Downloaded 24 times

![Definition

According to the American Institute of Certified Public

Accountants [AICPA];

“Accounting is the art of recording, classifying and

summarizing in a significant manner and in terms of money,

transactions and events, which are, in part at least, of a

financial character and interpreting the result thereof.”](https://image.slidesharecdn.com/accountingcycle-171223154319/85/Accounting-cycle-a-bird-eye-view-b-4-320.jpg)

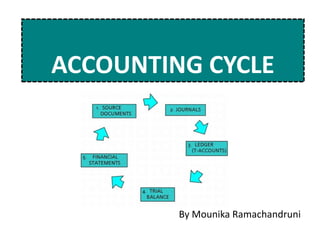

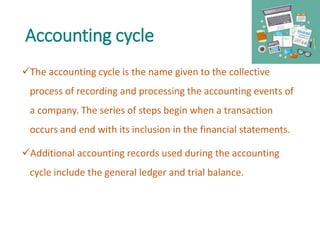

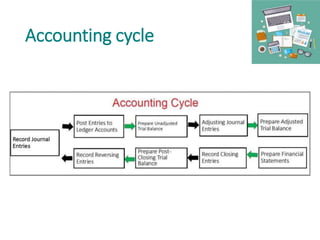

The accounting cycle summarizes the process of recording accounting transactions from occurrence through to financial statements. It begins with journal entries to record transactions, followed by posting to ledger accounts. An adjusted trial balance is prepared after adjusting entries. Financial statements are then prepared, followed by closing entries and a post-closing trial balance. The accounting cycle ensures all transactions are recorded, summarized and reported accurately.