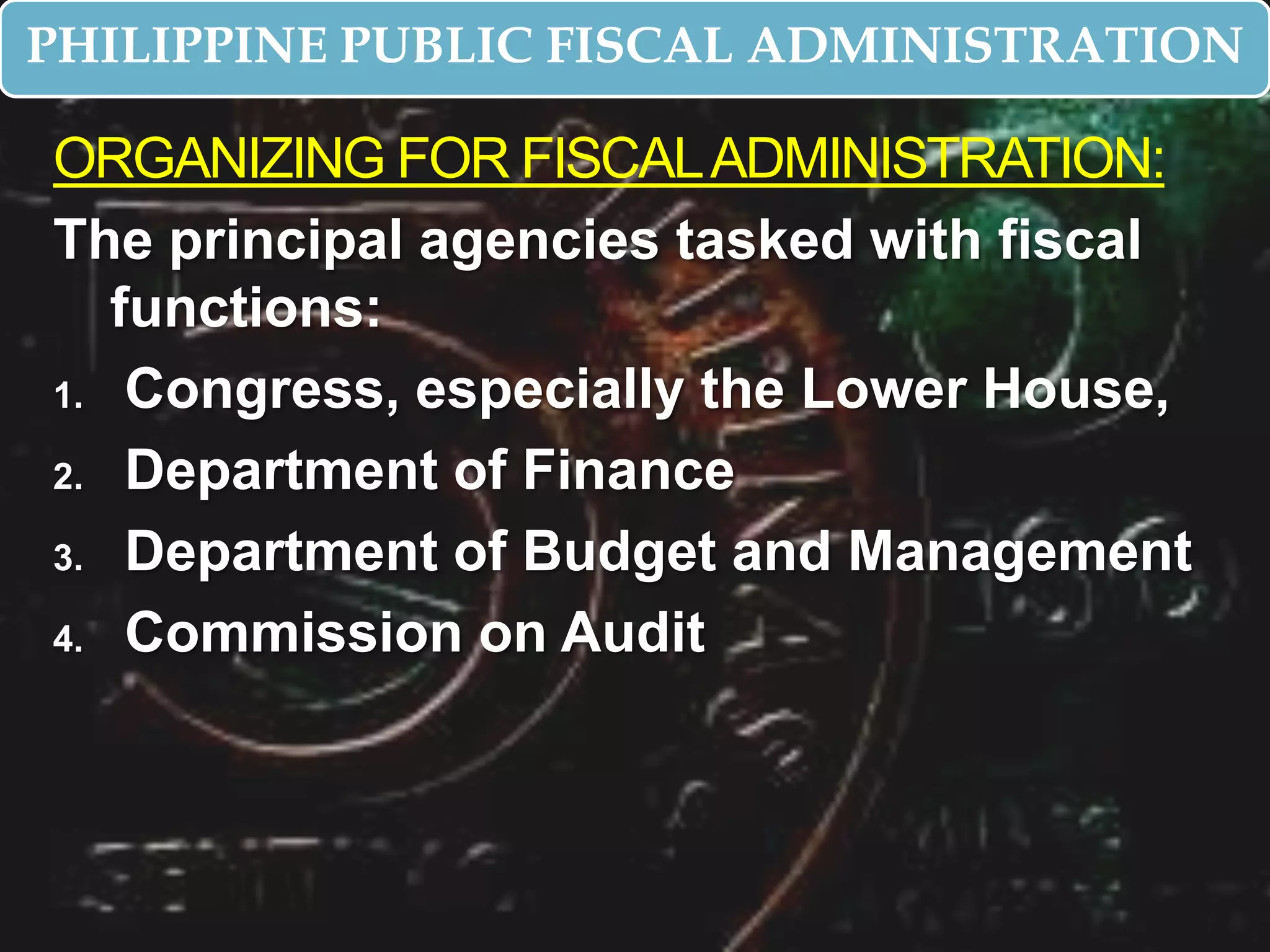

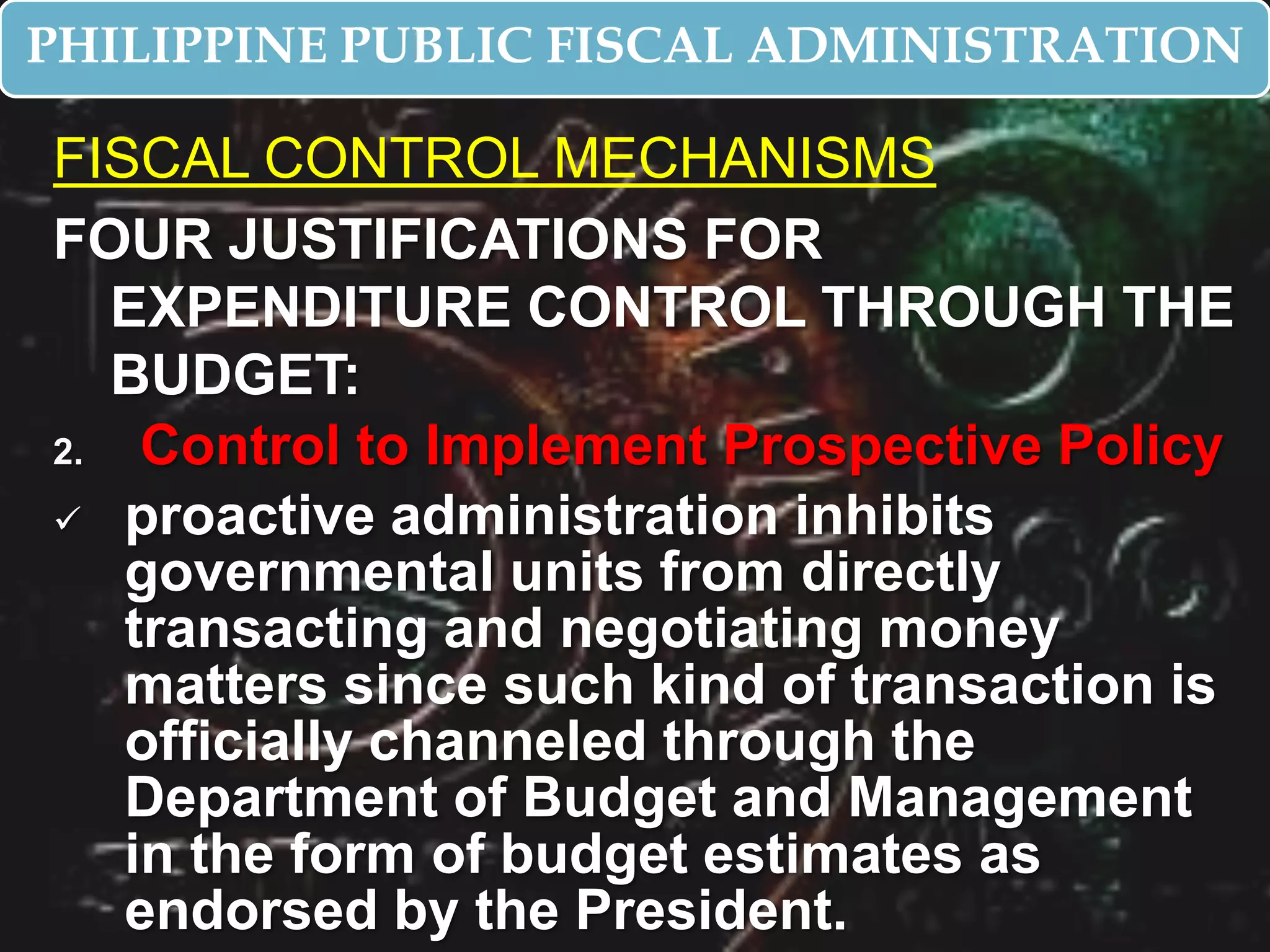

Fiscal administration involves the management of financial resources including revenue generation, fund availability, and ensuring funds are spent wisely, lawfully, and efficiently. It is an important administrative responsibility. The key Philippine government agencies involved in fiscal functions are Congress, the Department of Finance, Department of Budget and Management, and Commission on Audit. The budget process involves preparation, authorization, implementation, and accountability stages at both the national and local levels.