Downloaded 81 times

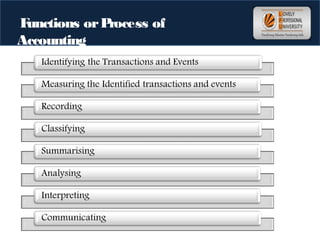

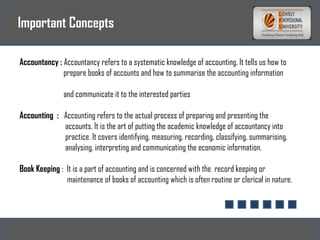

Accounting is the process of identifying, measuring, recording, classifying, summarizing, analyzing, interpreting and communicating financial information about an entity. It involves recording economic events which affect the financial position and performance of a business. The key functions of accounting include identifying transactions, measuring transactions in monetary terms, recording transactions methodically in books of accounts, classifying transactions into appropriate accounts, summarizing transactions periodically into financial statements, analyzing trends and relationships, interpreting financial statements for decision making and communicating essential information to users.