The document discusses the concept and process of test checking in auditing. It defines test checking as selecting and examining a representative sample from a large number of similar transactions rather than examining every transaction. Some key points discussed include:

- Test checking is suitable when there are large volumes of routine transactions or when the auditor needs to complete work quickly.

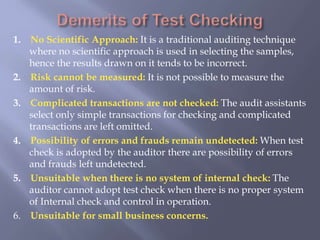

- It allows the auditor to focus on more important areas while still obtaining a reasonable assurance about the accounts. However, it does not allow risks to be measured scientifically and errors or frauds could remain undetected.

- The auditor must select samples carefully and ensure different types of entries, accounts, and personnel work is included in the test checks.