Download to read offline

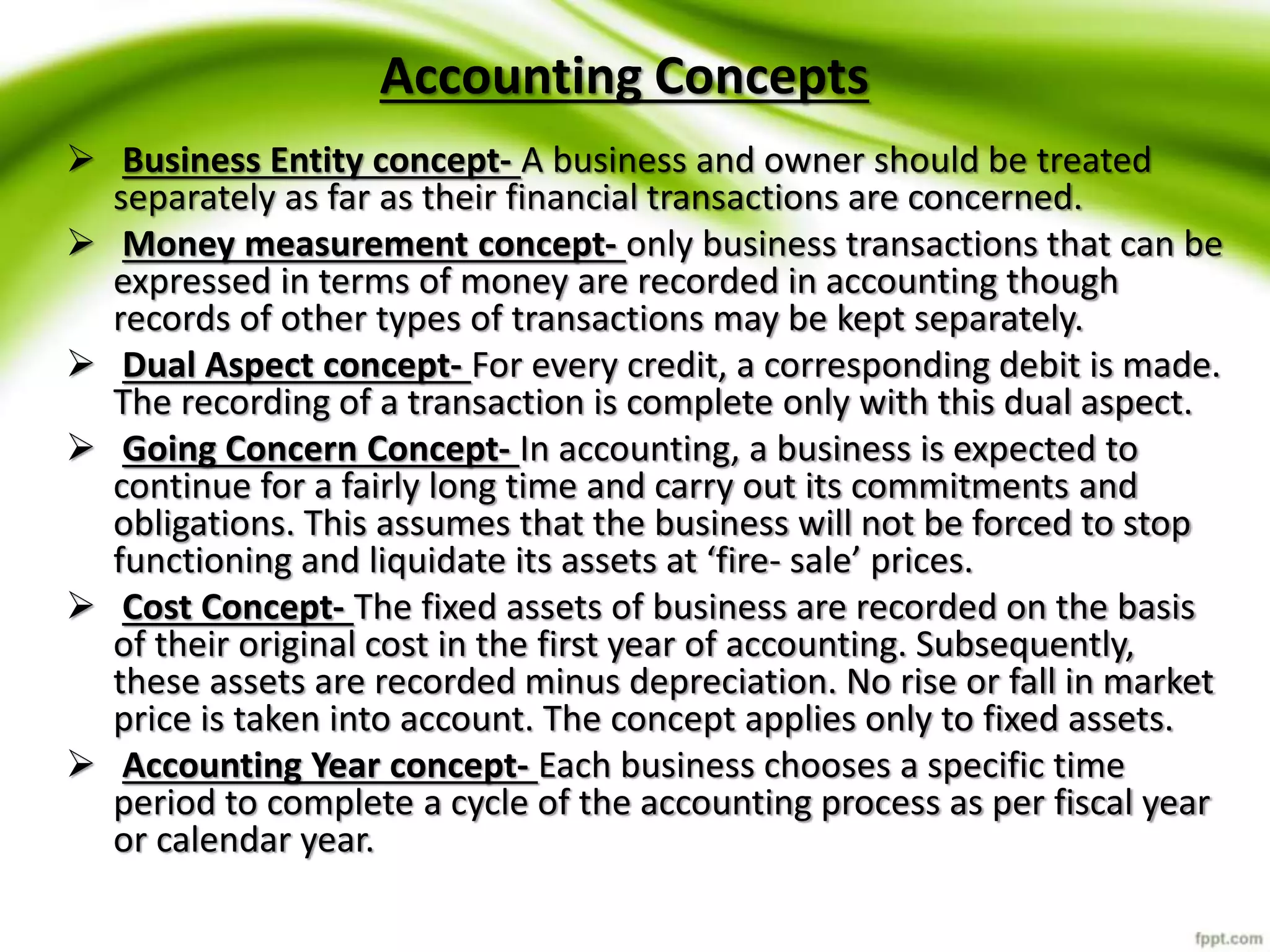

Accounting is the art of recording, classifying, and summarizing financial transactions, leading to the analysis and interpretation of financial data for decision-making. It encompasses branches like financial, cost, and management accounting and offers benefits such as insights into financial performance and aid in management decisions. However, accounting has limitations, such as ignoring qualitative factors and price level changes, and involves key concepts like the business entity concept and the accounting equation.

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)