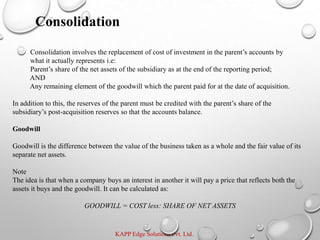

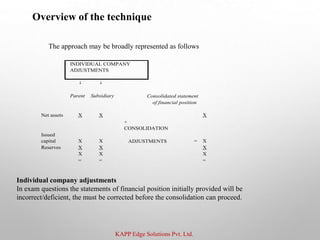

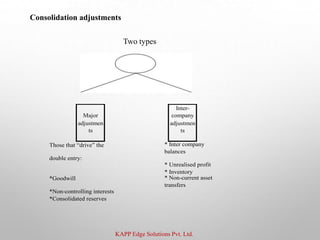

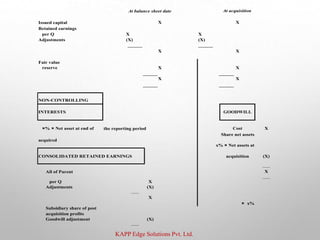

This document discusses consolidated financial statements and the process of consolidation. It defines a group as a parent company that controls one or more subsidiary companies. The key points are: - Consolidated financial statements combine the financial statements of a parent and its subsidiaries to present them as a single entity. - The consolidation process involves replacing the parent's cost of investment with its share of the subsidiary's net assets. It also credits the parent's reserves with its share of the subsidiary's post-acquisition reserves. - Goodwill arises as the difference between the cost of acquisition and the acquirer's interest in the fair value of the identifiable assets acquired and liabilities assumed in a business combination.