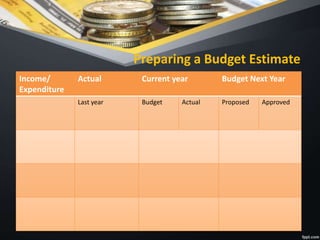

The document outlines the importance and components of budgeting in nursing management, highlighting the necessity for a financial plan to coordinate resources for healthcare services. It details various budget types, including capital, operating, personal, and cash budgets, along with methods for estimating and justifying expenses. The role of the nurse manager is emphasized in preparing and managing the budget, ensuring adequate funds, and maintaining financial accountability.