Downloaded 98 times

![WHO SHALL CONDUCT SUCH AUDIT?

The audit may be conducted either by the

company’s auditor or another chartered

accountant who may or may not be engaged

in a practice, appointed by the Central

Government [Sections 233(1) & (2)].](https://image.slidesharecdn.com/auditing-150208040644-conversion-gate01/75/Special-Auditing-6-2048.jpg)

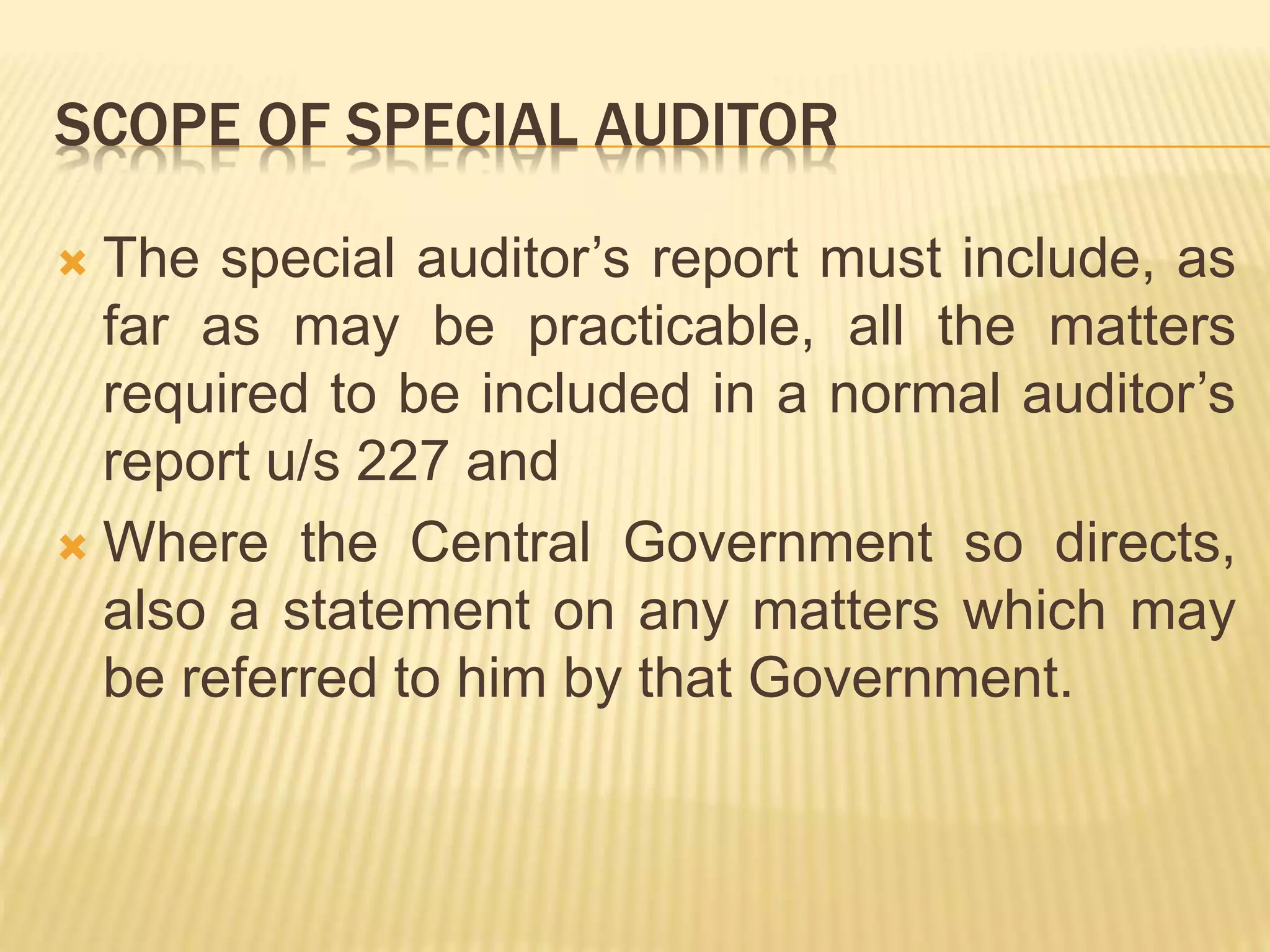

![SCOPE(CONT….)

To facilitate the special auditor’s work, the

Central Government may serve an order on

any person directing him to furnish all

information that the special auditor may

need. Non-compliance with the order attracts

a fine upto Rs.5,000 [Section 233A(5)].](https://image.slidesharecdn.com/auditing-150208040644-conversion-gate01/75/Special-Auditing-9-2048.jpg)

![REPORT

On receipt of the report, the Central

Government may take necessary action under

the Companies Act,1956 or any other law.

If no action is taken within four months from the

receipt of the report, the Central Government

must send either a complete copy of the report

or relevant extracts from it and direct the

company either to circulate the copy or extracts

among the members or to read it at the next

general meeting [Section 233A(6)].](https://image.slidesharecdn.com/auditing-150208040644-conversion-gate01/75/Special-Auditing-10-2048.jpg)

![REMUNERATION & ITS RECOVERY

The expenses of or incidental to a special

audit, including the remuneration of the

special auditor as fixed by the Central

Government (and its decision in this regard is

final), must be paid by the company.

If the company defaults in making the

payment, the amount can be recovered from

the company as arrears of land revenue

[Section 233A(6)].](https://image.slidesharecdn.com/auditing-150208040644-conversion-gate01/75/Special-Auditing-11-2048.jpg)

A special audit is conducted by the government in certain circumstances to examine a company's financial information. It can be performed by the company's auditor or another chartered accountant appointed by the government. The special auditor has the same powers as a statutory auditor and must report findings to the government. The scope includes examining matters in a normal audit report and any other issues referred by the government. The company must pay expenses of the special audit.