Downloaded 905 times

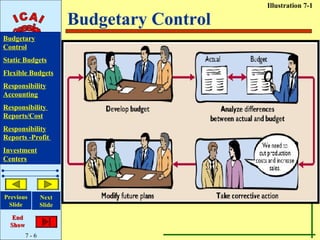

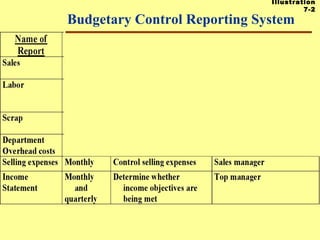

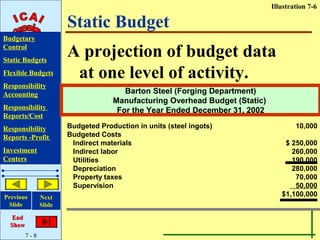

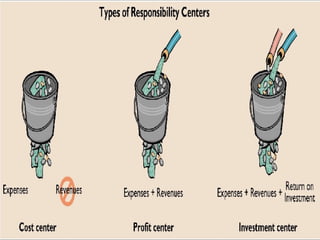

The document discusses key concepts related to budgetary control including: - Static and flexible budgets which are used to control operations by comparing actual results to planned objectives. - Responsibility accounting which involves accumulating and reporting revenues and costs based on the manager who has authority over decisions. - Types of responsibility centers like cost centers, profit centers, and investment centers. - Performance evaluation principles for responsibility centers and the use of budgets, reports, and metrics like residual income and return on investment to evaluate managers.