Download to read offline

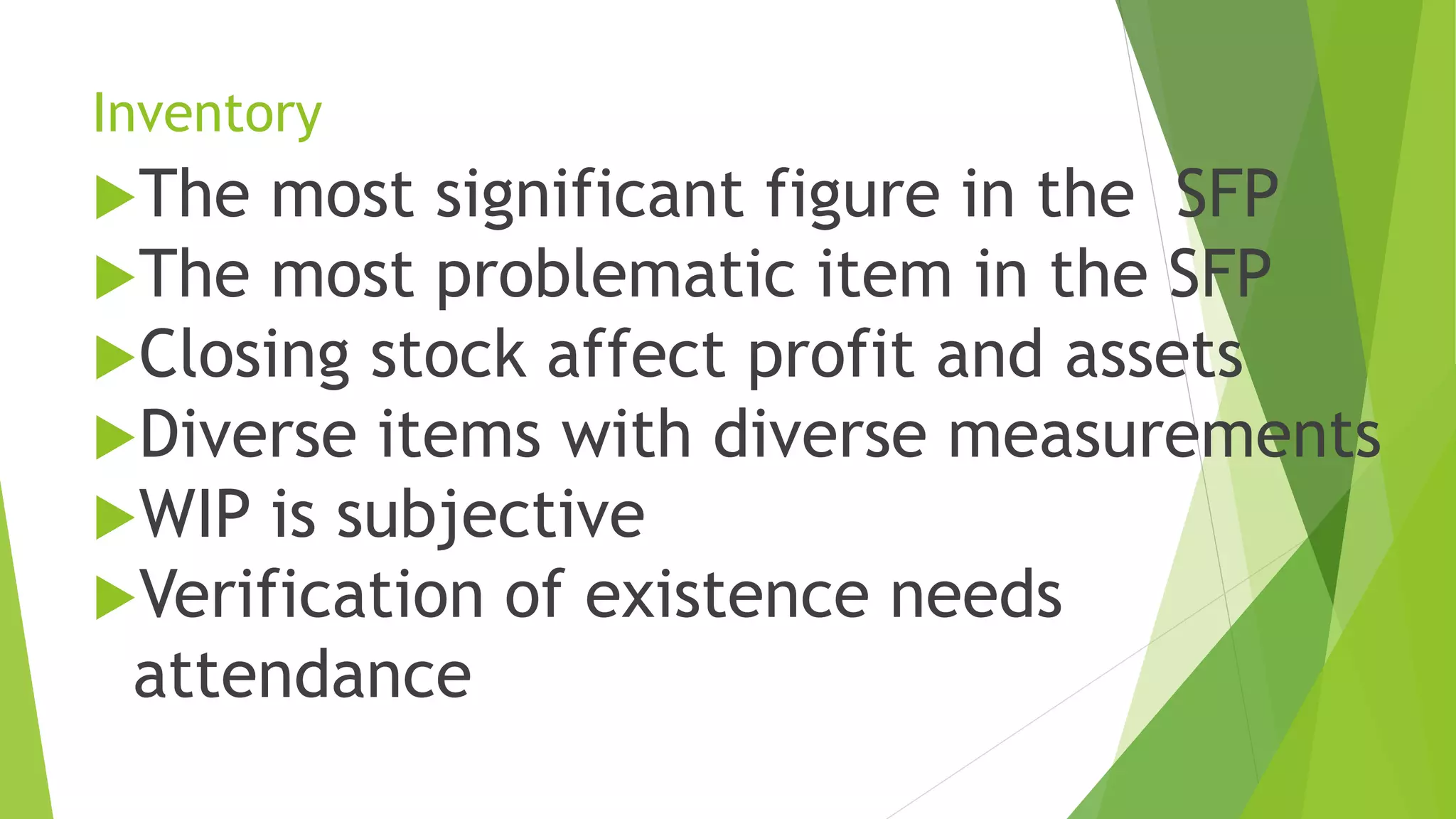

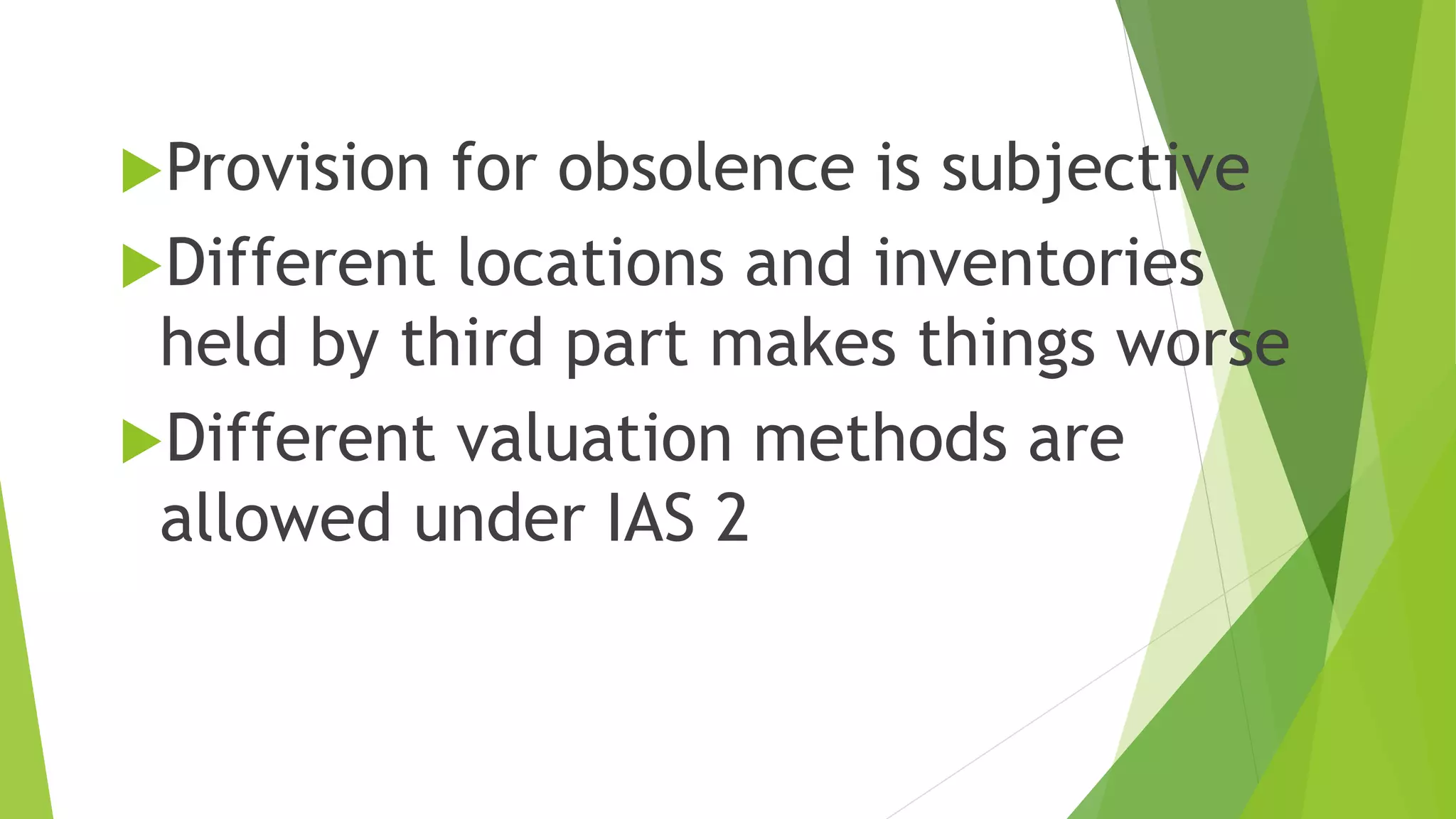

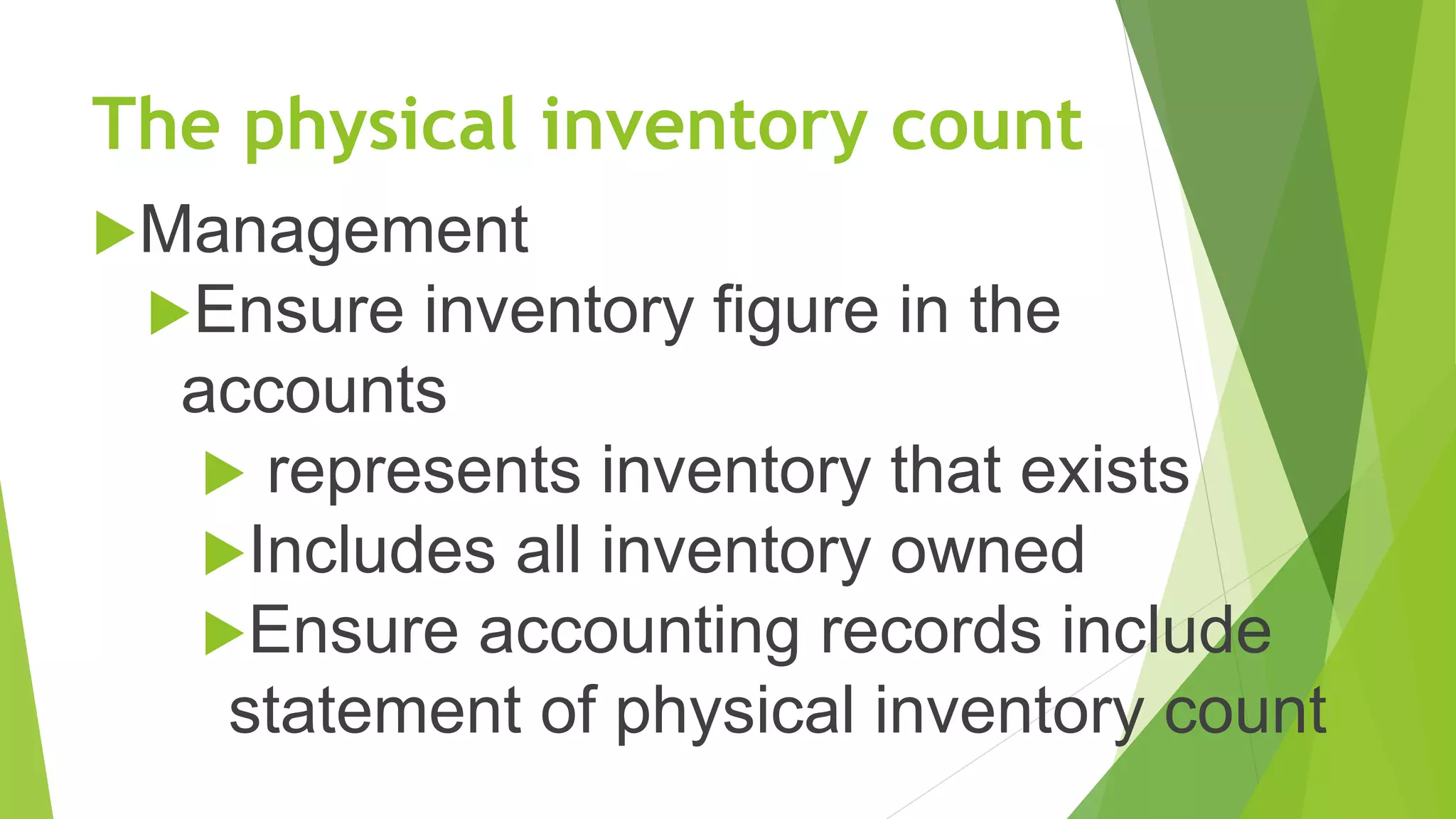

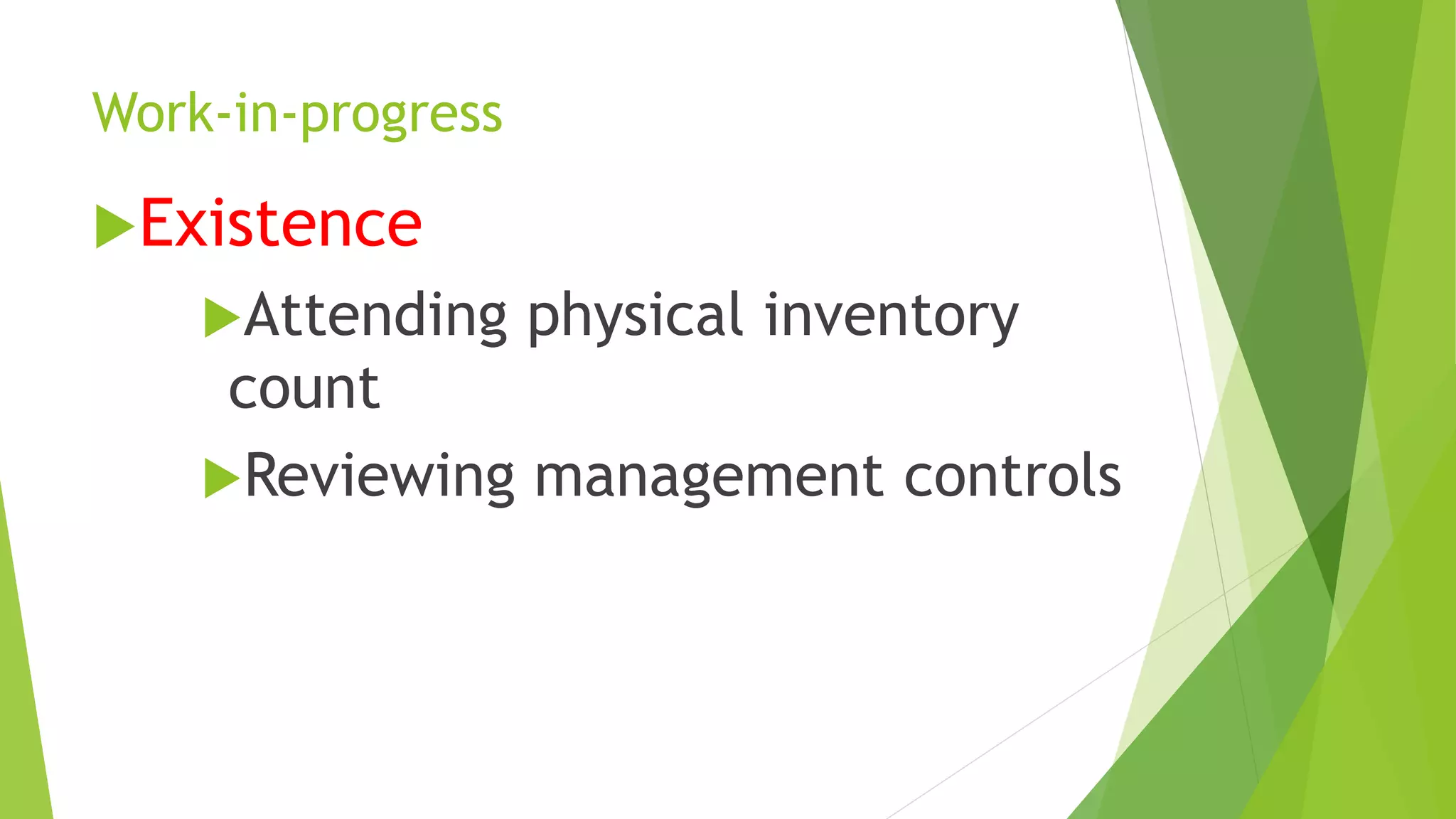

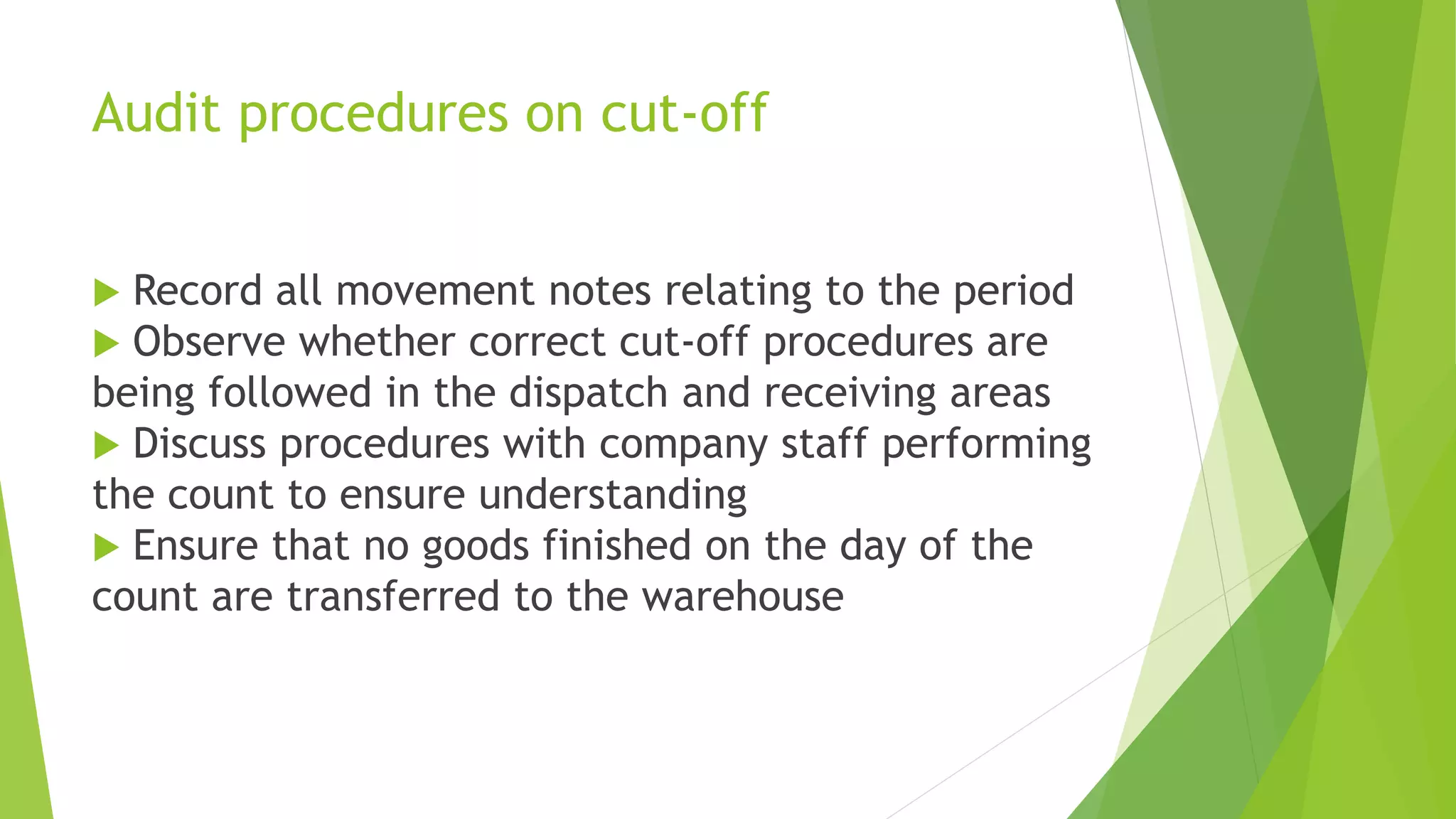

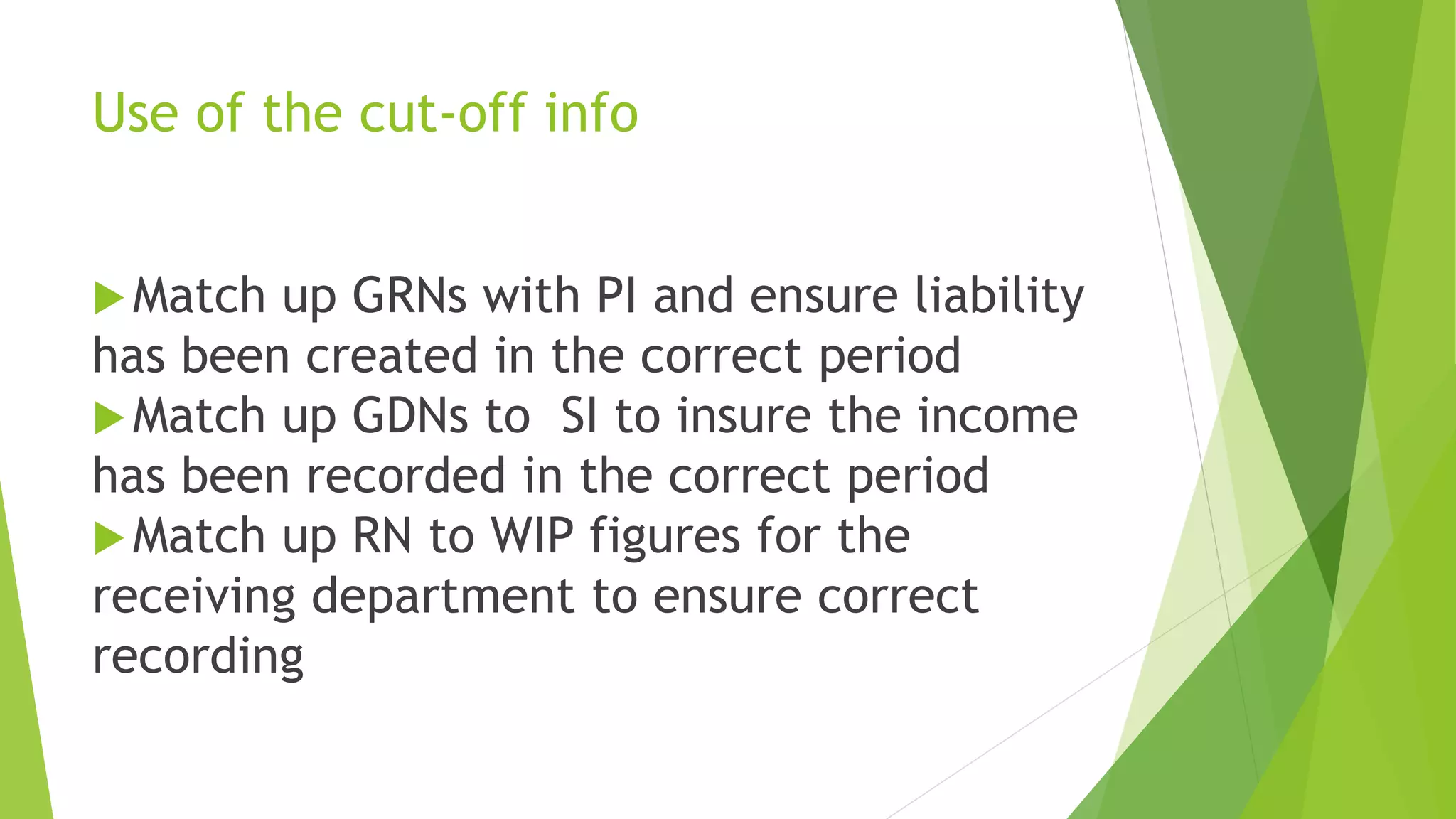

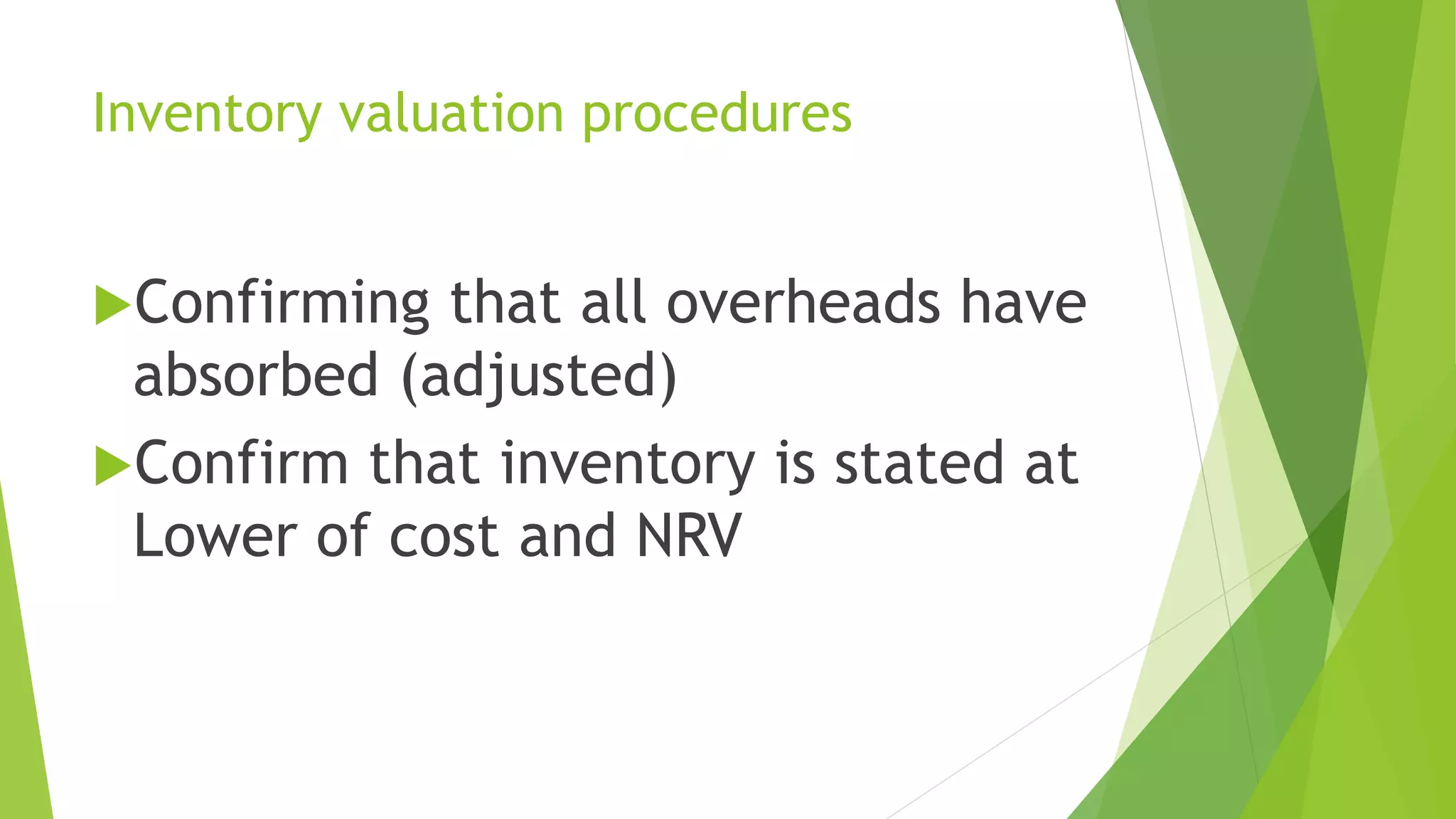

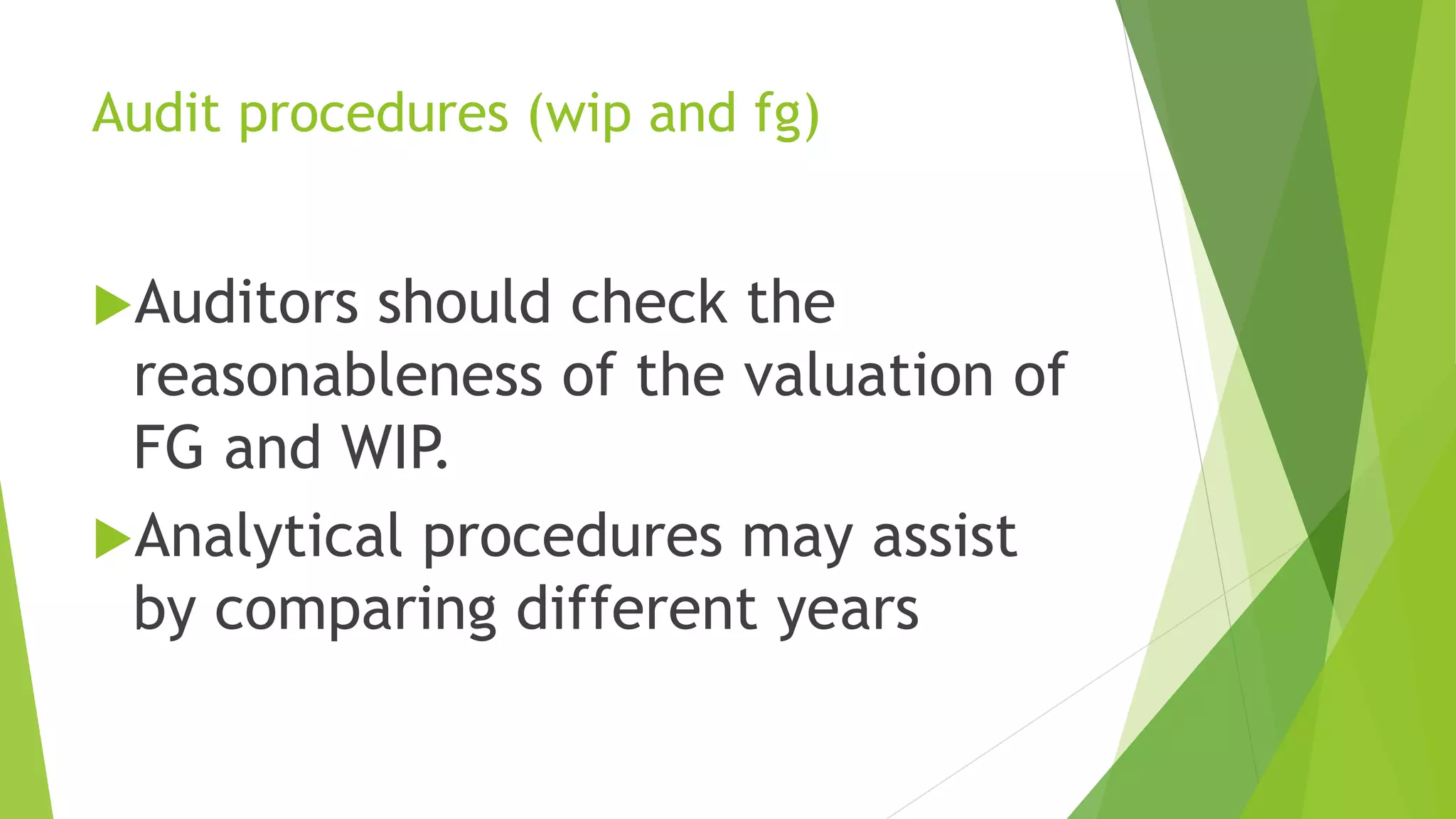

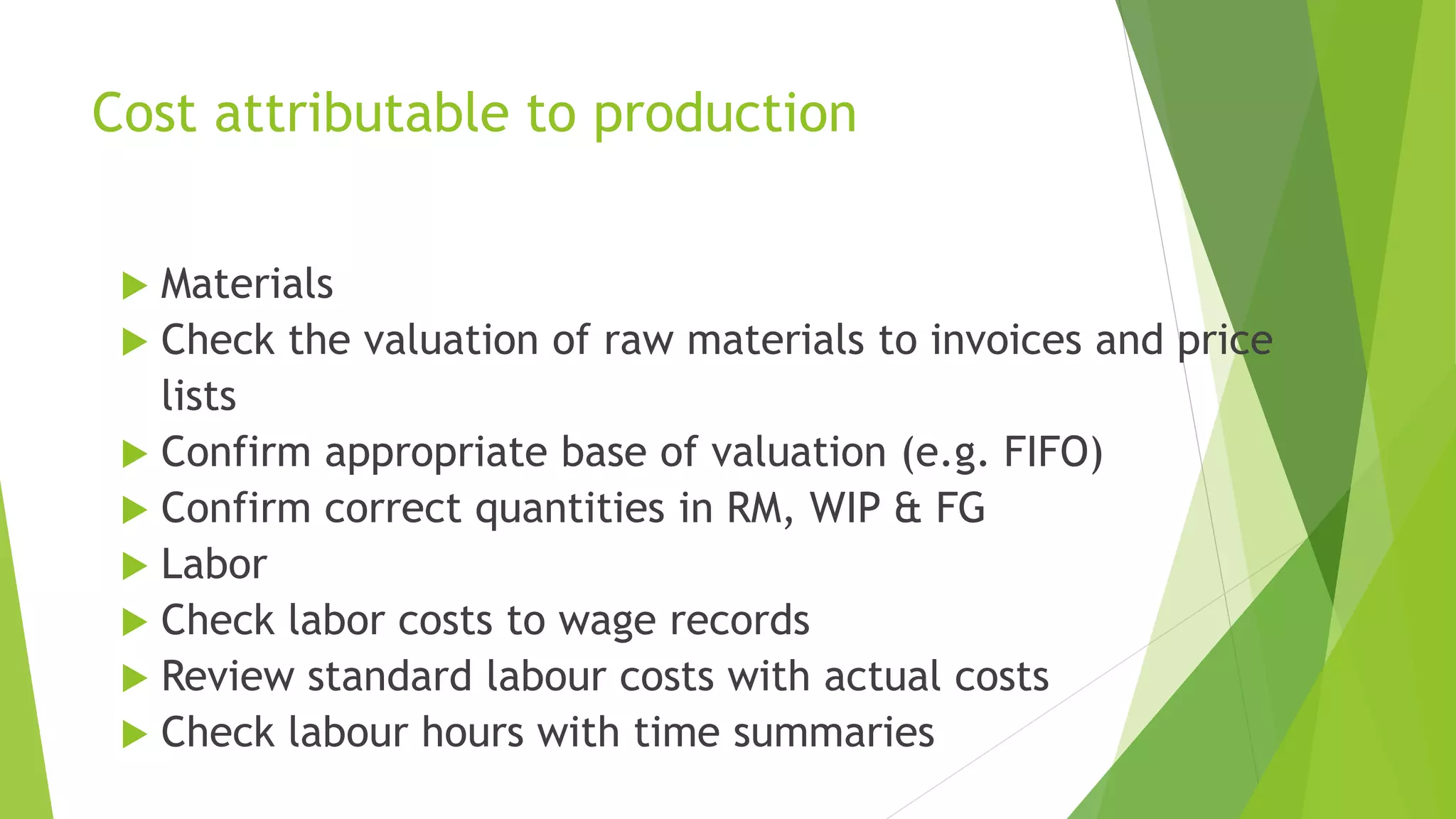

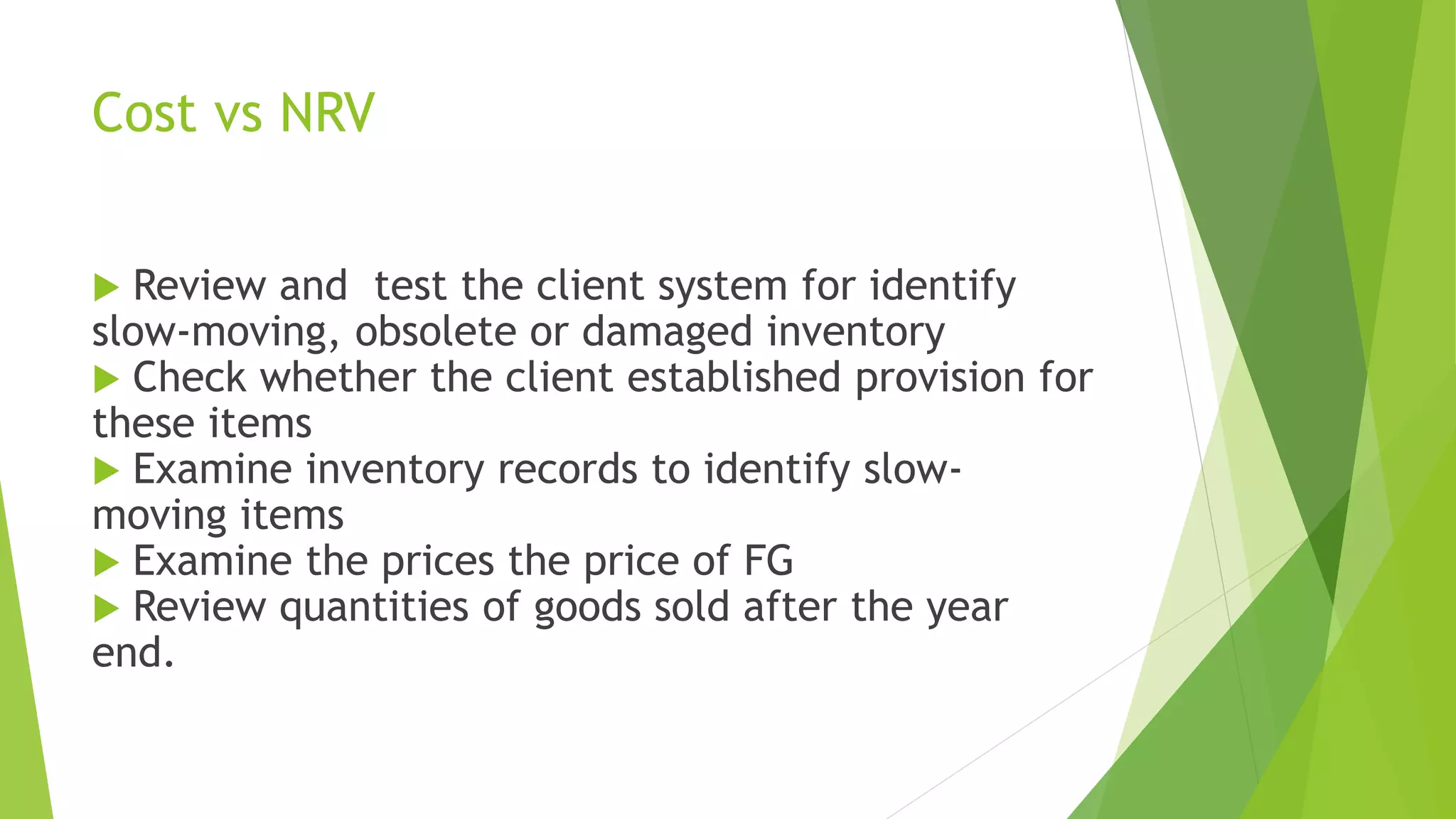

This document discusses inventory auditing. It covers the key elements of inventory auditing including existence, completeness, valuation, and ownership. It describes regulatory requirements under IAS 2 and ISA 501. The document outlines procedures for planning, attending, and following up on the physical inventory count. It also discusses important audit procedures for inventory cut-off, valuation of raw materials, work-in-progress, and finished goods, as well as comparing inventory costs to net realizable value.

![AOMEI Partition Assistant 11.1 Crack with License Key [Latest]](https://cdn.slidesharecdn.com/ss_thumbnails/auditiich-4-250407152903-ab1d141c-250407155555-93d416fc-thumbnail.jpg?width=640&height=640&fit=bounds)

![Rekordbox DJ Crack with License Key Download [Latest]](https://cdn.slidesharecdn.com/ss_thumbnails/auditiich-4-250407152903-ab1d141c-250407154506-cfbcf160-thumbnail.jpg?width=640&height=640&fit=bounds)