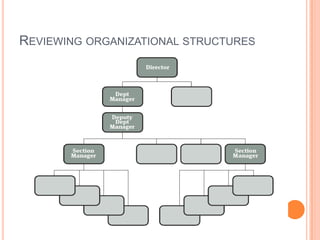

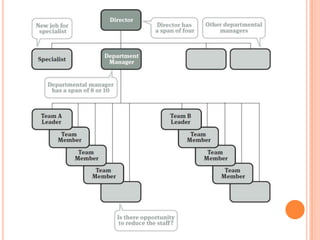

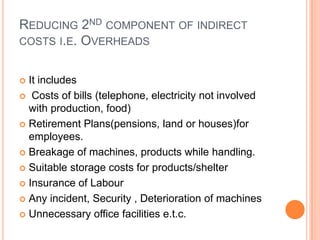

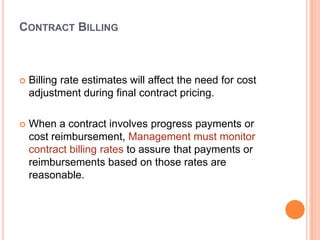

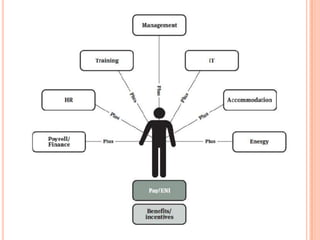

This document discusses ways to reduce indirect costs in manufacturing industries. It defines direct and indirect costs, with the latter including overhead expenses like administration, utilities, and insurance. The document recommends systematically reviewing organizational structures and staffing to identify unnecessary roles and layers. It also suggests improving technology use, evaluating capabilities, reshaping functions, consolidating services, and monitoring billing rates and benefits costs to further reduce indirect expenses. With tighter indirect cost management, the document argues that manufacturers can lower overall costs and gain a competitive advantage in the market.