Download to read offline

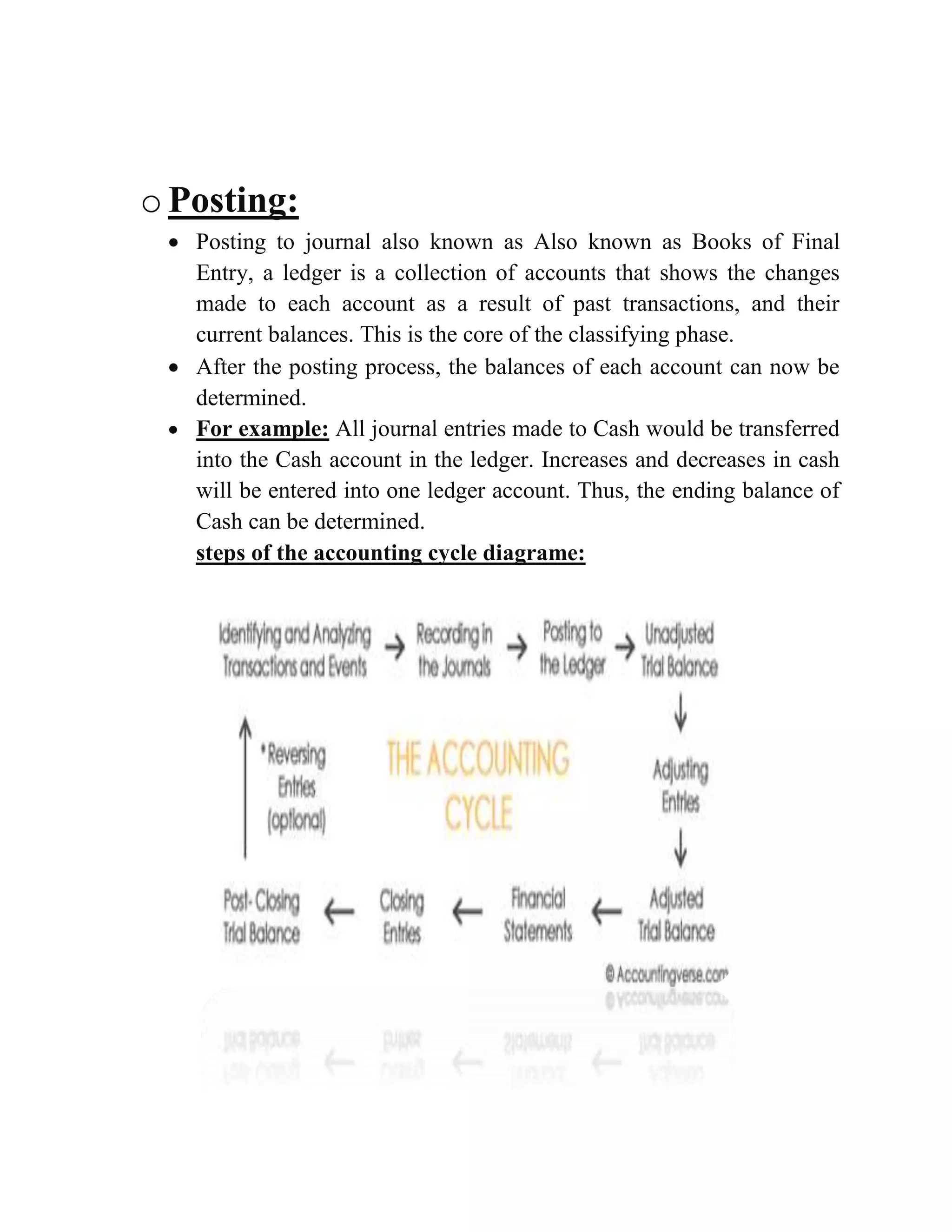

The accounting cycle refers to the series of steps involved in recording business transactions and producing financial statements. The key steps are: 1) identifying transactions and preparing source documents, 2) recording transactions in journals using double-entry bookkeeping, and 3) posting transaction details from journals to individual accounts in the ledger to accumulate balances over time. This process allows a business to track the financial effects of transactions and produce accurate financial statements.