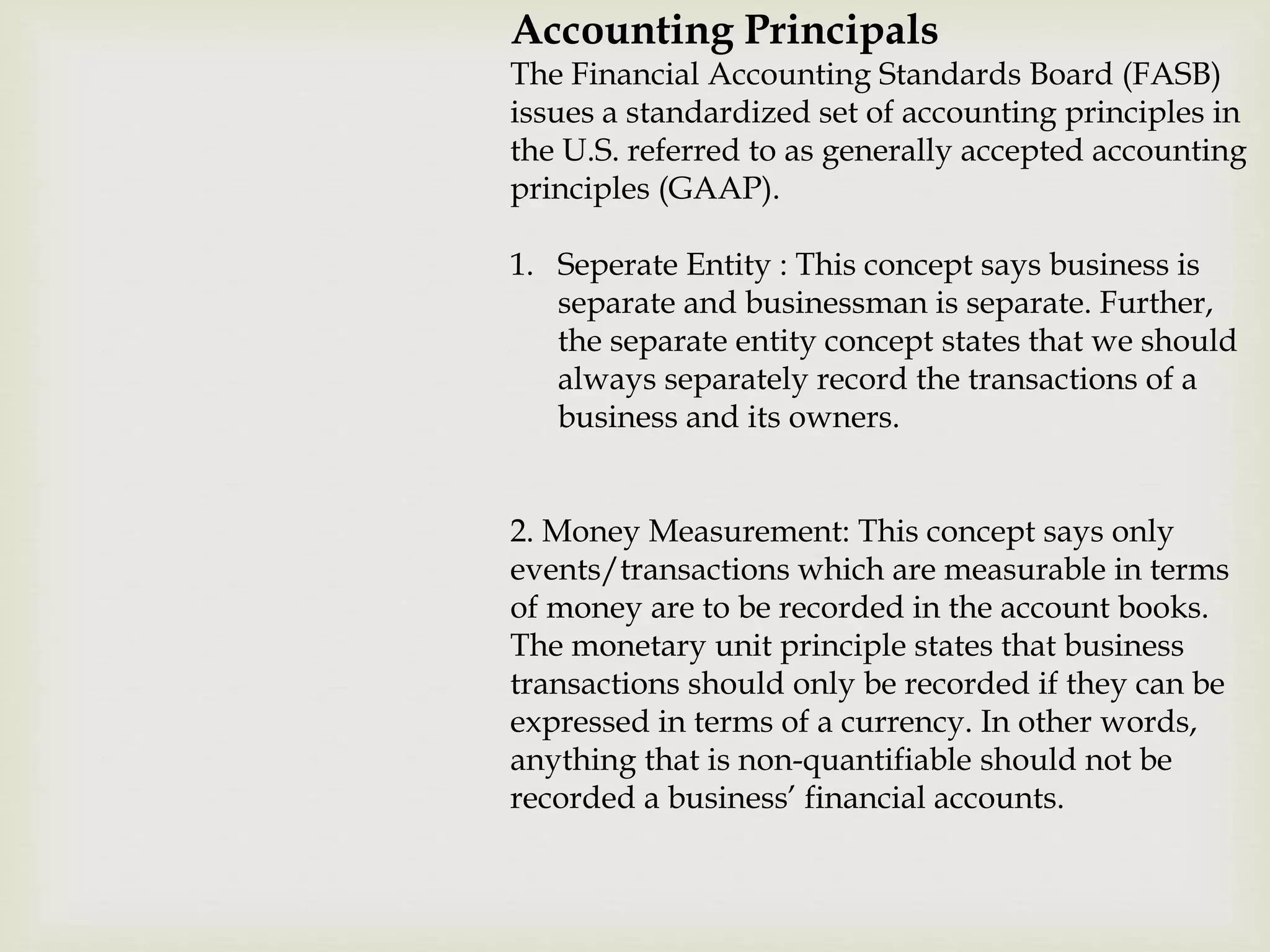

Accounting involves systematically recording all financial transactions of a business entity. The key objectives of accounting are to maintain records of transactions, ascertain profits and losses, determine the financial position of the entity, provide information to users of financial statements, and assist management. Financial statements like the income statement and balance sheet are prepared using accounting principles such as separate entity, money measurement, and accrual basis. Qualitative characteristics of accounting information include reliability, relevance, understandability, and comparability.

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)