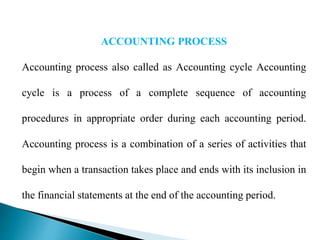

The document outlines the accounting process, also known as the accounting cycle, which consists of a series of steps beginning with the identification and analysis of business transactions and concluding with the preparation of financial statements. It details the stages of recording transactions in journals, posting to ledgers, balancing accounts, and preparing a trial balance, which serves as a basis for the final financial statements including the trading, profit and loss account, and balance sheet. This process ensures accurate financial reporting and reflects the financial position of a business.