Downloaded 1,242 times

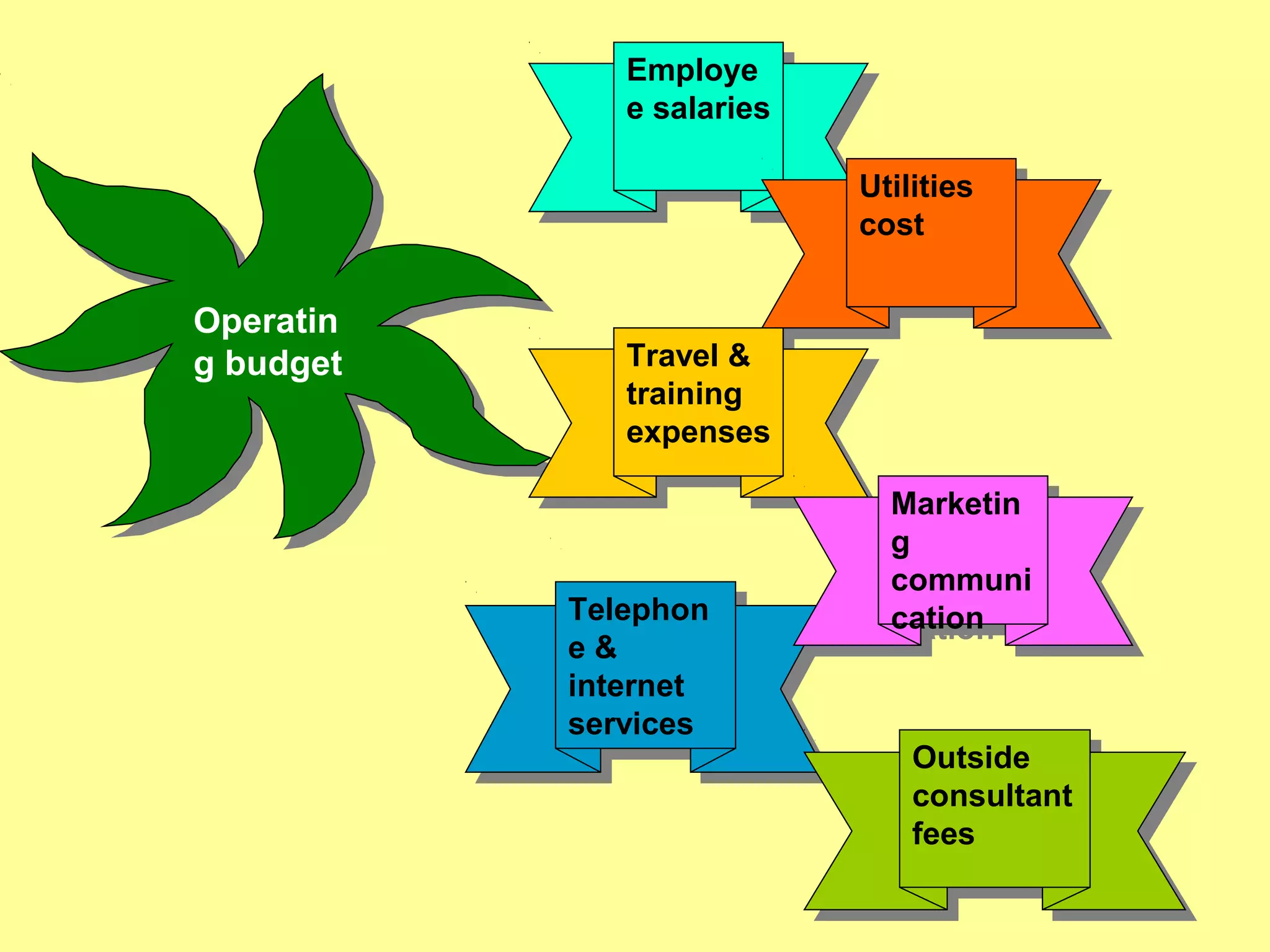

This document discusses various aspects of fiscal planning in nursing management. It describes the steps involved in fiscal planning including developing a plan, assessing needs, evaluation, and implementation. It highlights that nursing budgets account for a large share of healthcare expenses, making fiscal planning an important tool. Some key aspects covered are types of budgets (capital, revenue, operating), budgeting approaches like zero-based budgeting, and fiscal terms like revenue deficit. The document provides advice on integrating leadership roles and management functions into effective fiscal planning.

![Organizational Structure Of A Hospital[1]](https://cdn.slidesharecdn.com/ss_thumbnails/organizationalstructureofahospital1-100104091259-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)