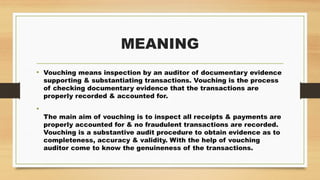

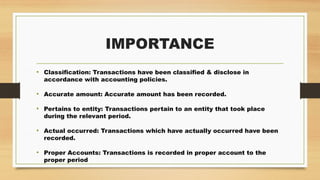

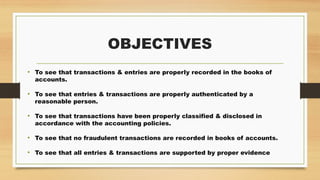

Vouching is an auditing process that involves inspecting documentary evidence to validate and substantiate financial transactions, ensuring they are accurately recorded and free from fraud. Its importance lies in confirming that transactions are classified, accurately recorded, pertain to the entity, and are supported by proper documentation. Vouchers serve as documentary evidence for transactions and can be classified into primary and secondary types.