Download as PDF, PPTX

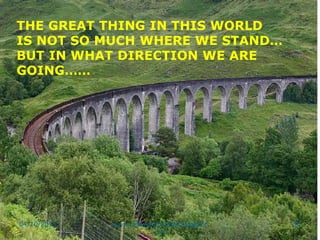

![Cost Per Patient Day

CPPD =

[(Total RNs * 8 hours) * hourly salary +

(Total LVNs * 8 hours) * hourly salary +

(Total NAs * 8 hours) * hourly salary)]

/divided by midnight census

04/10/2015 www.drjayeshpatidar.blogspot

.com

35](https://image.slidesharecdn.com/budget-151004050940-lva1-app6891/85/Budget-35-320.jpg)

The document discusses several key aspects of budgeting for nursing services, including: 1) The importance of nursing leaders having budgeting knowledge to efficiently manage operations and meet financial targets. 2) The different types of budgets including operating, revenue, and expense budgets and how they are used. 3) Factors to consider when creating a nursing budget, such as variable costs, staffing needs, and volume projections. 4) The process of analyzing variances between budgeted and actual costs and examining factors that contributed to differences.