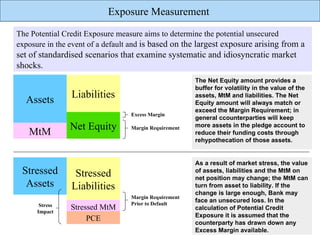

The Potential Credit Exposure measure aims to determine the largest unsecured exposure that could arise if a counterparty defaults due to market shocks. It examines scenarios where assets and liabilities are stressed and the mark-to-market value changes, which could cause the net position to become a liability. If the stress impact creates a shortfall larger than the excess margin, the bank may face an unsecured loss upon default. The measure will be positive if the collateral value covers positions under stress scenarios, but negative if there is a shortfall that could cause potential loss.

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (17)

Similar to Exposure Measurement

Similar to Exposure Measurement (20)

Recently uploaded

Recently uploaded (20)

Exposure Measurement

- 1. Exposure Measurement The Potential Credit Exposure measure aims to determine the potential unsecured exposure in the event of a default and is based on the largest exposure arising from a set of standardised scenarios that examine systematic and idiosyncratic market shocks. The Net Equity amount provides a buffer for volatility in the value of the Liabilities assets, MtM and liabilities. The Net Assets Equity amount will always match or exceed the Margin Requirement; in Excess Margin general ccounterparties will keep Net Equity Margin Requirement more assets in the pledge account to MtM reduce their funding costs through rehypothecation of those assets. As a result of market stress, the value Stressed Stressed of assets, liabilities and the MtM on net position may change; the MtM can Assets Liabilities turn from asset to liability. If the change is large enough, Bank may Margin Requirement Prior to Default face an unsecured loss. In the Stress Impact Stressed MtM calculation of Potential Credit Exposure it is assumed that the PCE counterparty has drawn down any Excess Margin available.

- 2. Exposure Measurement The measure will have a positive value under many scenarios, indicating that the value of the collateral under these scenarios is sufficient to cover market stress; negative values on the other hand indicate a shortfall in the value of the collateral versus the positions held, and a potential loss for the Bank. Stress Impact, indicates the “volatility” of the portfolio and P&L effect implicit in the measure. Stress Impact = Potential Shortfall Exposure – Margin Requirement Net Equity = Net Assets + Net MTM - Net Liabilities PCE = Stressed Assets + Stressed Liabilities + Stressed Net MtM – Excess Margin