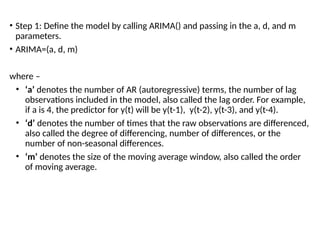

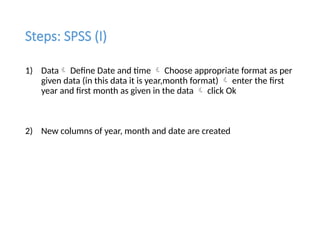

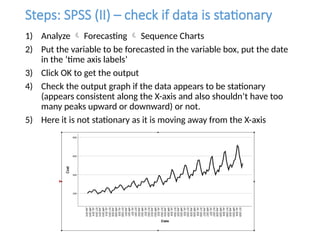

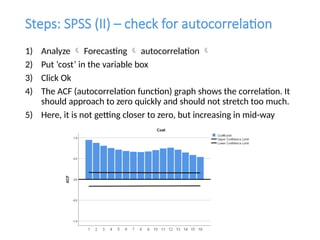

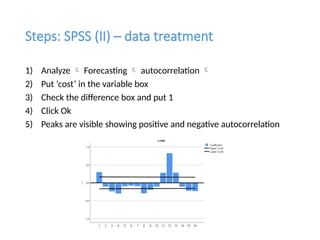

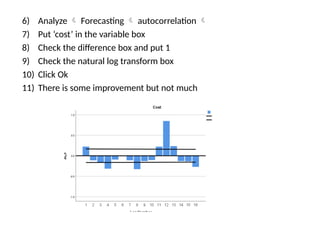

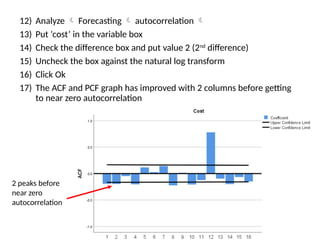

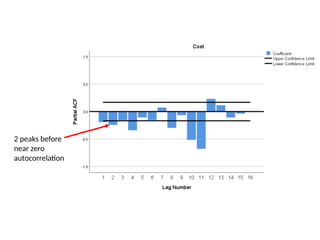

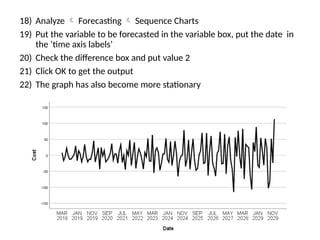

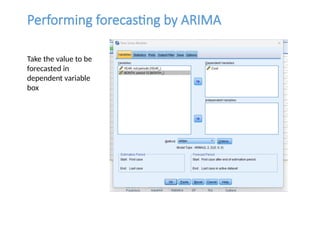

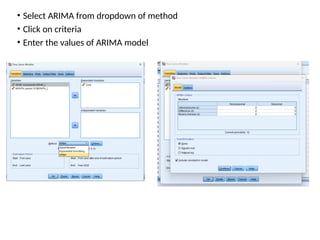

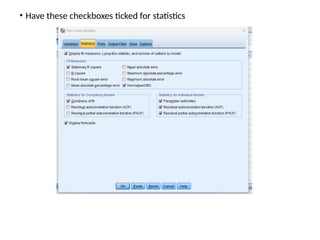

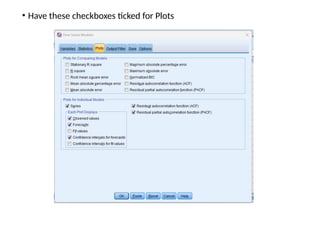

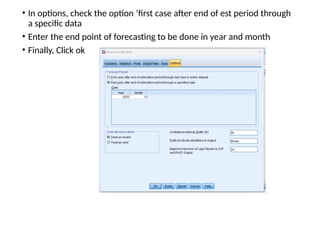

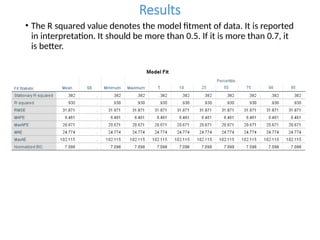

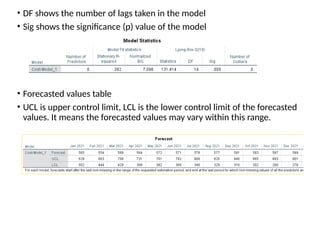

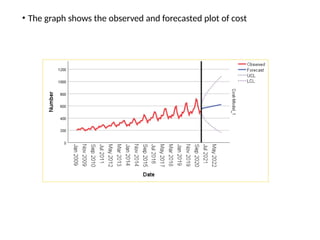

The document discusses forecasting HR costs using time series modeling, particularly the ARIMA method, essential for strategic managerial decision-making. It details the components of HR costs and outlines the steps in applying SPSS for checking data stationarity, autocorrelation, and performing the ARIMA forecast. The final results include model fit metrics, significance values, and forecasted cost ranges.

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)