Downloaded 22 times

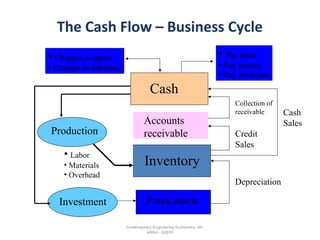

The cash flow statement outlines the cash inflows and outflows of a business, categorized into operating, investing, and financing activities. It highlights the importance of generating positive cash flow from operations for a company's survival and the reliance of financing activities on operational cash generation. The document also provides an illustrative example of the cash flow statement of SABIC, detailing specific figures for different activities over two periods.