Download as ODP, PPTX

![THANKS.... GIVE YOUR SUGGESTIONS AND JOIN AFTERSCHOOOL NETWORK / START AFTERSCHOOOL NETWORK IN YOUR CITY [email_address] PGPSE – WORLD'S MOST COMPREHENSIVE PROGRAMME IN SOCIAL ENTREPRENEURSHIP](https://image.slidesharecdn.com/howtopreparecashflowstatement-100113212521-phpapp02/85/How-To-Prepare-Cash-Flow-Statement-52-320.jpg)

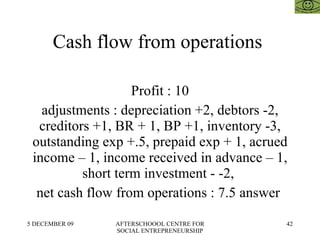

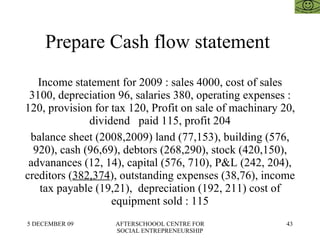

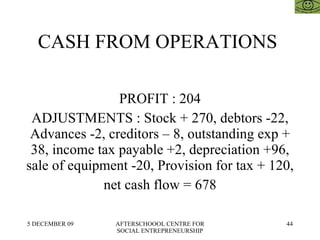

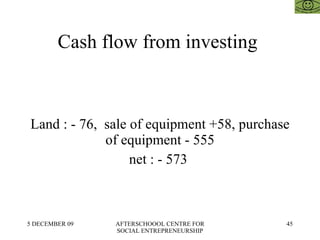

The document provides guidance on how to prepare a cash flow statement. It explains that a cash flow statement shows the inflow and outflow of cash from operating, investing, and financing activities. It discusses identifying cash sources and uses, classifying transactions, and preparing the statement using direct and indirect methods. The key is to distinguish between cash and accrual-based transactions and analyze changes in balance sheet accounts to determine the impact on cash flow.