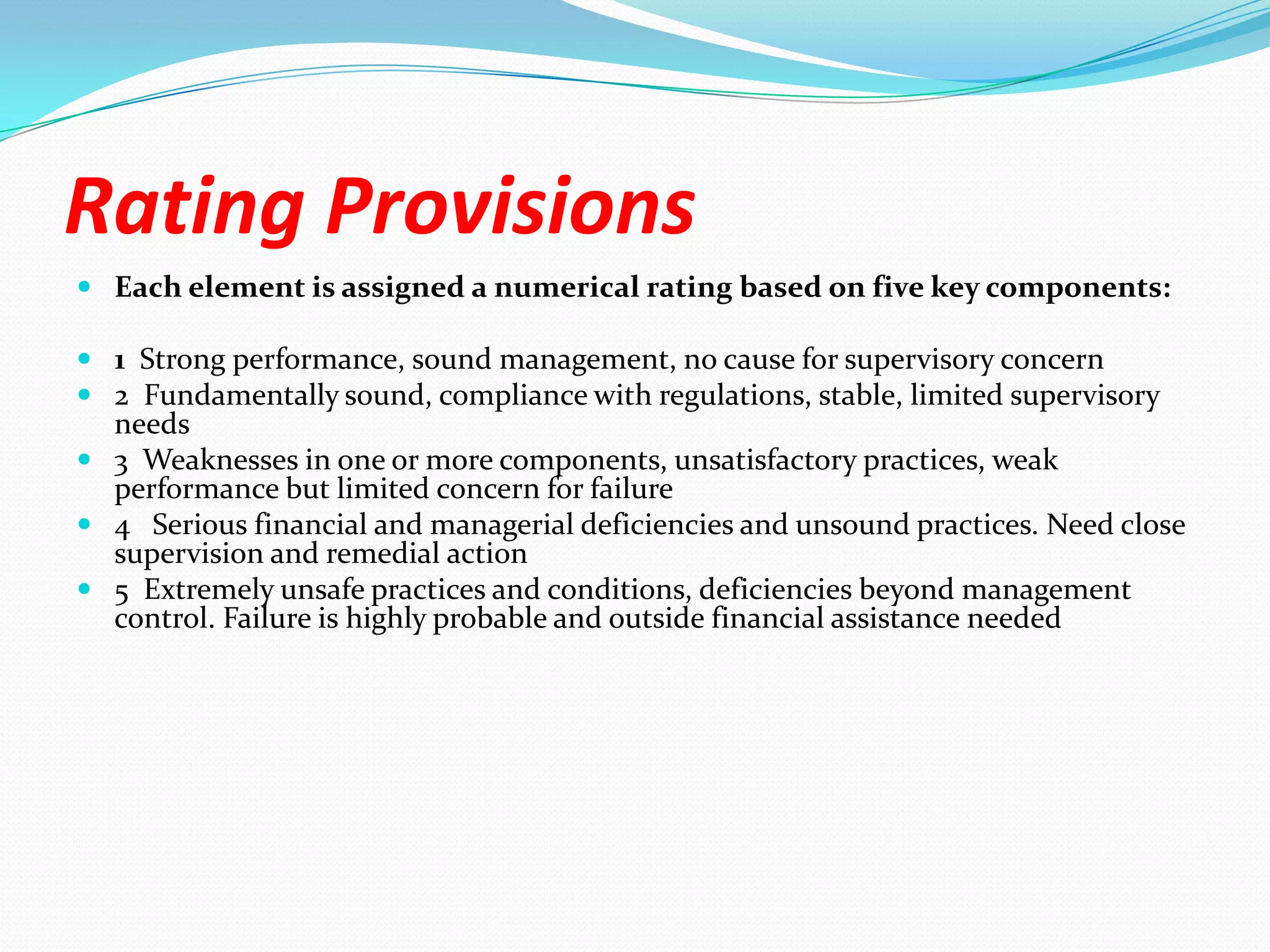

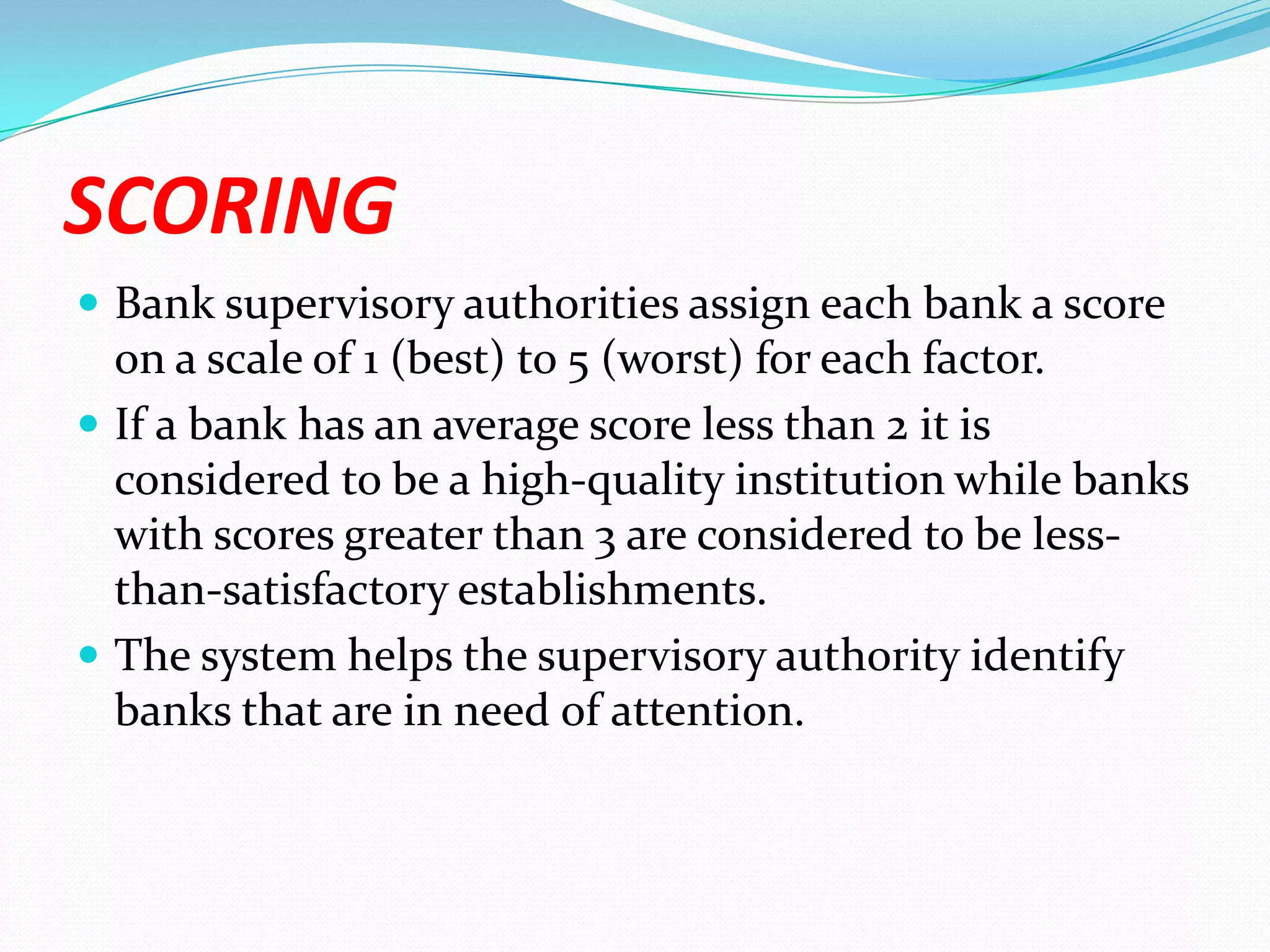

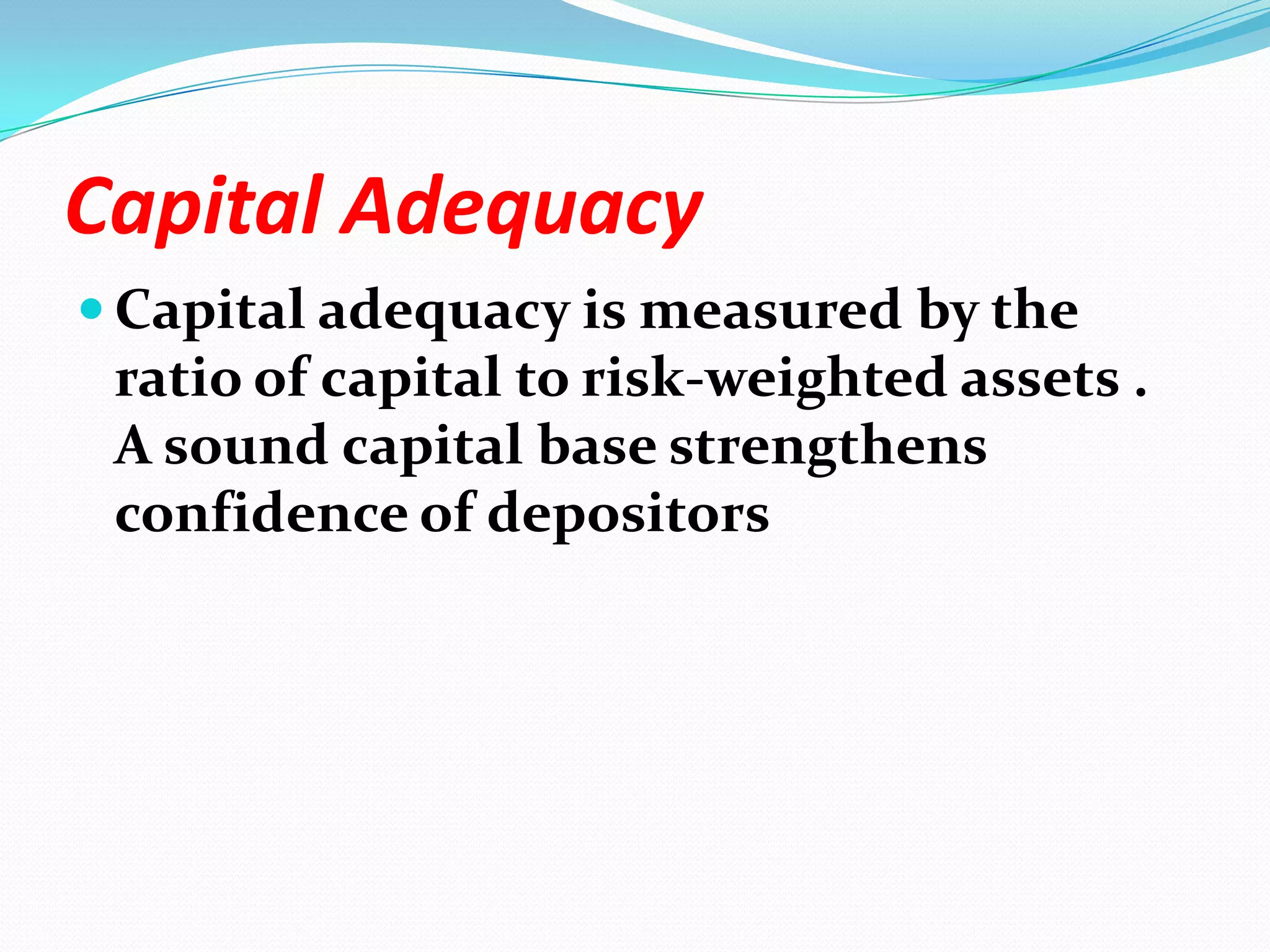

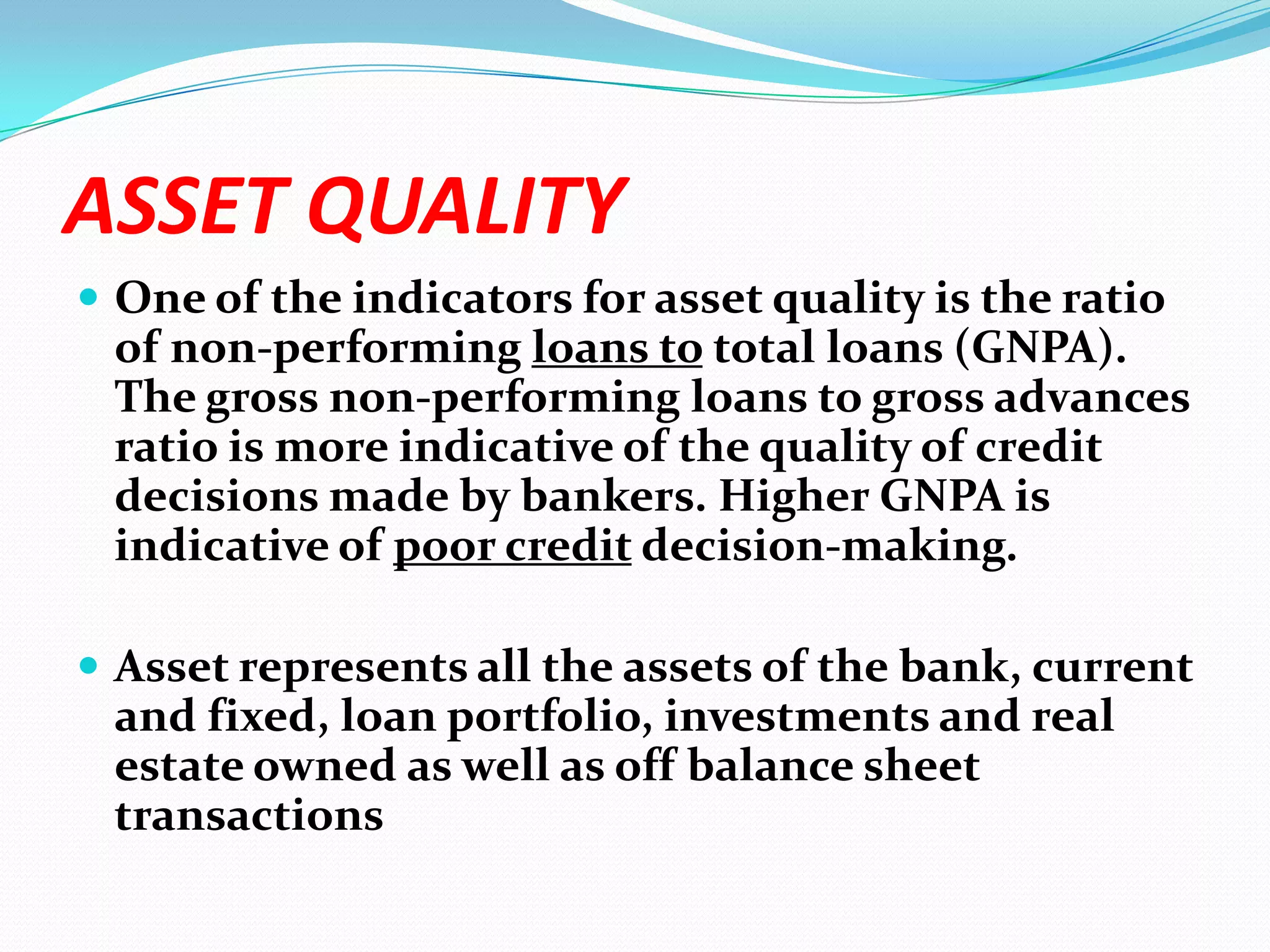

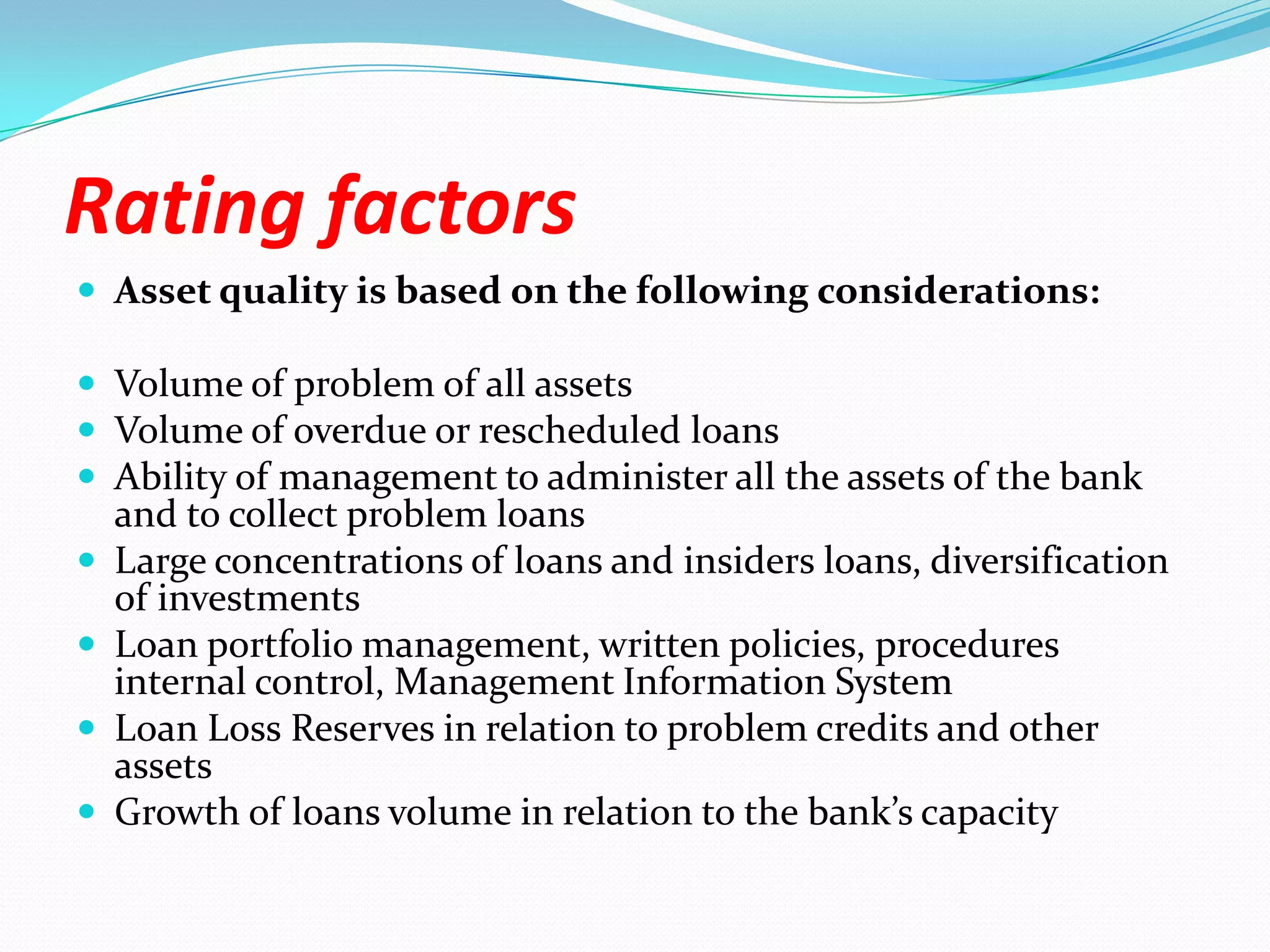

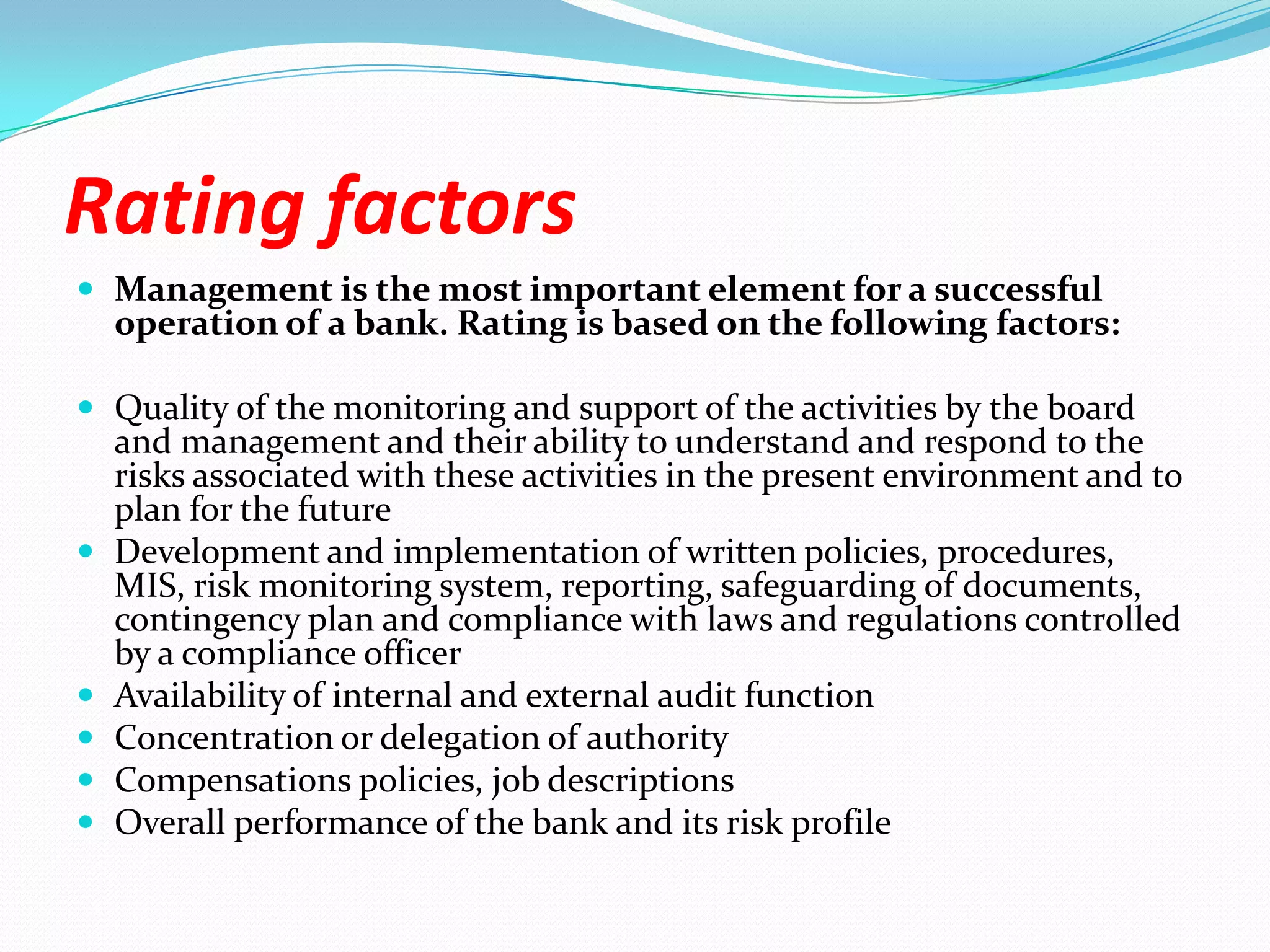

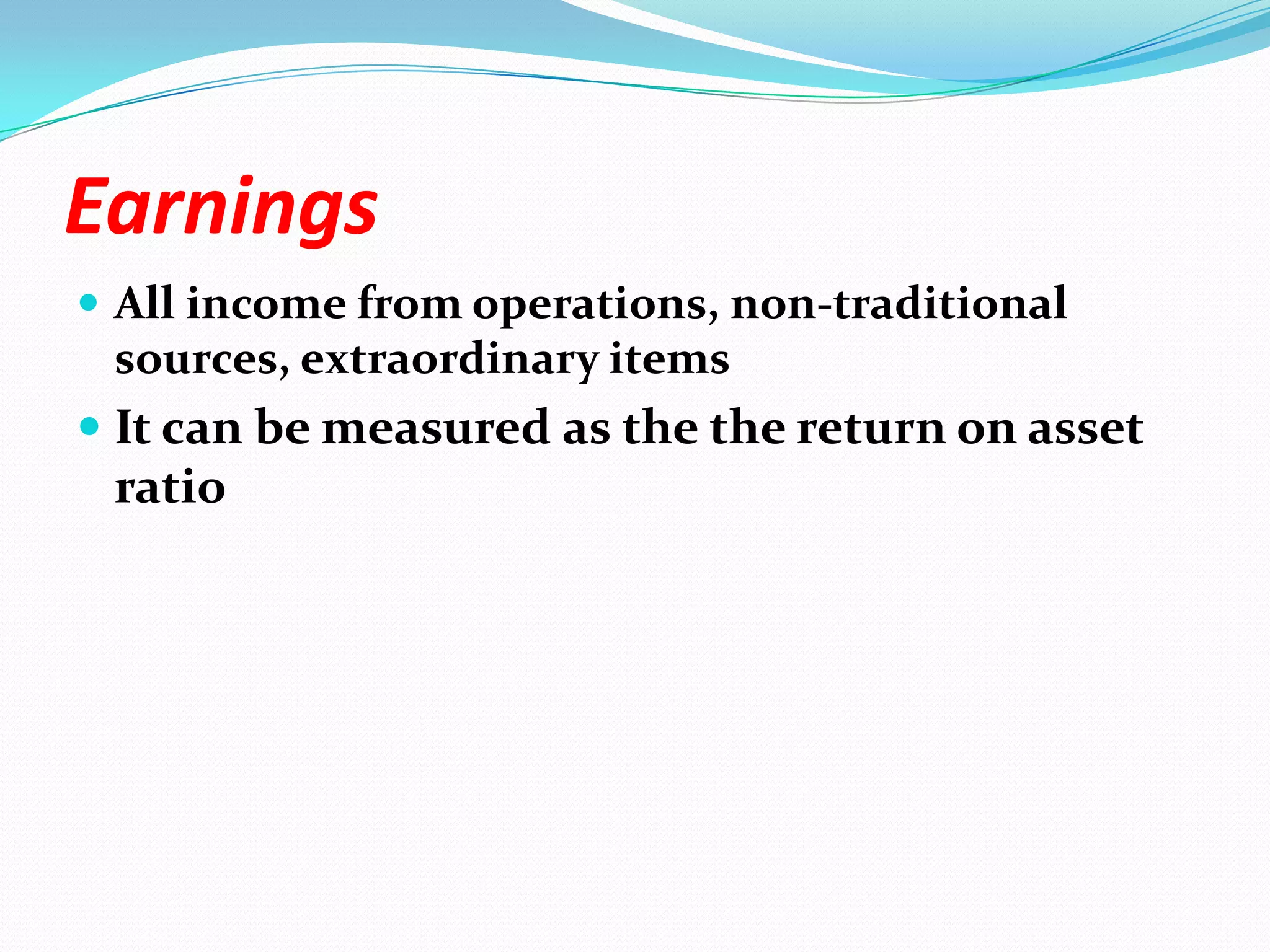

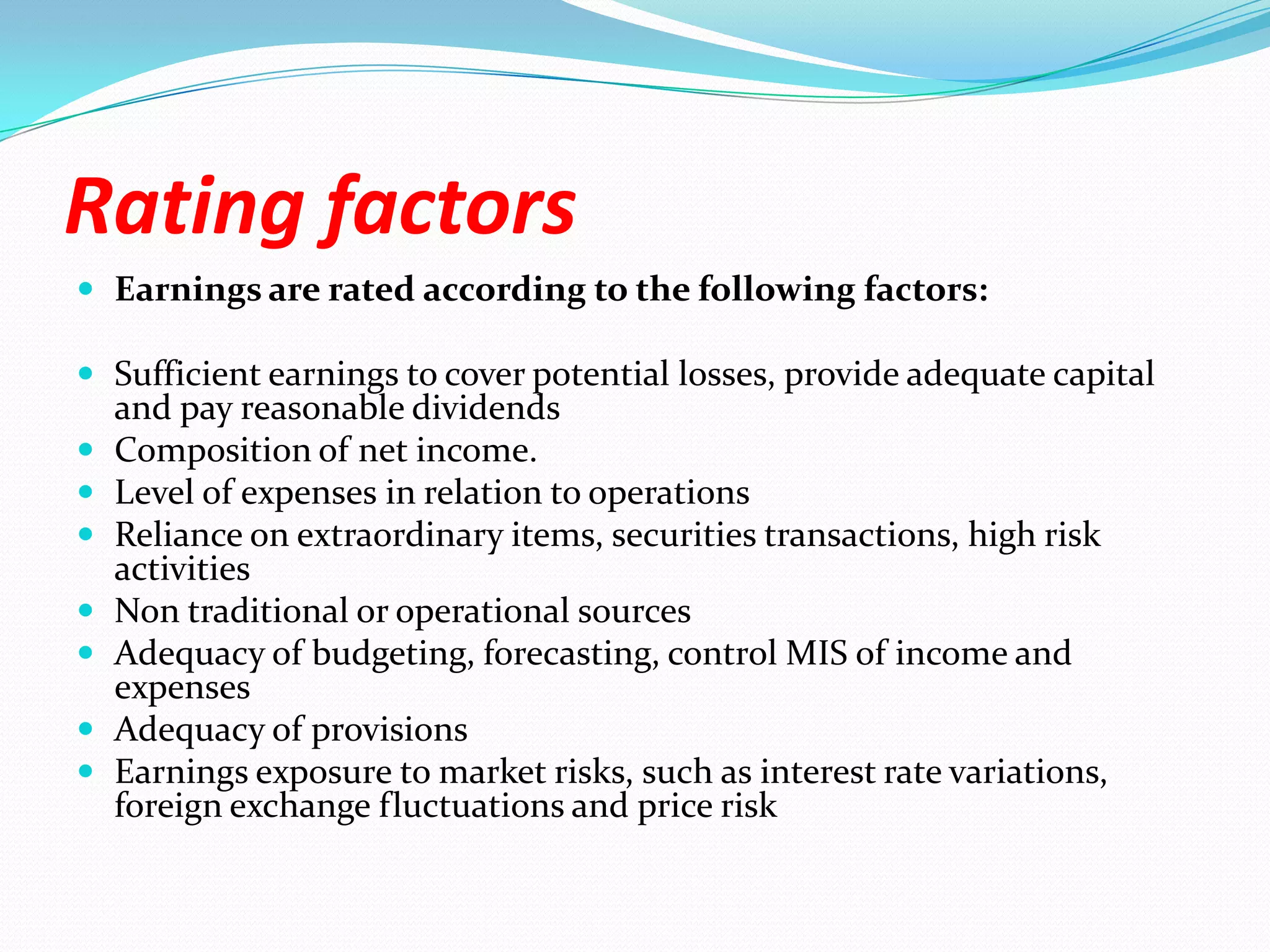

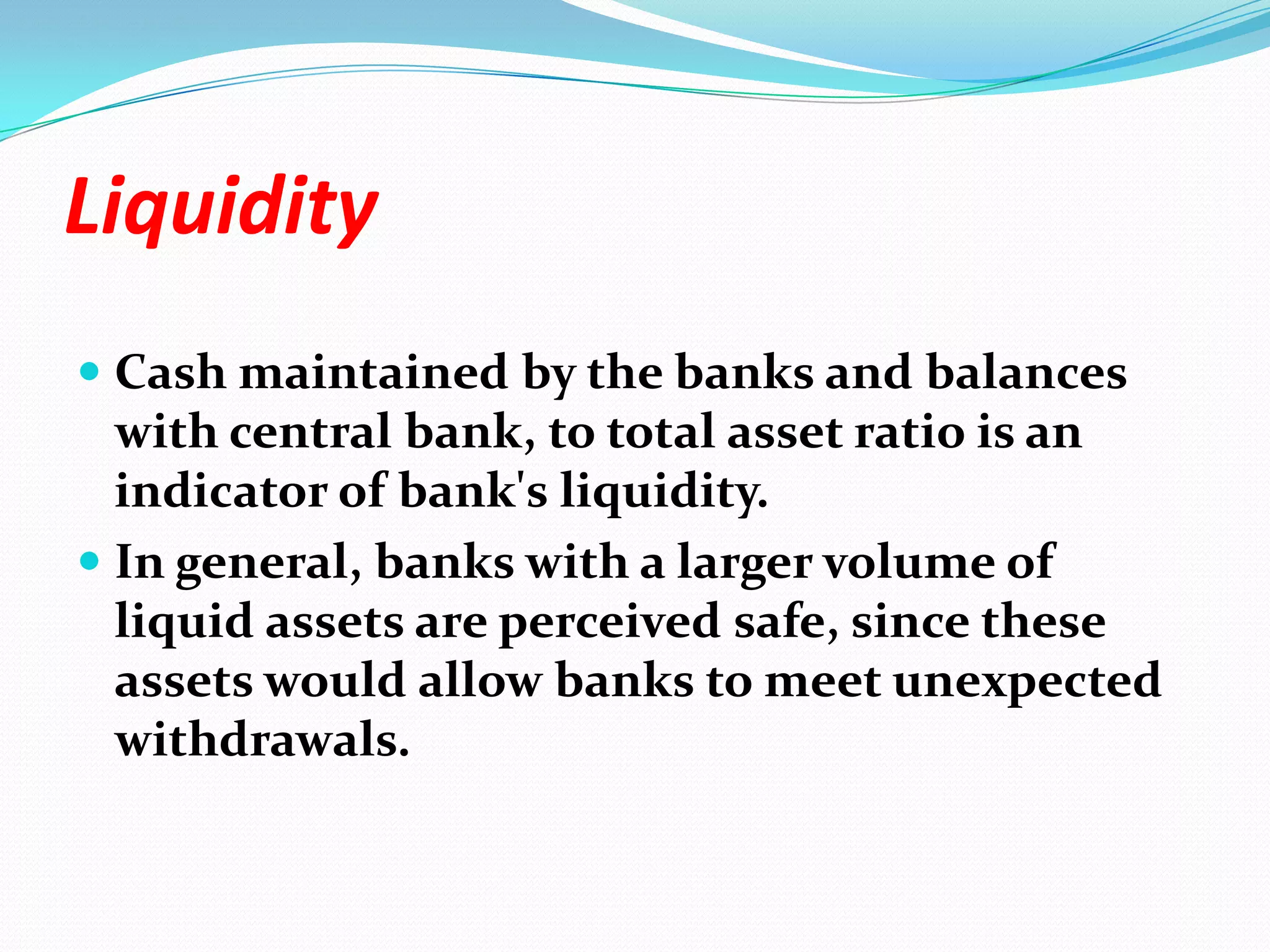

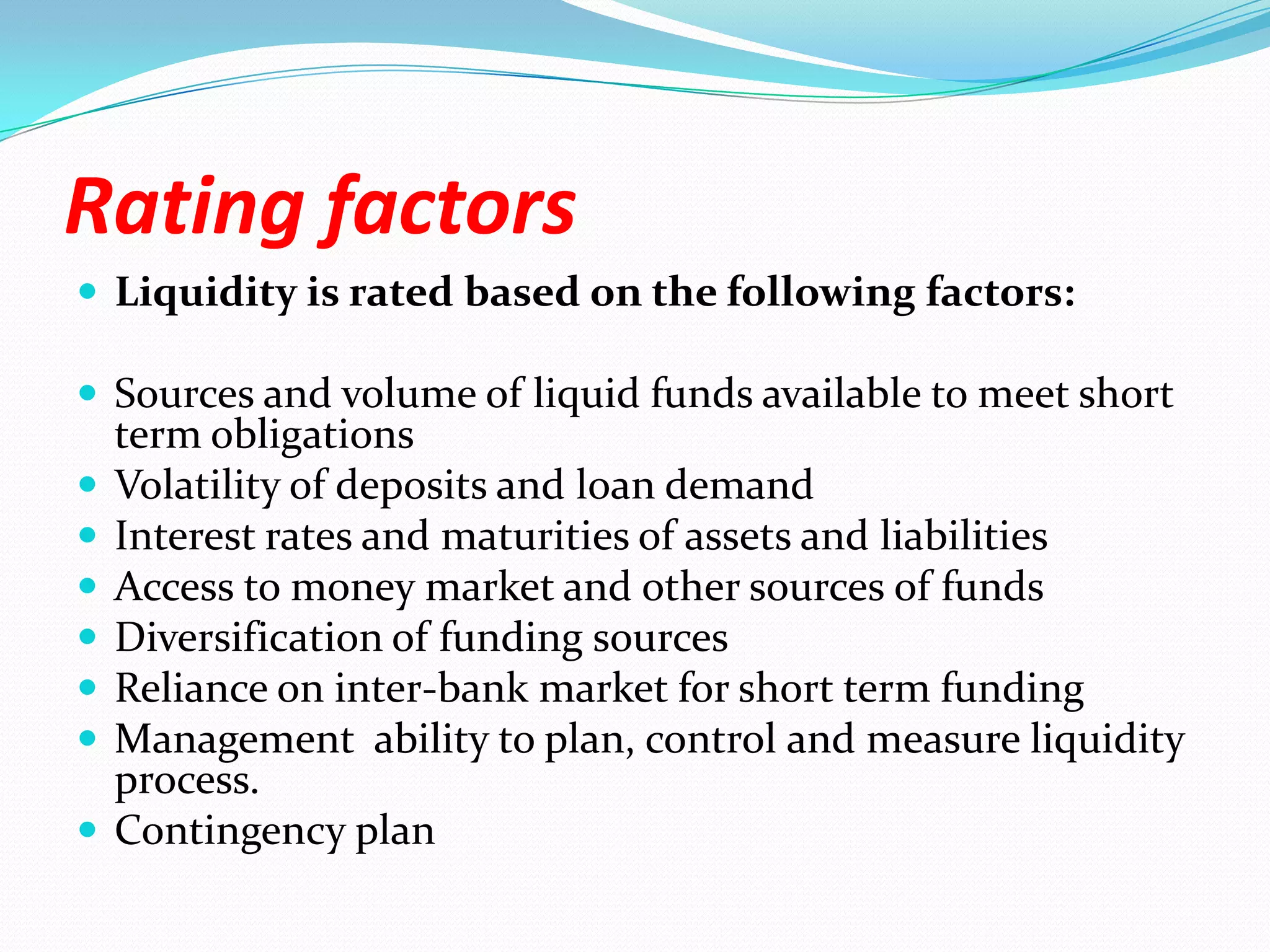

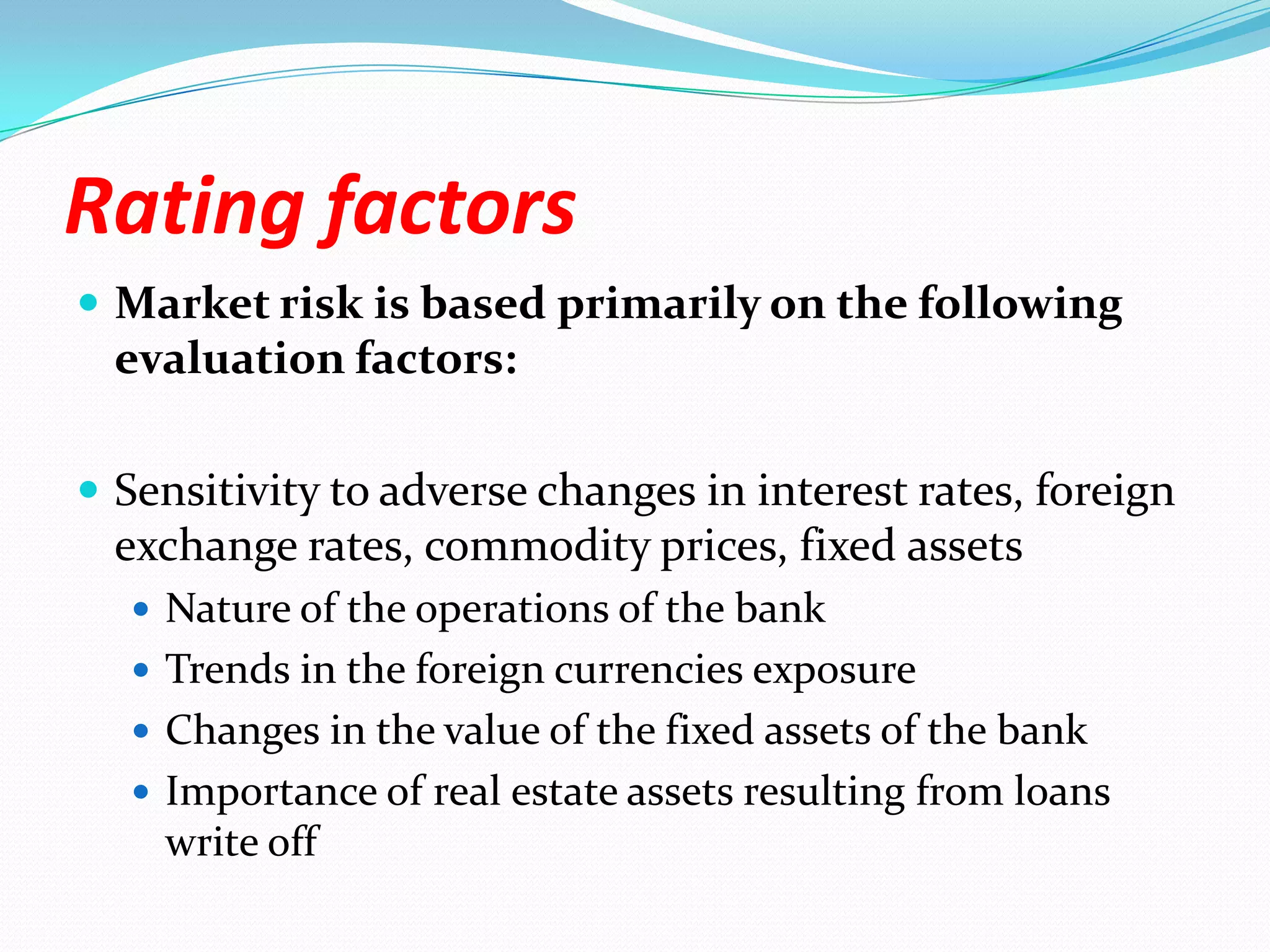

The document discusses CAMELS ratings, which is a system used by banking supervisory authorities to evaluate the financial condition and operations of banks. CAMELS evaluates banks on six components: Capital adequacy, Asset quality, Management, Earnings, Liquidity, and Sensitivity to market risk. Each component is assigned a rating from 1 to 5 based on various factors, with 1 being the best rating and 5 being the worst. The ratings help authorities identify banks needing attention or supervision.