Downloaded 114 times

![Monopoly

Derived from Greek Words: monos polein (alone to sell)

A market structure in which there is one seller who

either sets the price or the quantity but not both.

Exp: Enterprises supplying Public Utility Services – Water Supply &

Electricity (closely resemble)

[Gas Pipeline (Mahanagar Gas- Gas connection provided in building –Mumbai),

Public Transport: BEST BUS (Mumbai) Railways]](https://image.slidesharecdn.com/monopoly-160418160923/85/Monopoly-Lecture-Notes-Economics-3-320.jpg)

![Emergence of Monopoly

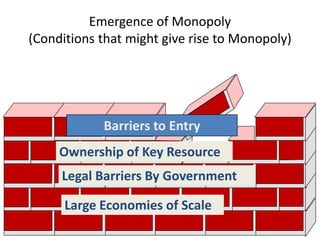

Barriers to Entry prevails in the

Market. Why?

(Implication: Imposition of Barrier to Entry ---

No competition-----Ensure growth of Profit)

– Monopolist can exercise monopoly power to

influence the market price (of its product)

[(Unlike in Perfect Competition, Monopoly is a price Setter not Price Taker

(set own price and supply entire quantity demanded)]](https://image.slidesharecdn.com/monopoly-160418160923/85/Monopoly-Lecture-Notes-Economics-12-320.jpg)

This document provides a comprehensive overview of monopoly market structures, covering definitions, examples, and the implications of monopolistic behavior on pricing and production decisions. It discusses the emergence of monopolies due to barriers to entry, economies of scale, and government interventions, alongside methods to measure monopoly power such as the Herfindahl and Lerner indices. Additionally, the document examines the effects of taxation on monopolies and compares them with perfect competition, emphasizing the impact on prices and output.

![Market structure[1]](https://cdn.slidesharecdn.com/ss_thumbnails/marketstructure1-220223133421-thumbnail.jpg?width=640&height=640&fit=bounds)