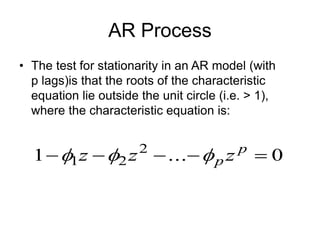

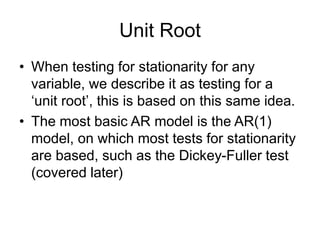

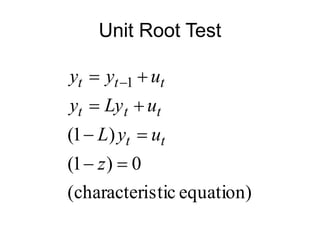

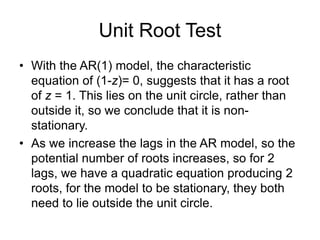

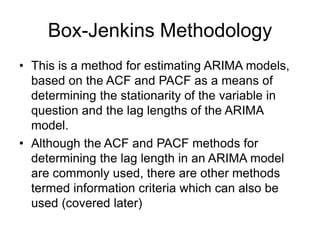

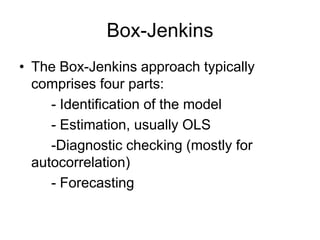

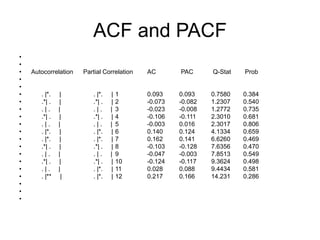

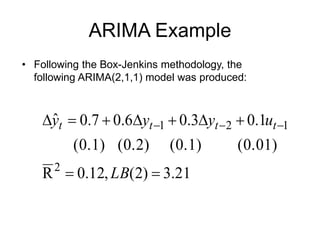

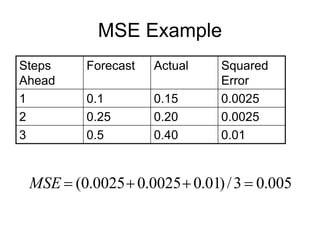

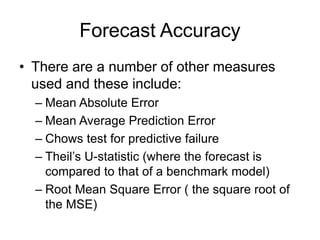

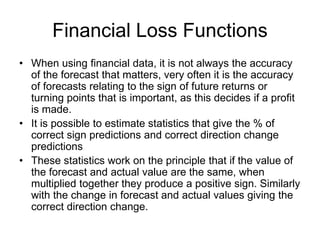

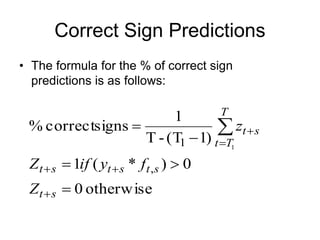

This document discusses ARIMA modelling and forecasting. It covers the Box-Jenkins methodology, which involves identifying the appropriate ARIMA model through examining the ACF and PACF, estimating the model, checking diagnostics, and forecasting. The document also discusses evaluating forecasts through measures like mean squared error and assessing whether models accurately predict turning points for financial data.

![ARIMA Models - [Lab 3]](https://cdn.slidesharecdn.com/ss_thumbnails/ydqcxn5vtqizjoun2as1-signature-e1de5ad681d661531c2467ca0d3e475440809ccfdbcb78c5369a1bb749945888-poli-141230090527-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)