Downloaded 32 times

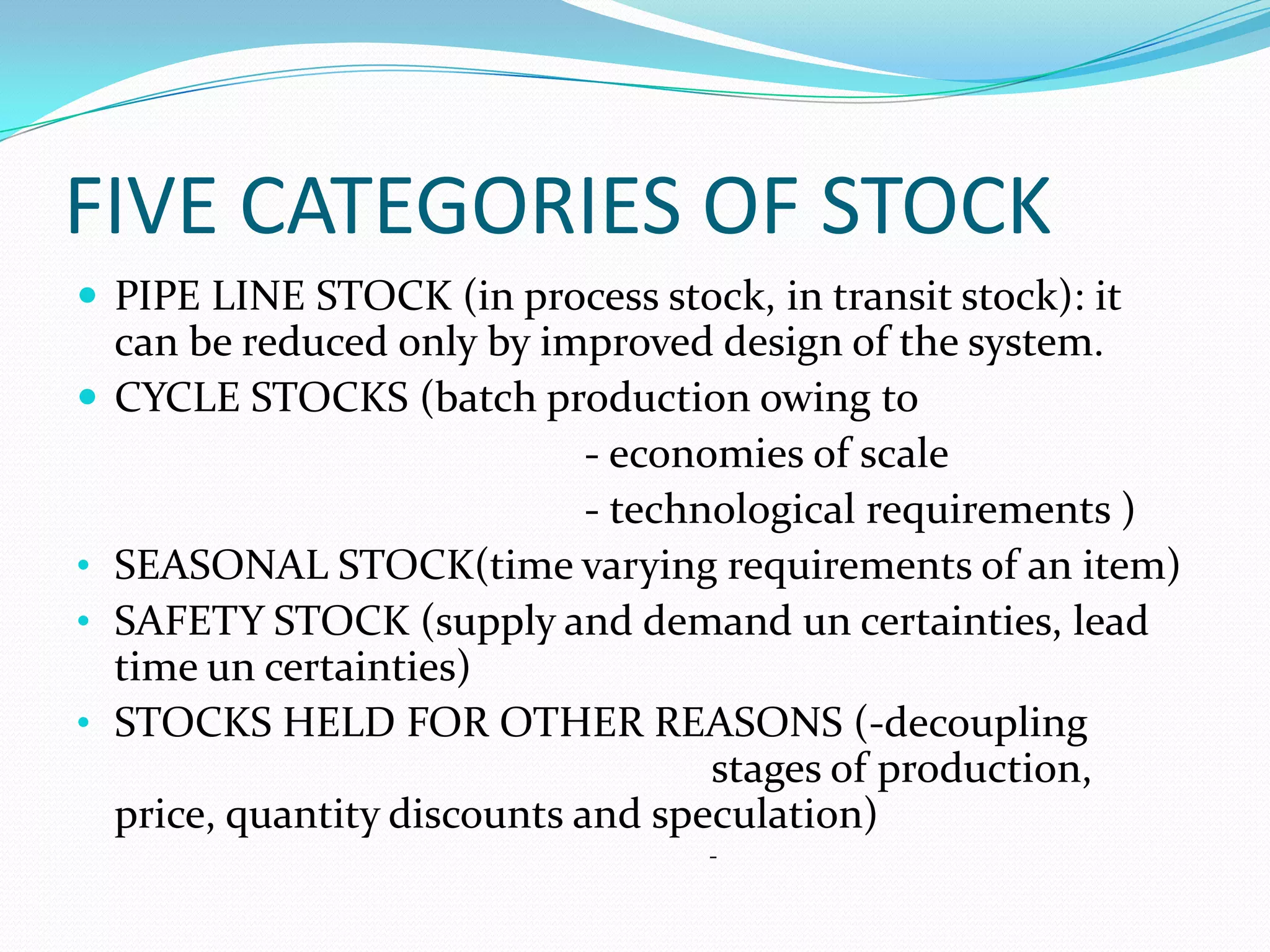

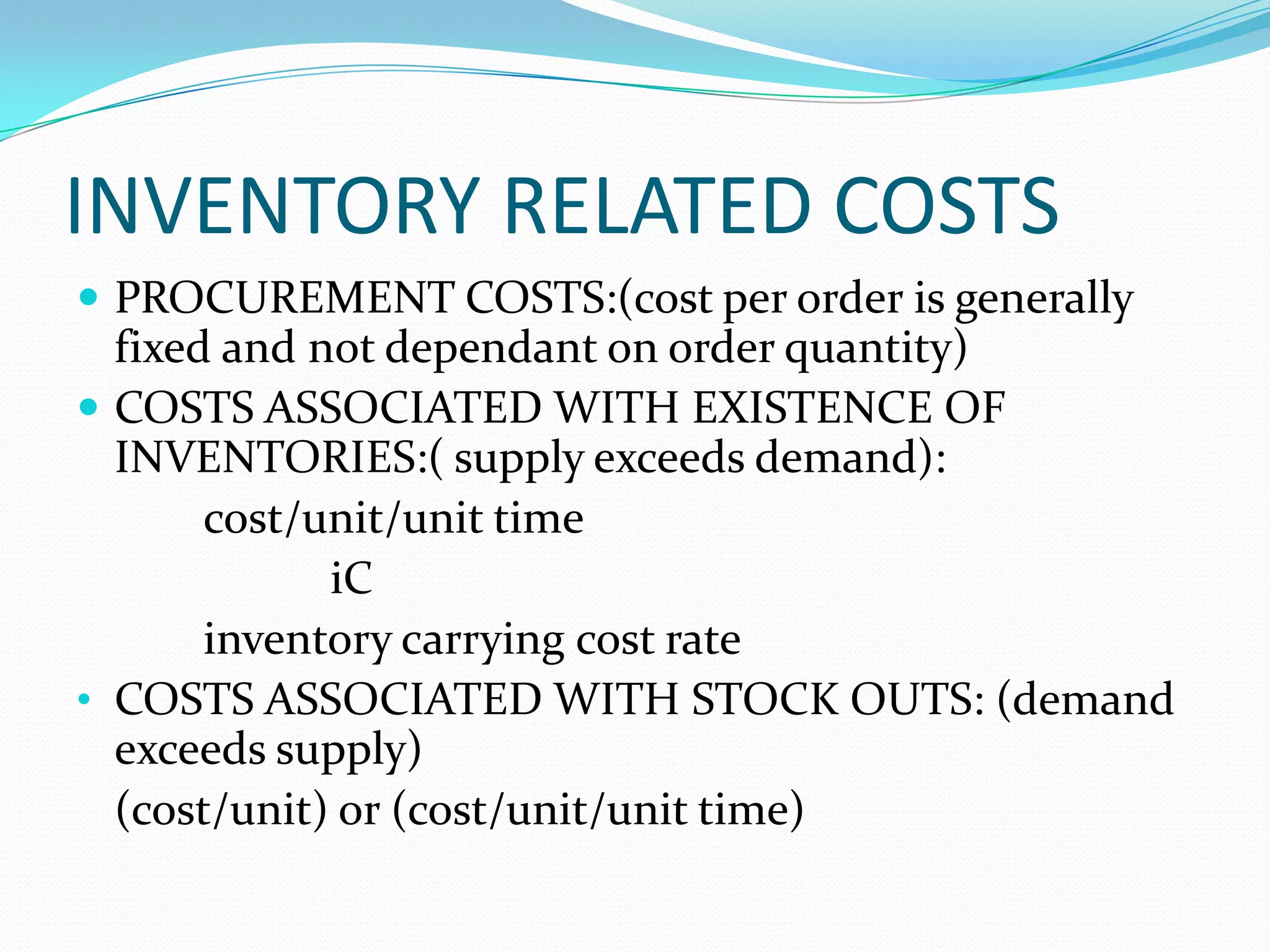

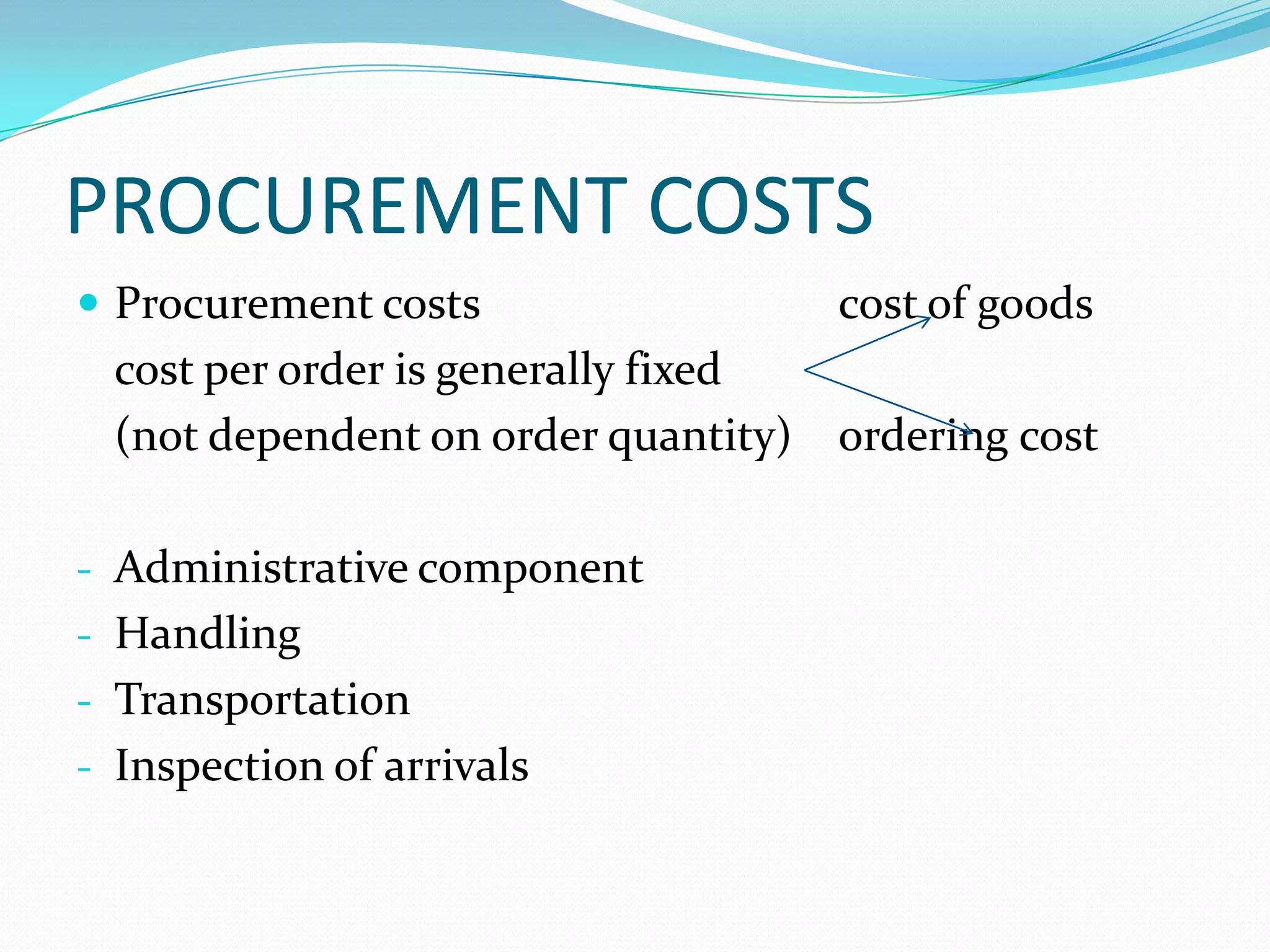

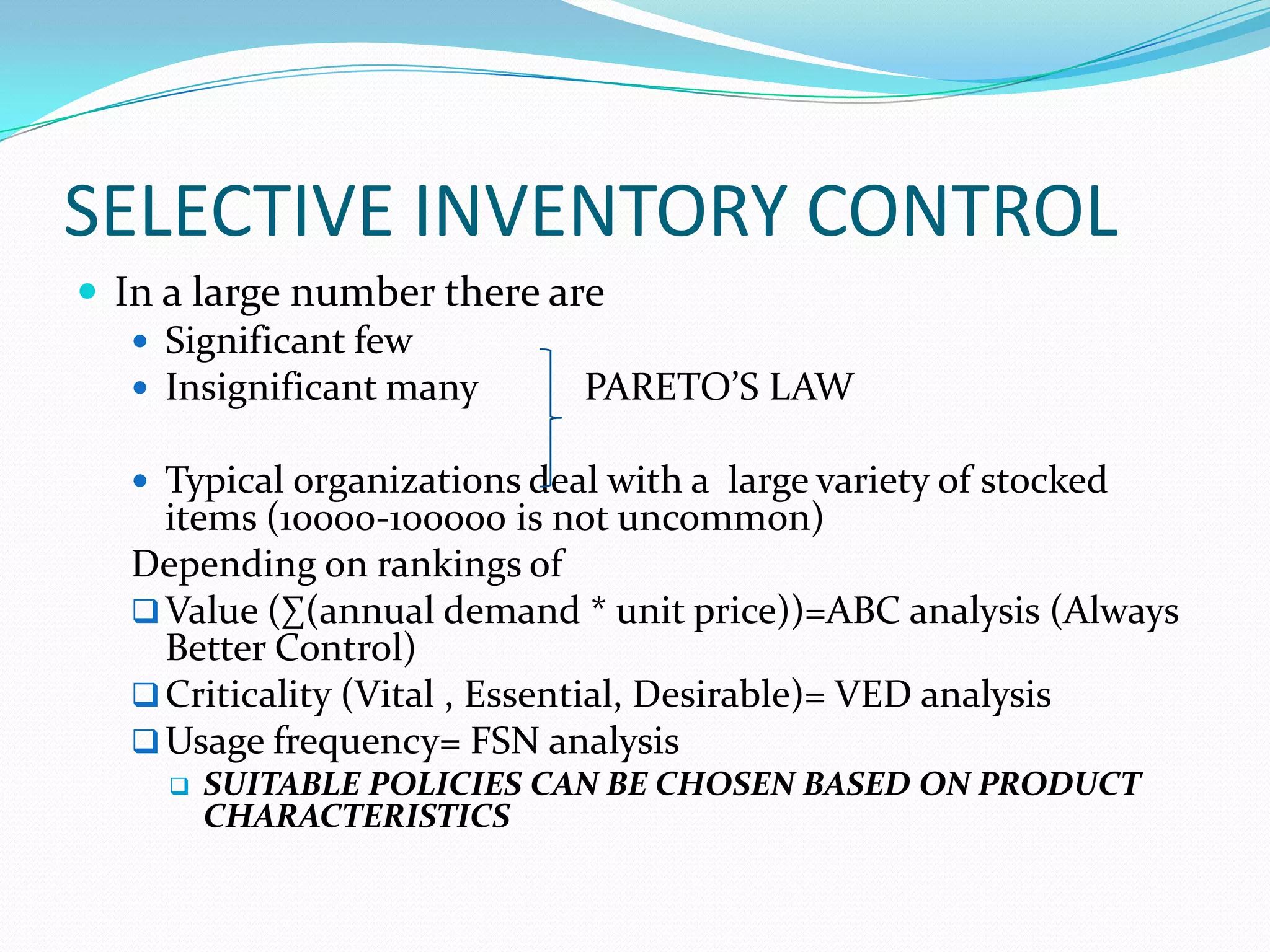

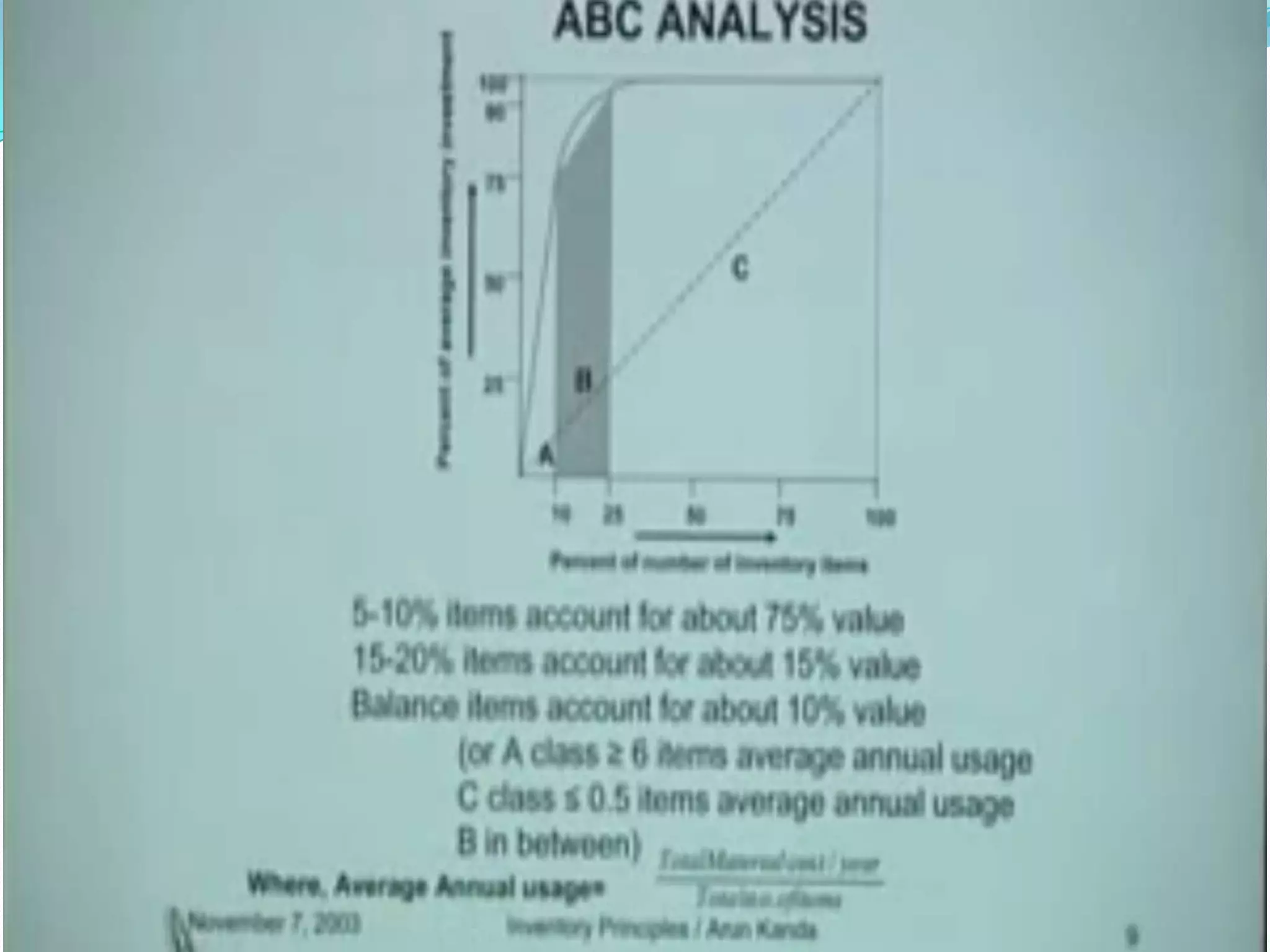

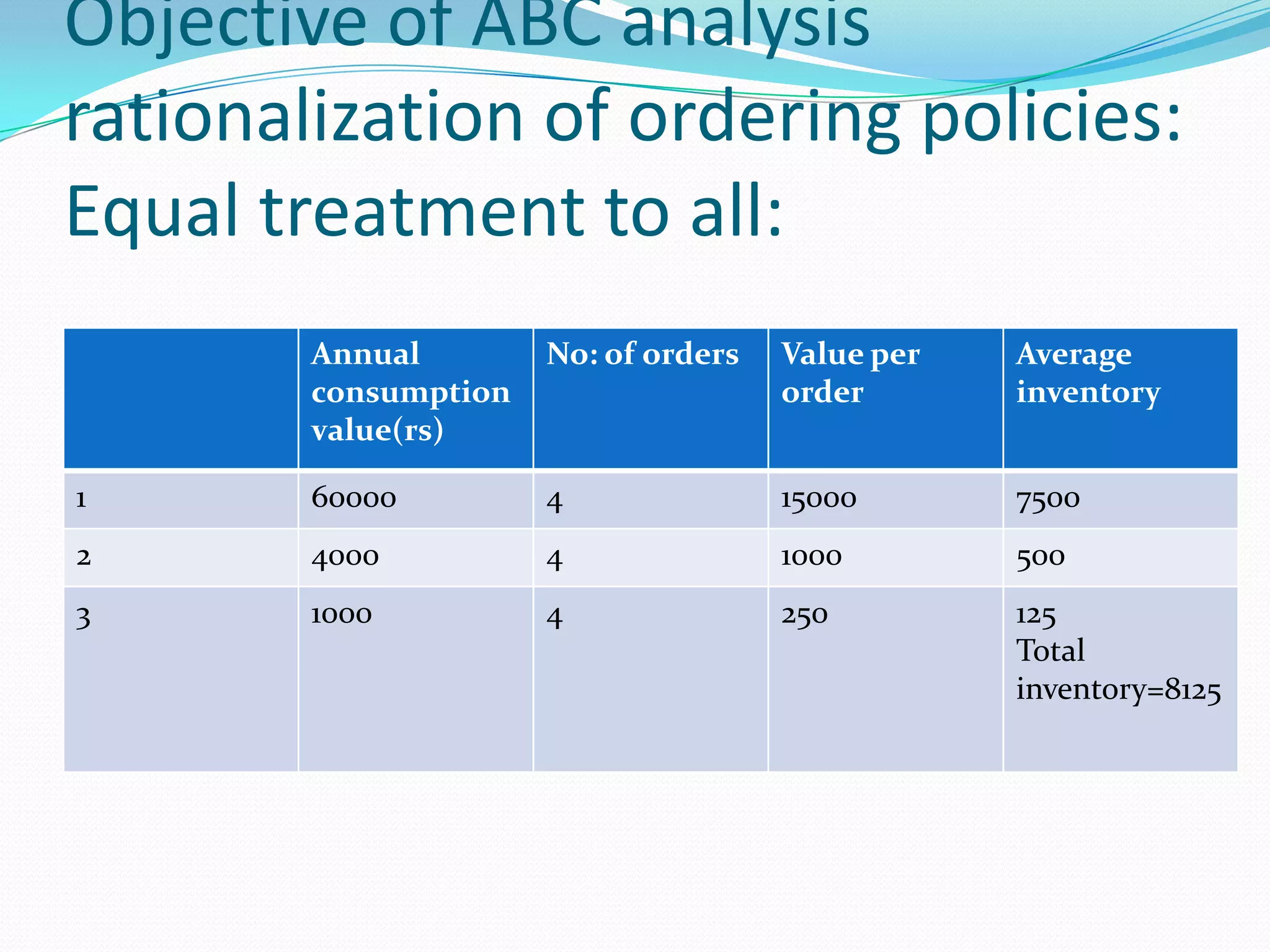

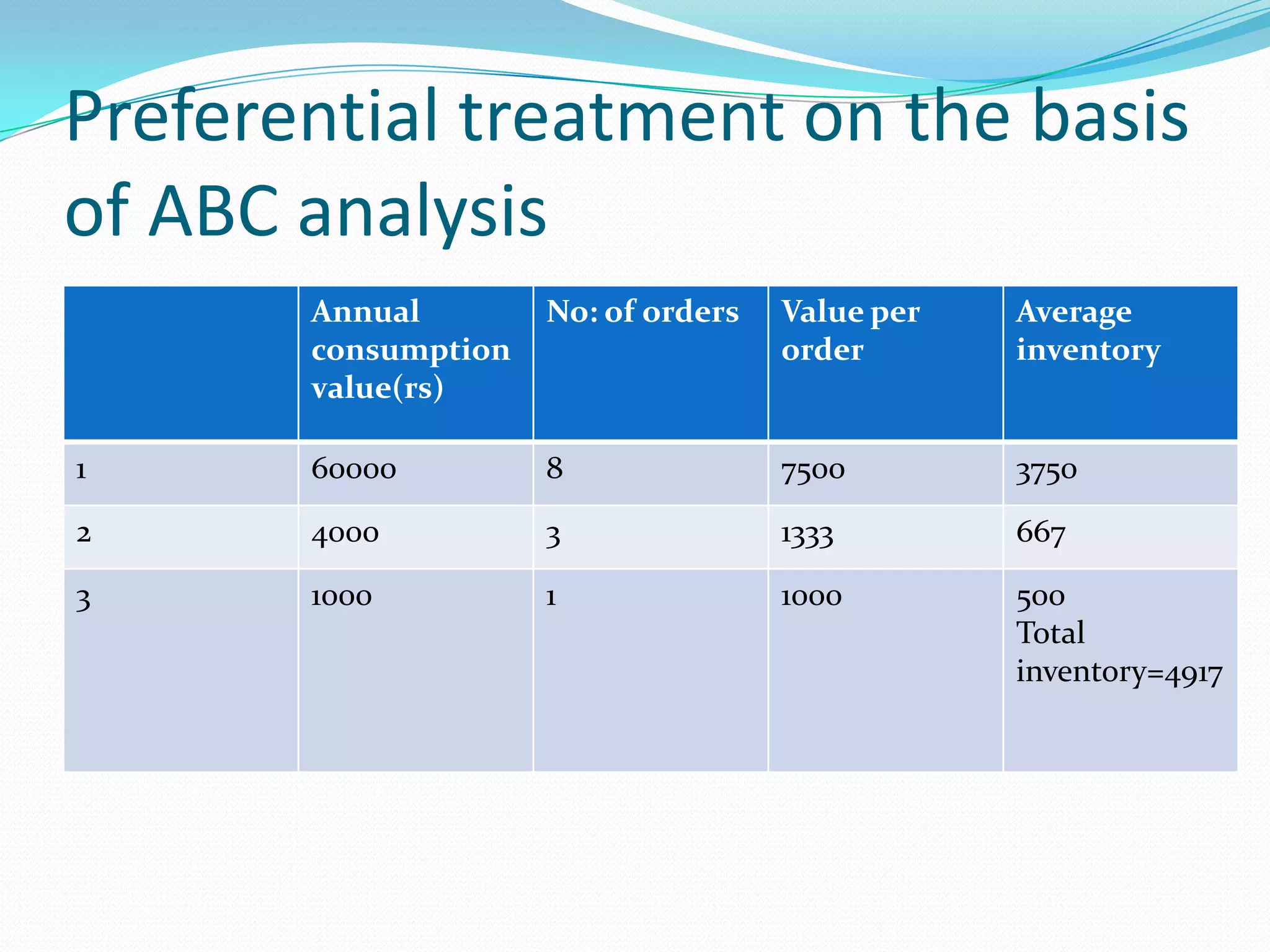

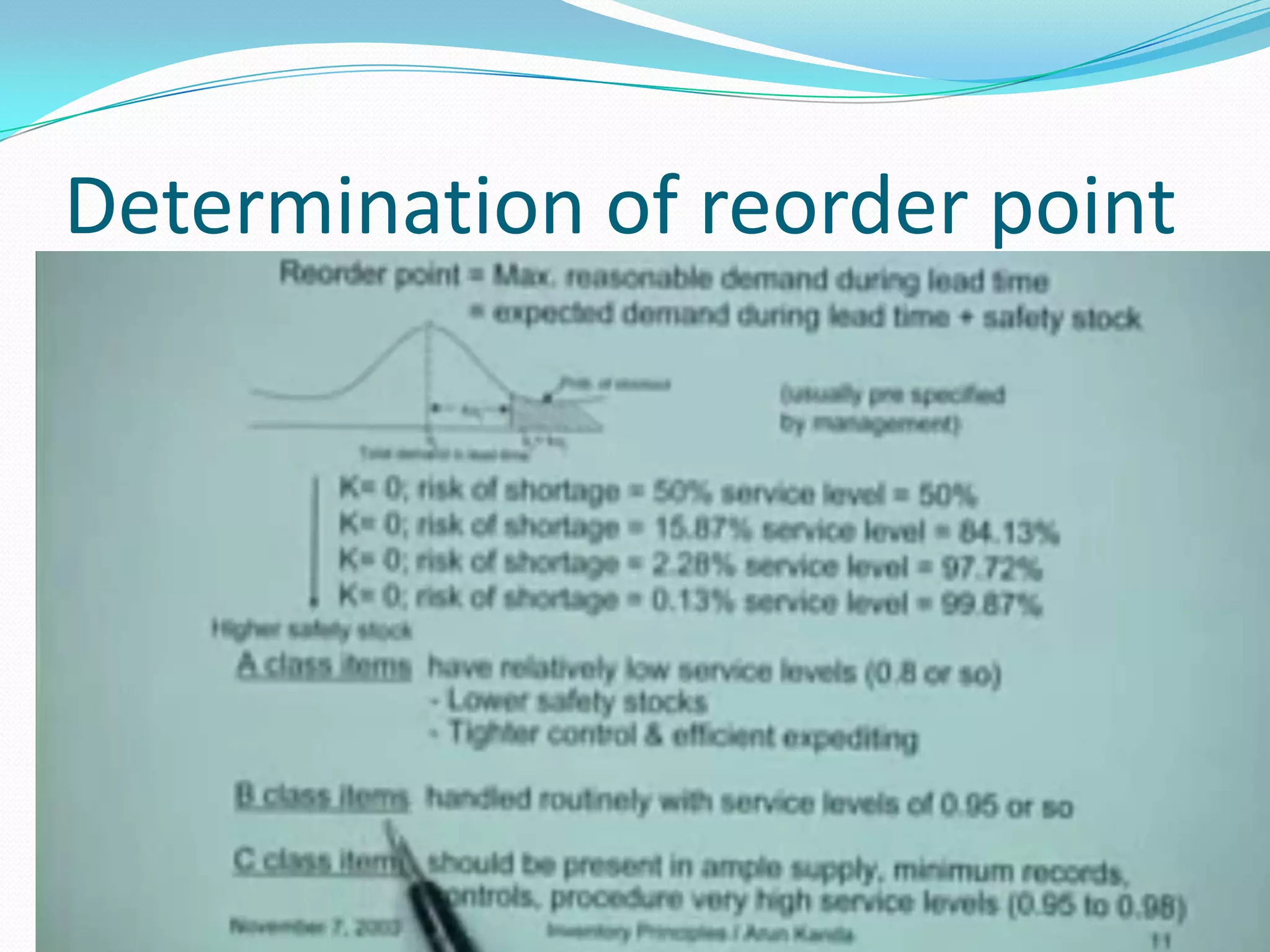

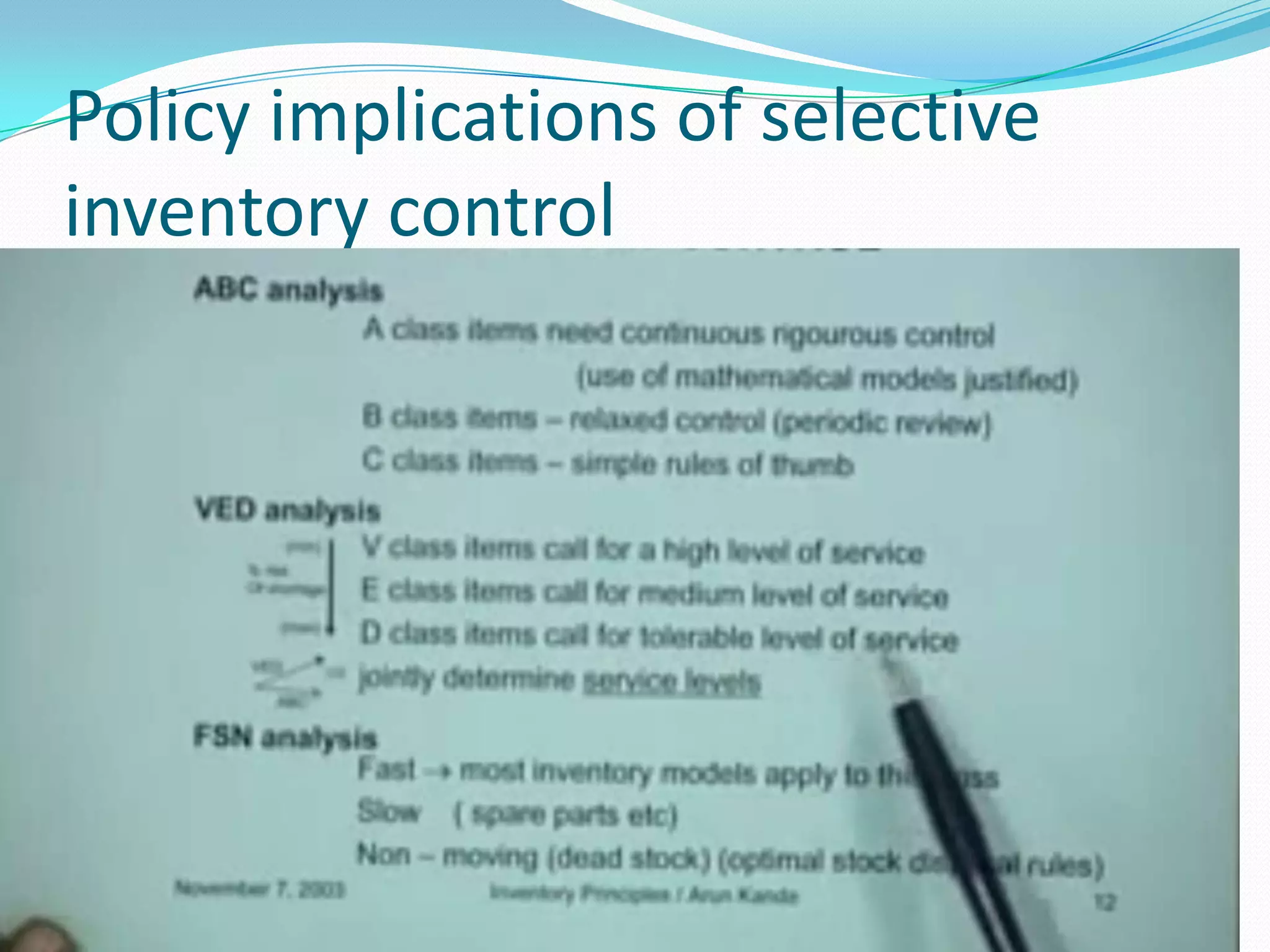

This document discusses inventory functions and costs. It describes five categories of stock: pipeline, cycle, seasonal, safety, and other. Inventory costs include procurement costs which are generally fixed per order, inventory holding costs which are the cost per unit per time period, and stockout costs when demand exceeds supply. The document advocates for selective inventory control using ABC analysis to prioritize items based on annual consumption value and tailor inventory policies accordingly in order to minimize total inventory costs.