Downloaded 22 times

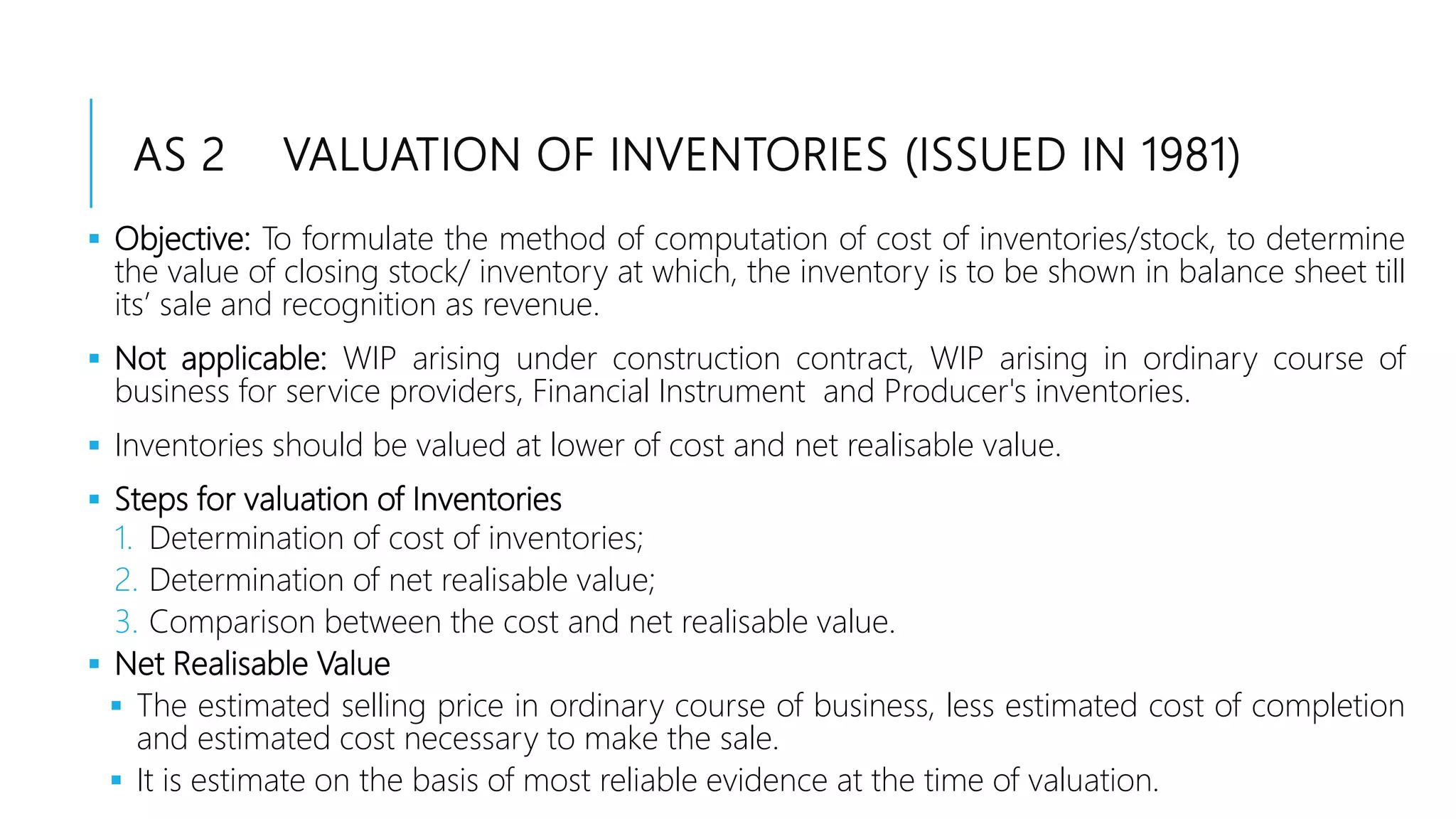

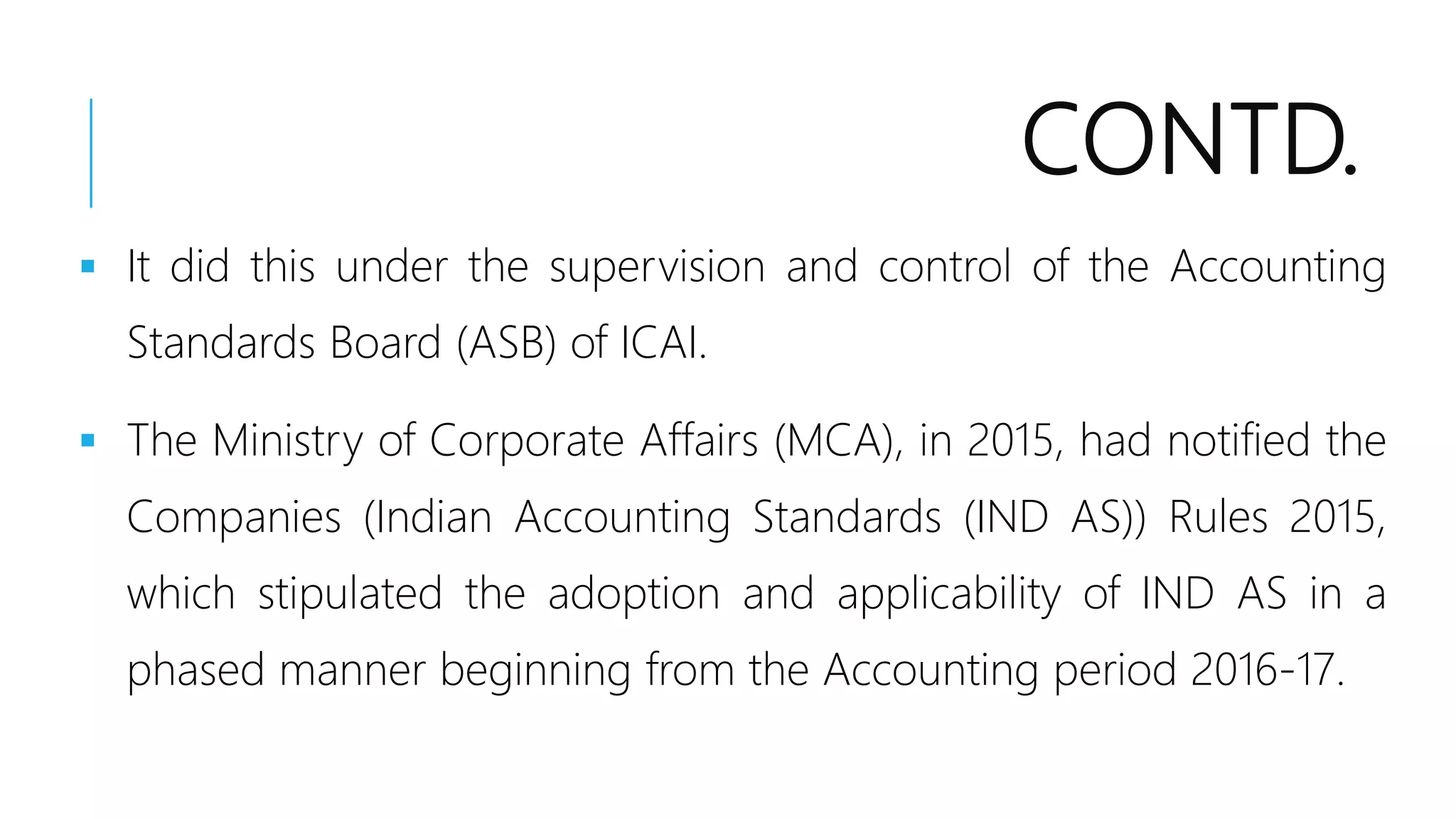

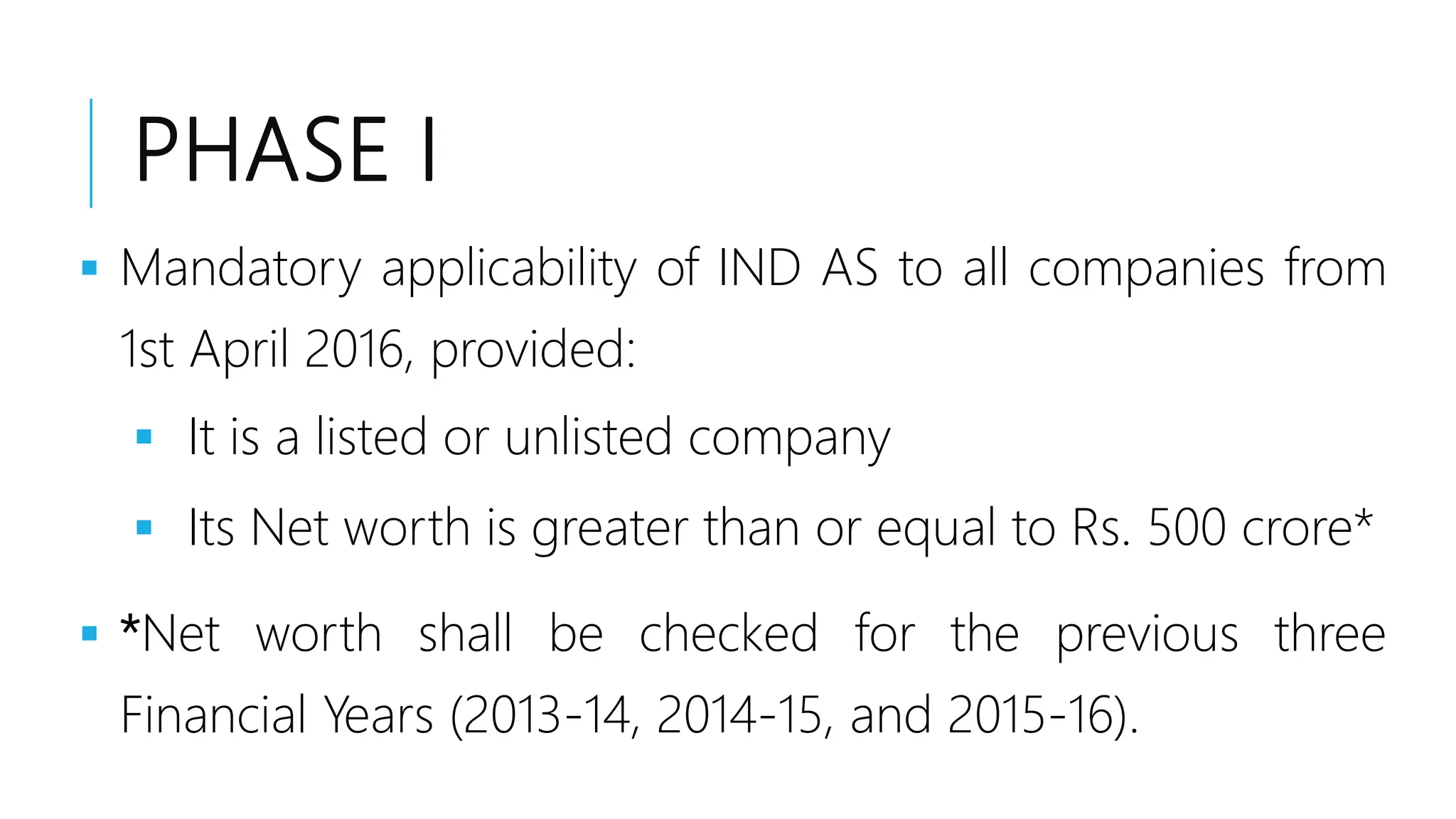

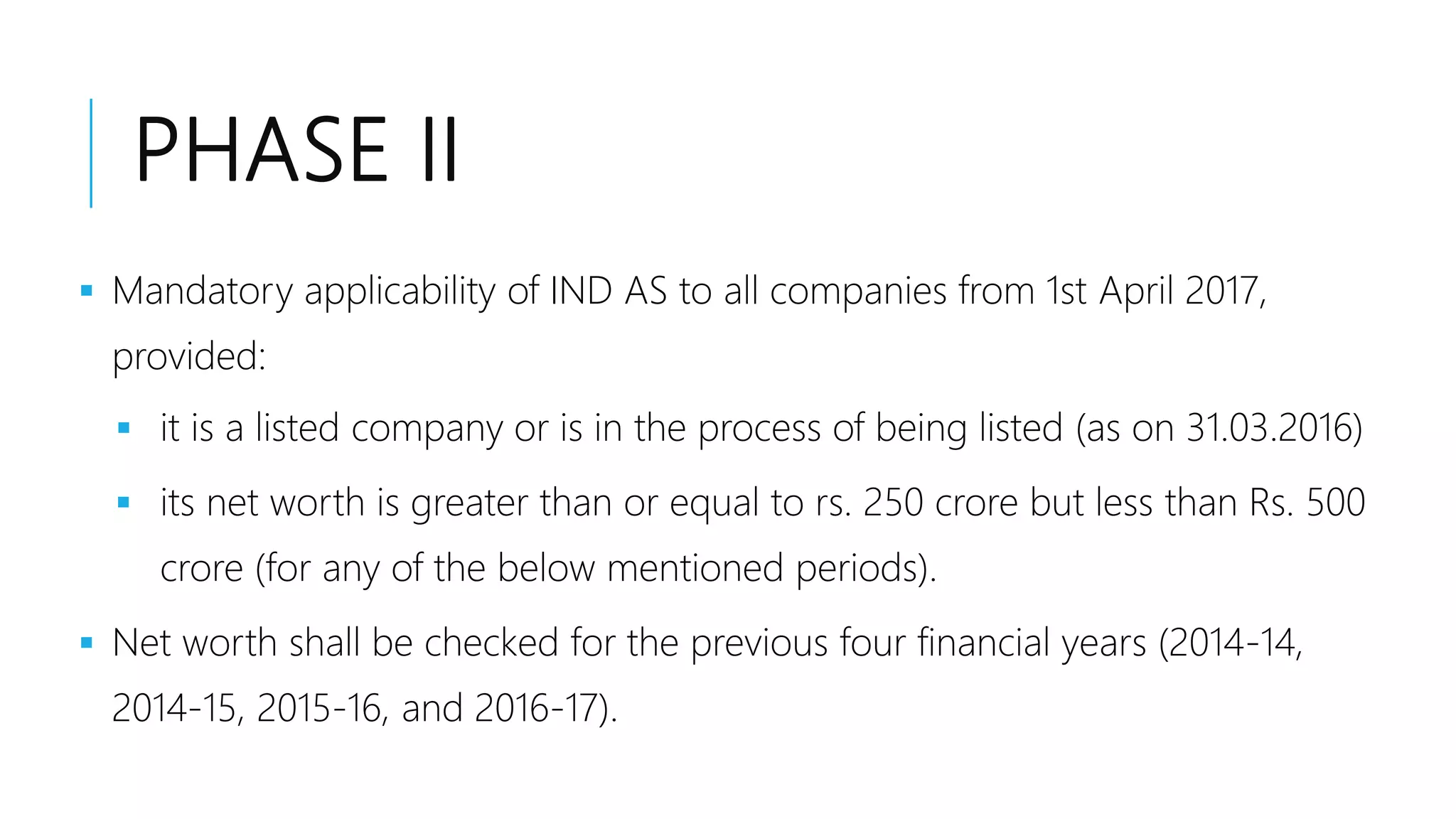

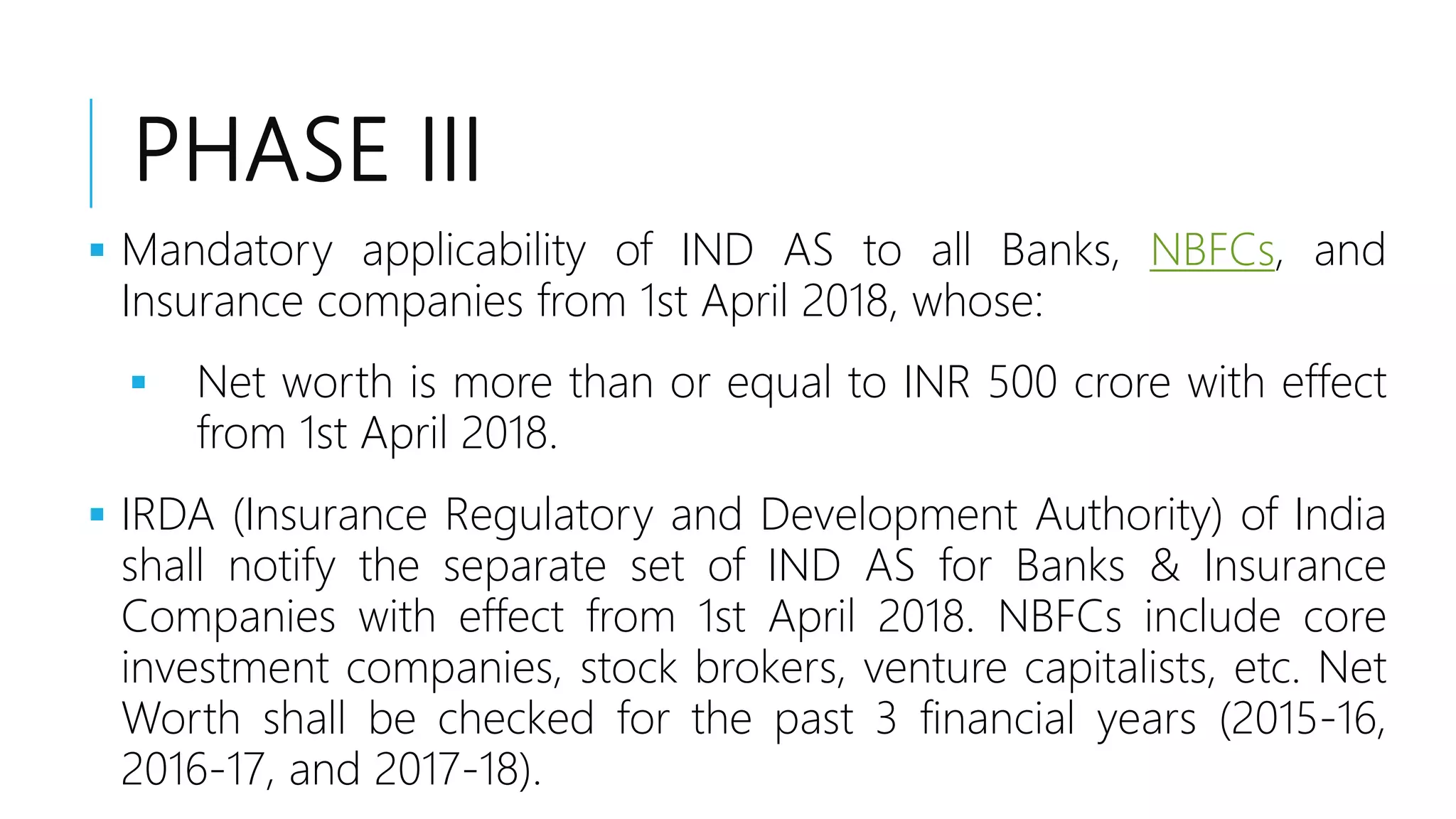

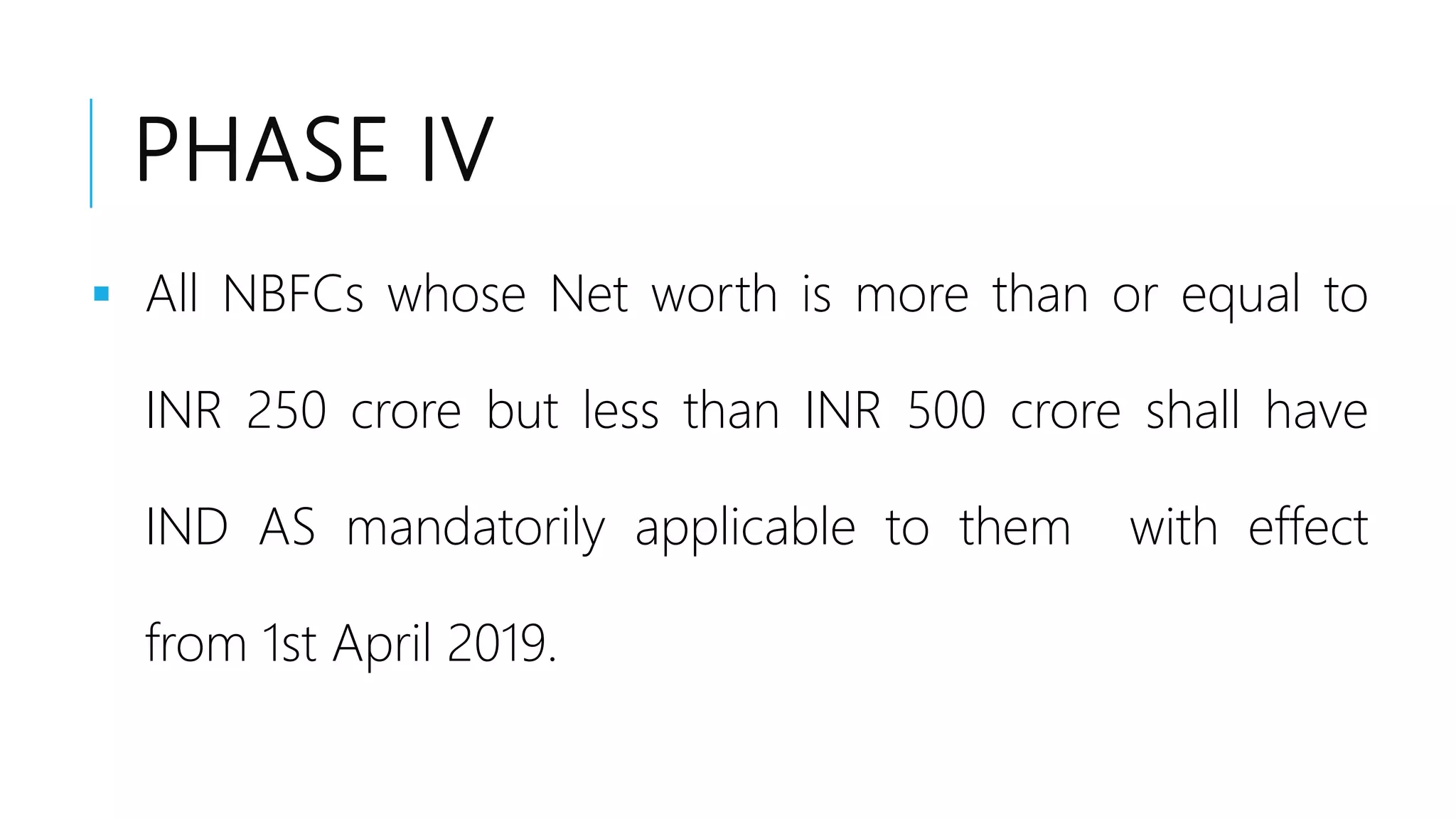

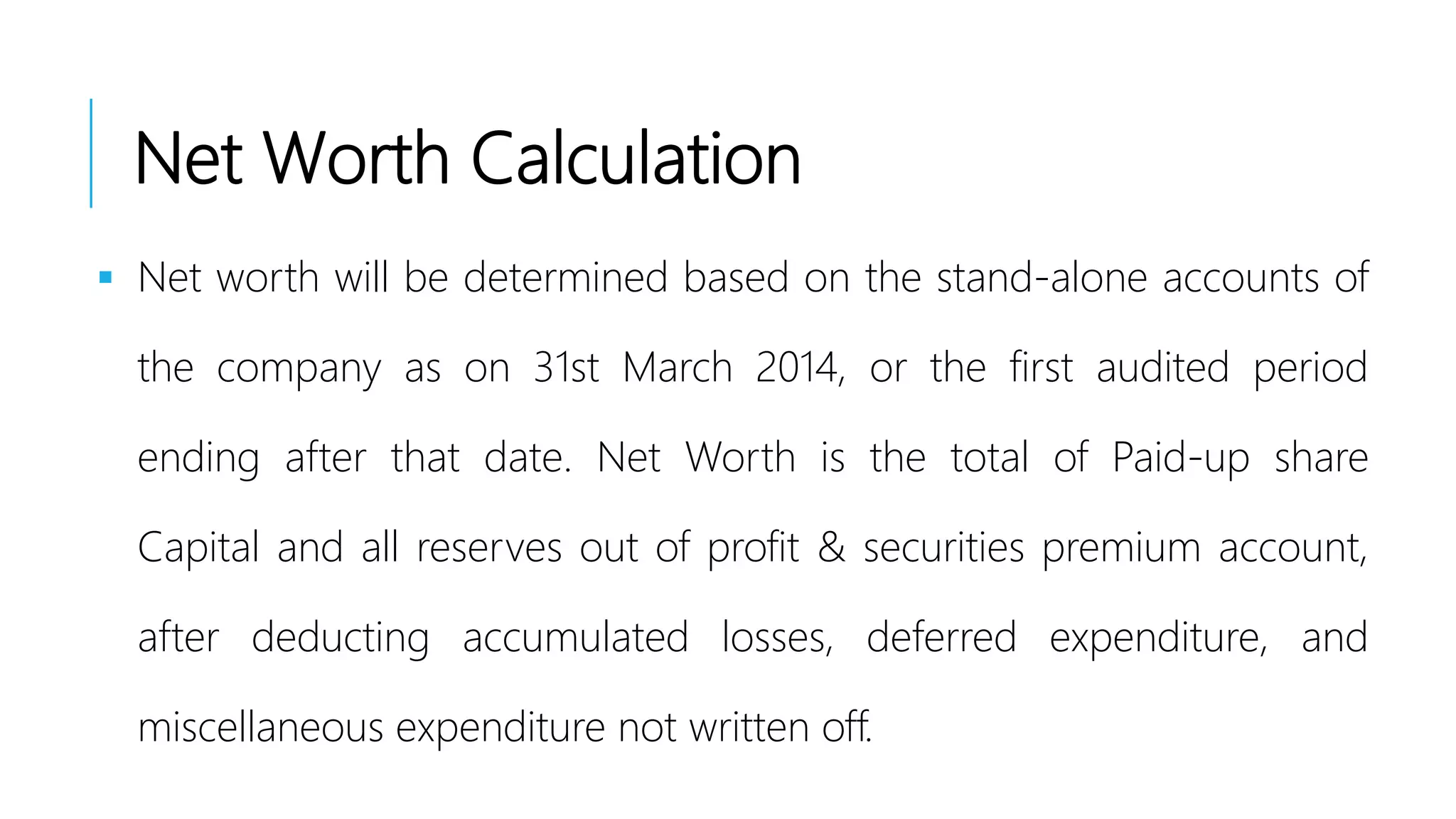

This document provides an overview of accounting standards in India. It discusses the need for and objectives of accounting standards, which are to bring uniformity in accounting methods, improve reliability of financial statements, and simplify accounting information. It summarizes some key Indian Accounting Standards (Ind AS), including Ind AS 1 on disclosure of accounting policies, Ind AS 2 on valuation of inventories, and Ind AS 101 on first-time adoption of accounting standards. Ind AS 2 specifies that inventories should be measured at the lower of cost and net realizable value. The document also outlines the phases for adoption of Ind AS for companies in India based on their net worth.