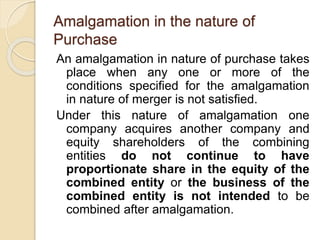

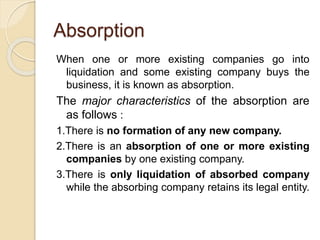

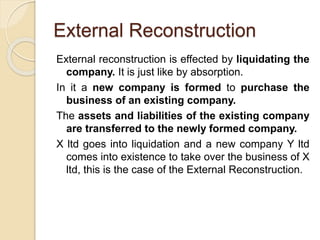

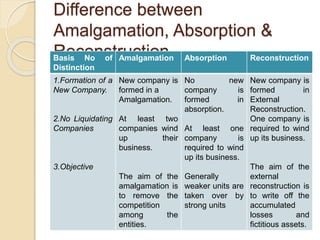

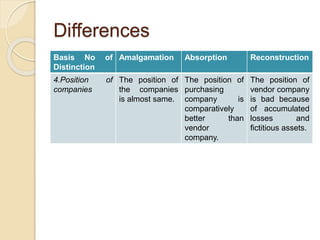

The document discusses amalgamation, absorption, and reconstruction in business combinations. It defines amalgamation as when two or more existing companies go into liquidation and a new company is formed, taking over their businesses. Absorption is when an existing company buys the business of one or more liquidating companies, without forming a new entity. Reconstruction involves an existing company liquidating and a new company being formed to purchase its business. The document outlines the accounting treatments and considerations for different types of business combinations.