The document provides information about financial statements, retained earnings, dividends, stockholders' equity, and valuation of investments. It defines key terms and concepts.

The main points are:

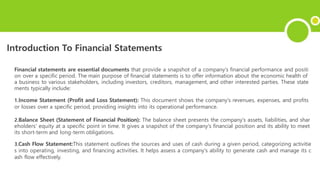

1. Financial statements include the income statement, balance sheet, and cash flow statement and provide information on a company's financial performance and position.

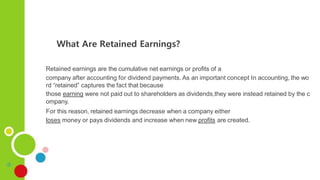

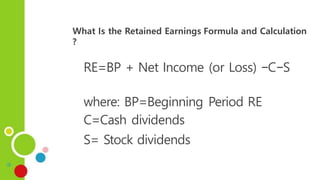

2. Retained earnings represent a company's cumulative net earnings minus any dividends paid out and can be used to expand operations, invest in new products, or repay debt.

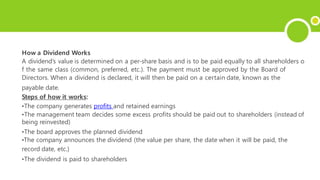

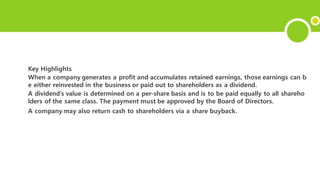

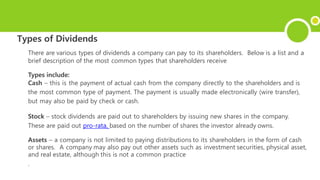

3. Dividends are payments made to shareholders from a company's profits and retained earnings, and must be approved by the board of directors.

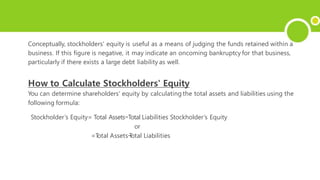

4. Stockholders' equity is calculated