Download as PPSX, PPTX

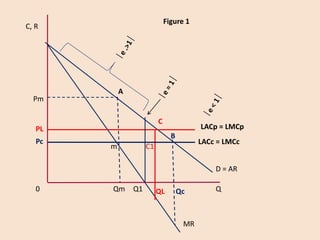

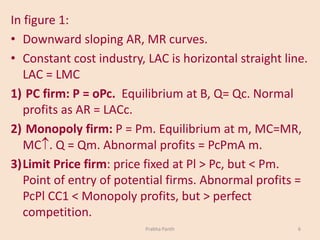

The document discusses Bain's limit pricing model. It states that under Bain's model, oligopoly firms do not maximize profits in the short run due to fear of attracting potential new entrants. Instead, firms fix a price on the inelastic portion of the demand curve called the limit price, which is the highest price that deters new firm entry. The limit price allows existing firms to earn abnormal profits above competitive levels but below monopoly profits, maintaining market stability. Diagrams are included showing the limit price between the perfect competition and monopoly price points.