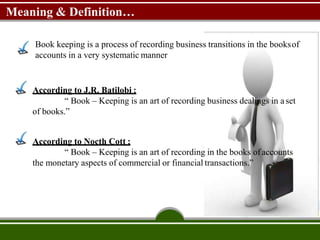

1. Bookkeeping is the process of recording business transactions in a systematic manner through journals, ledgers, and trial balances. It aims to keep permanent records, determine profits and losses, and know the financial position of the business.

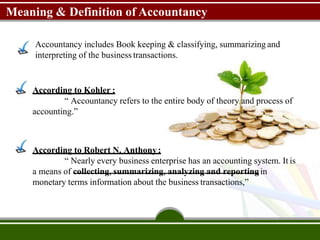

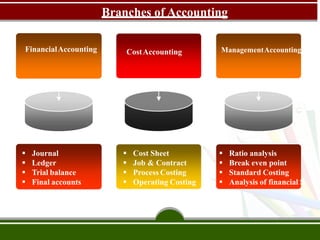

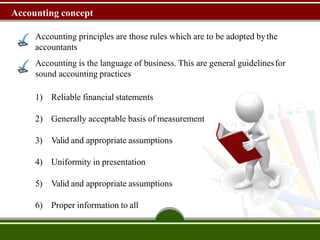

2. Accounting includes classifying, summarizing, and interpreting bookkeeping records to provide useful financial information. It has branches like financial, cost, and management accounting.

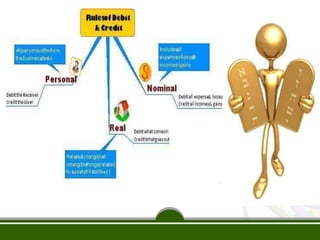

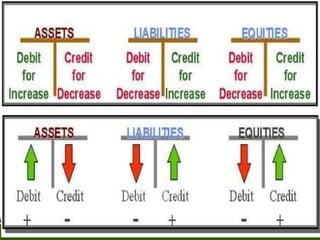

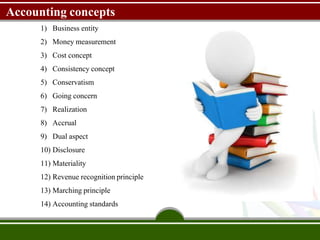

3. Key accounting concepts include the business entity, money measurement, cost, matching, dual aspect, realization, and consistency principles.