Downloaded 440 times

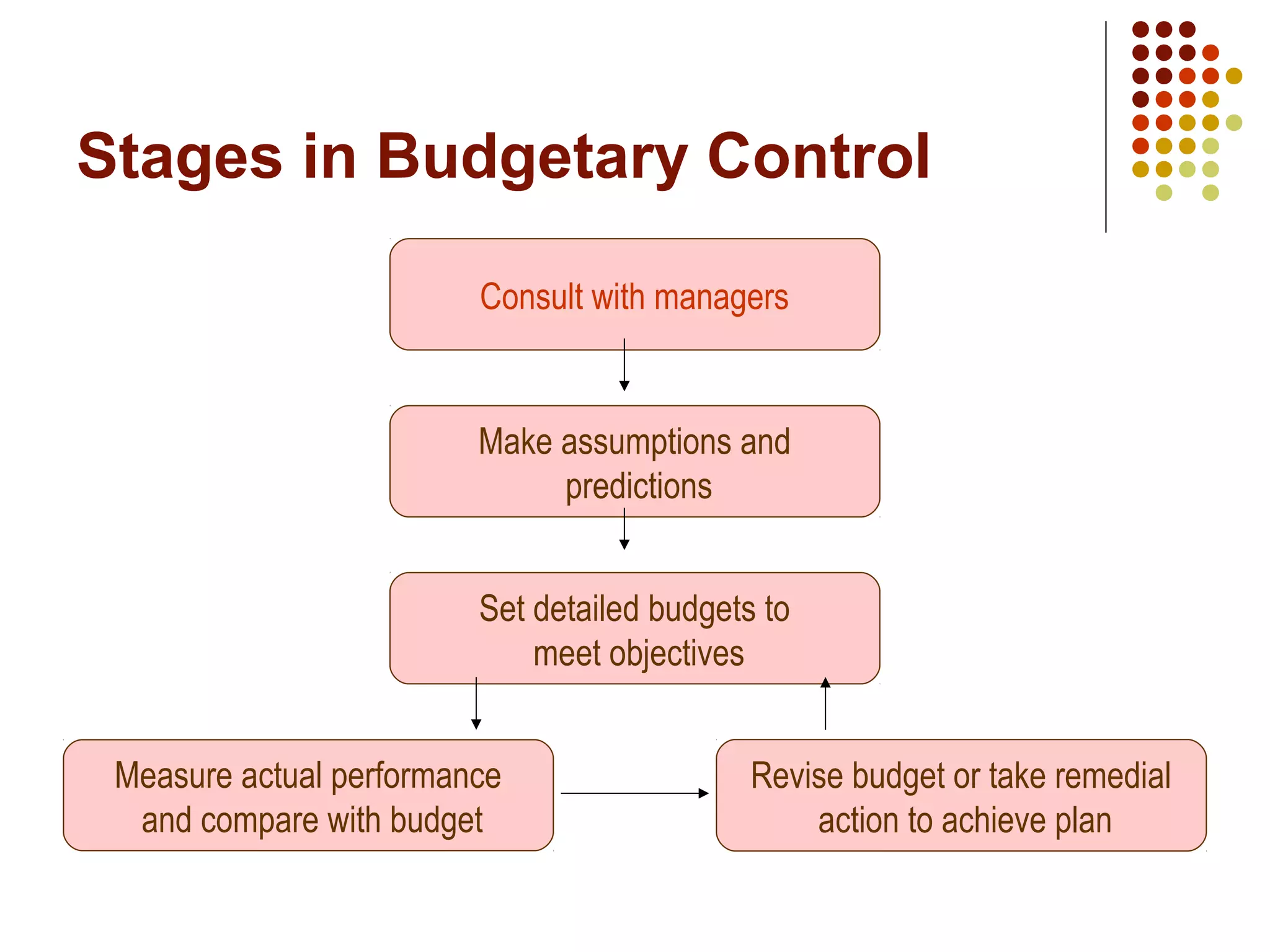

Budgetary control involves companies establishing budgets for revenue, expenses, assets and liabilities in advance of an accounting period. Managers prepare functional budgets for their departments, which are then combined into a master budget. Actual performance is continuously compared to budgets to ensure plans are achieved or provide a basis for revision. Budgetary control coordinates activities, provides responsibility accounting, motivates managers, and establishes a system for planning and control through regular budget reviews.