The document provides an overview of key concepts in financial accounting including:

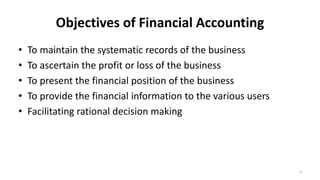

- The meaning and objectives of financial accounting

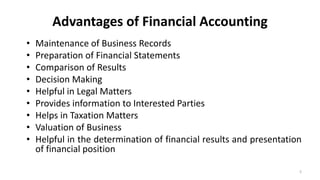

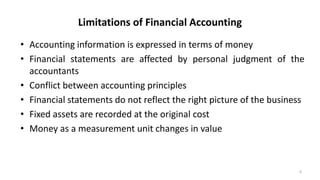

- The advantages and limitations of financial accounting

- Accounting principles like the accounting equation, concepts, and conventions

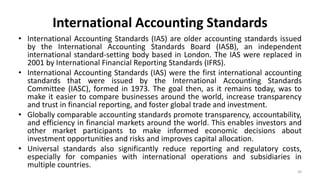

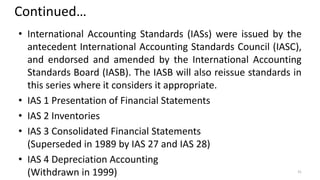

- International accounting standards set by the IASB

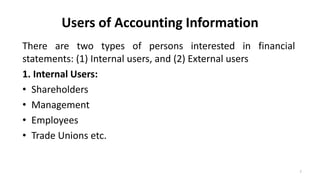

- Users of accounting information both internal and external to a business