Downloaded 1,270 times

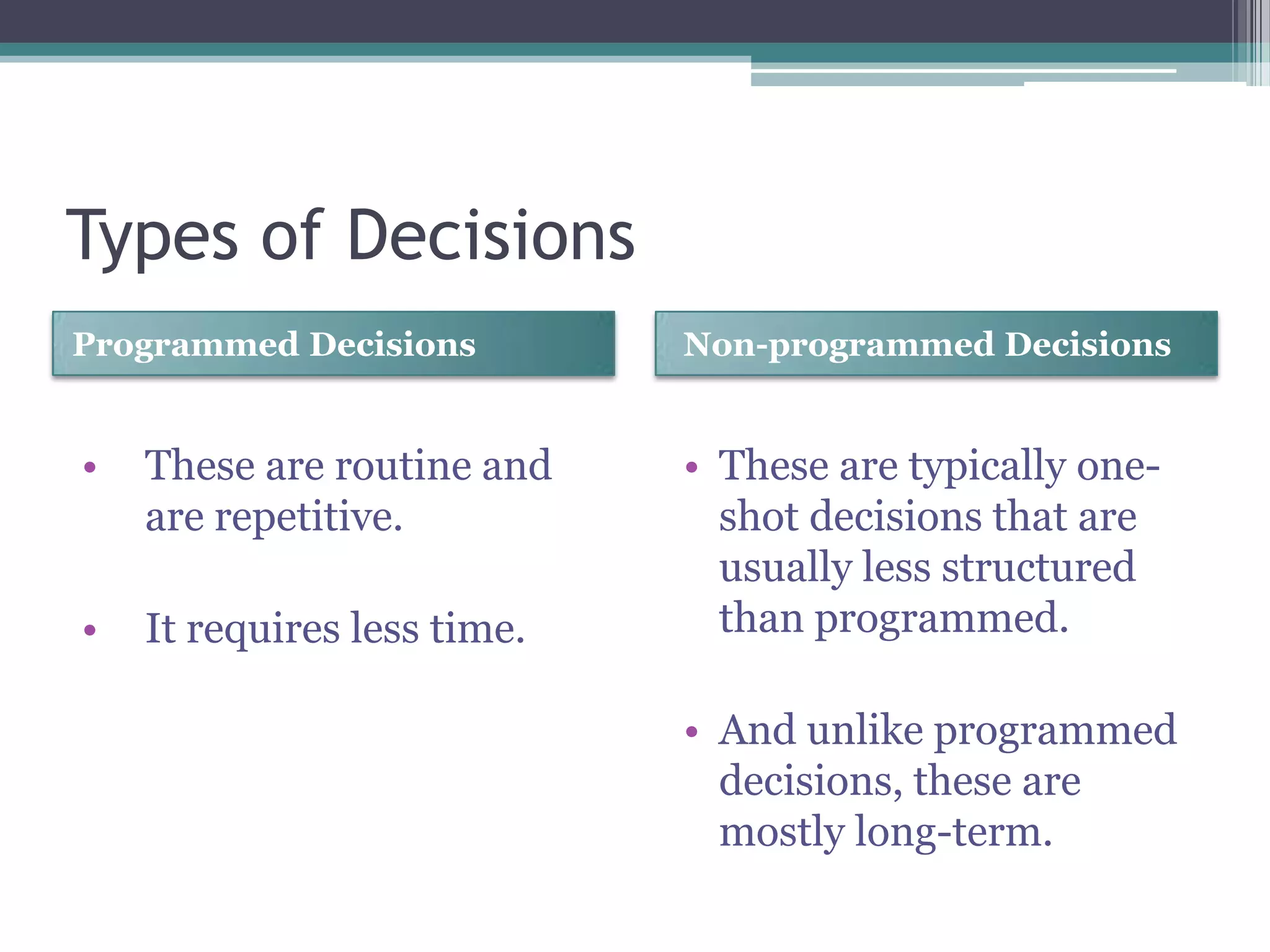

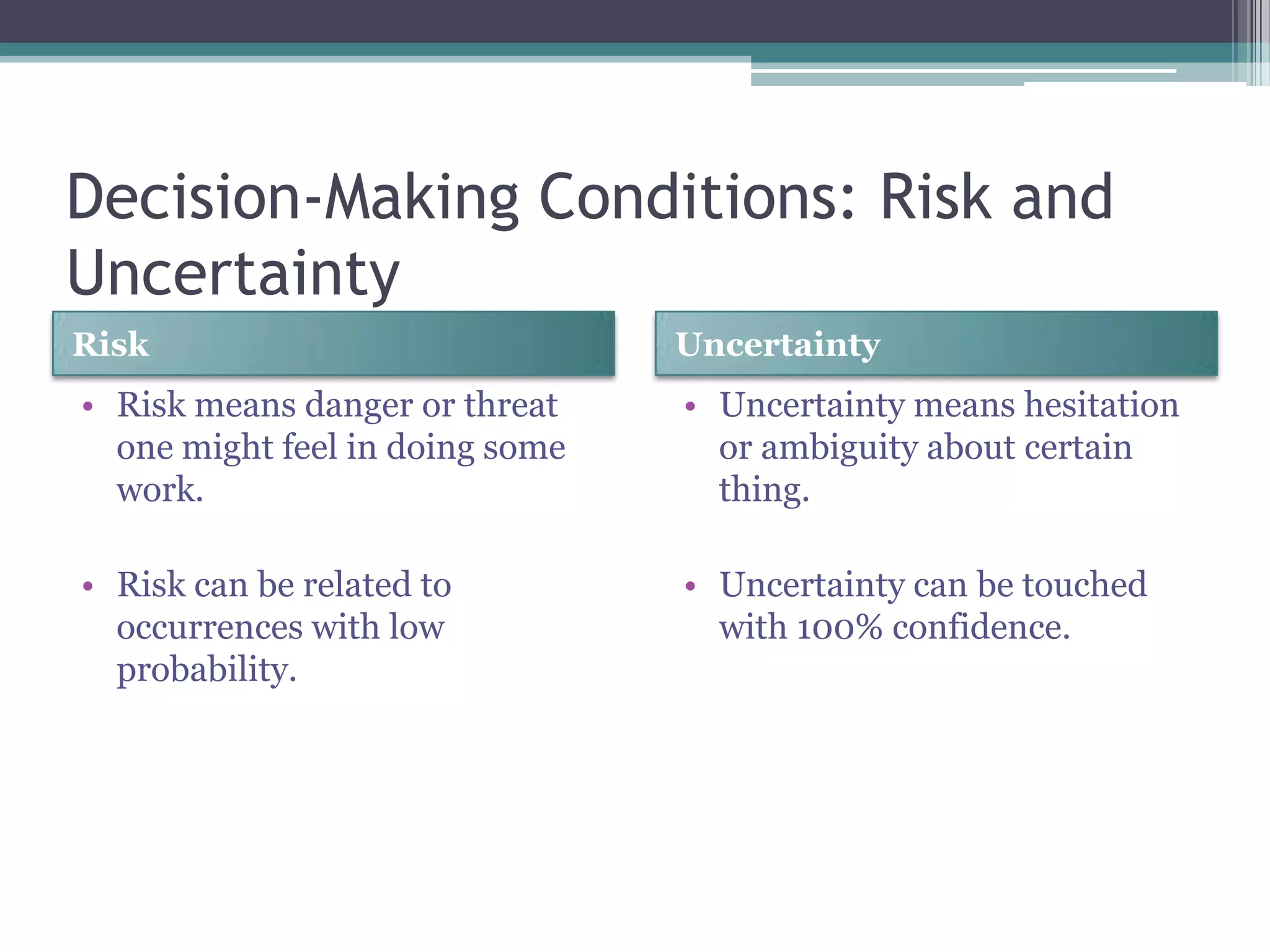

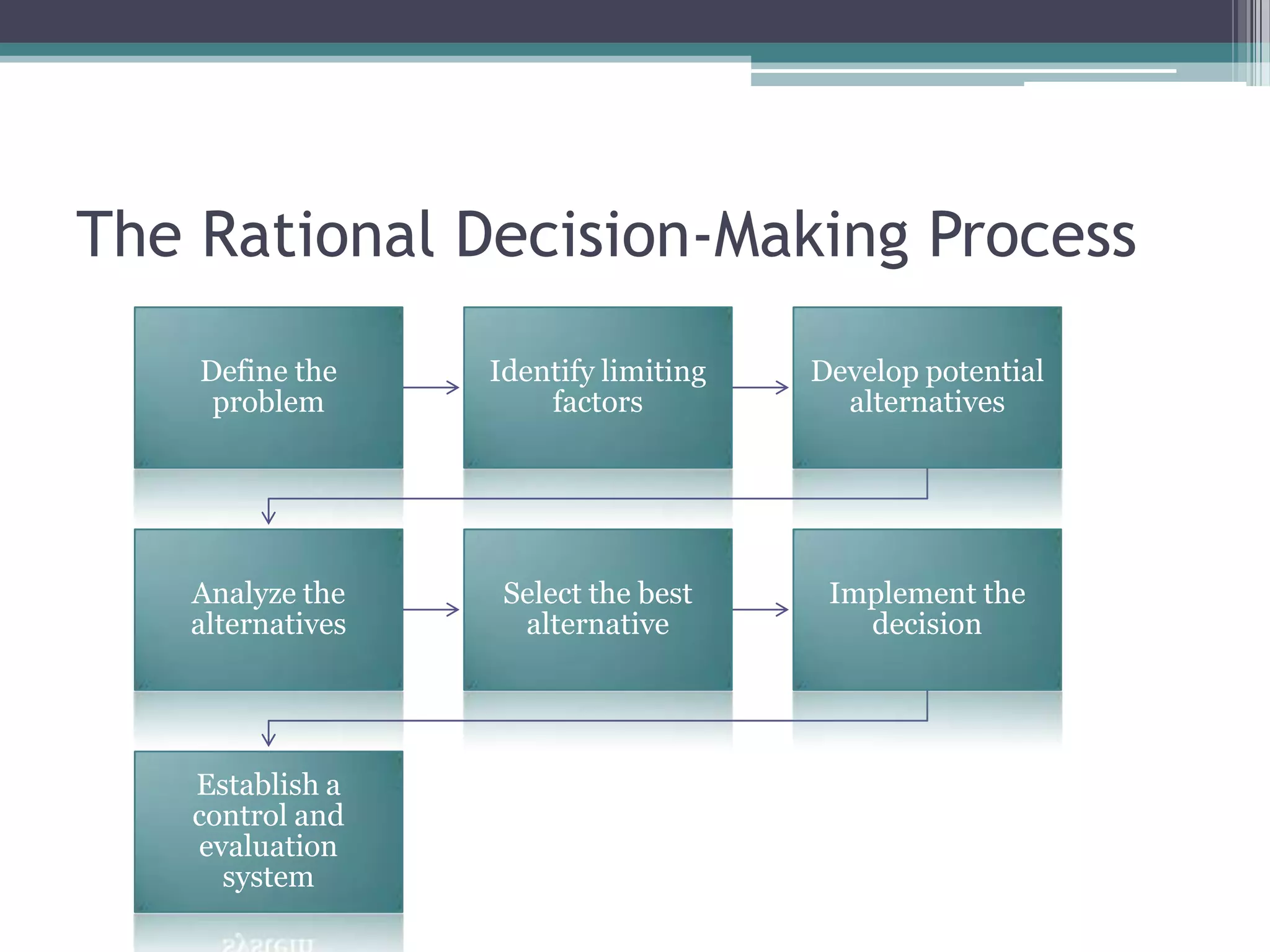

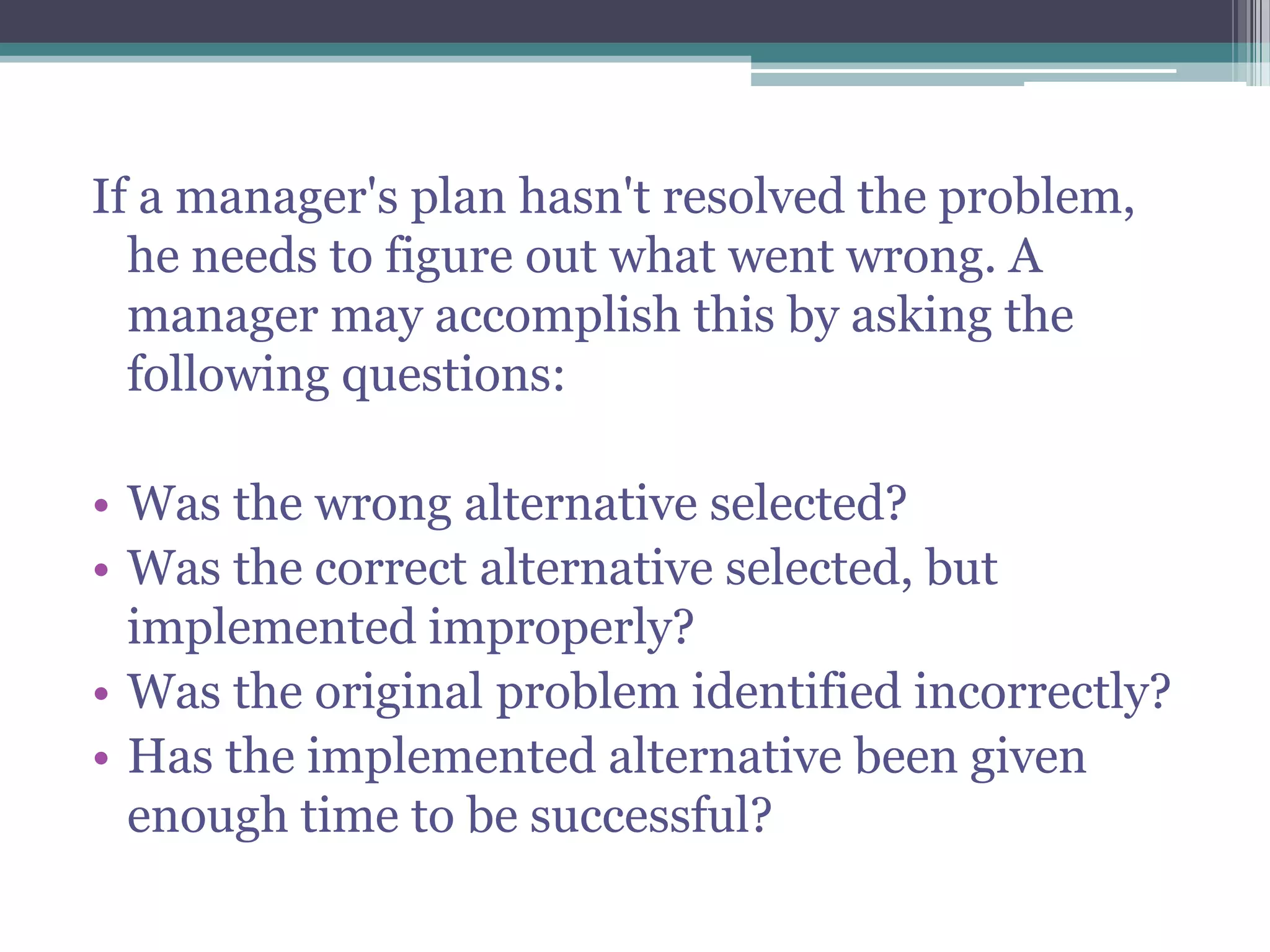

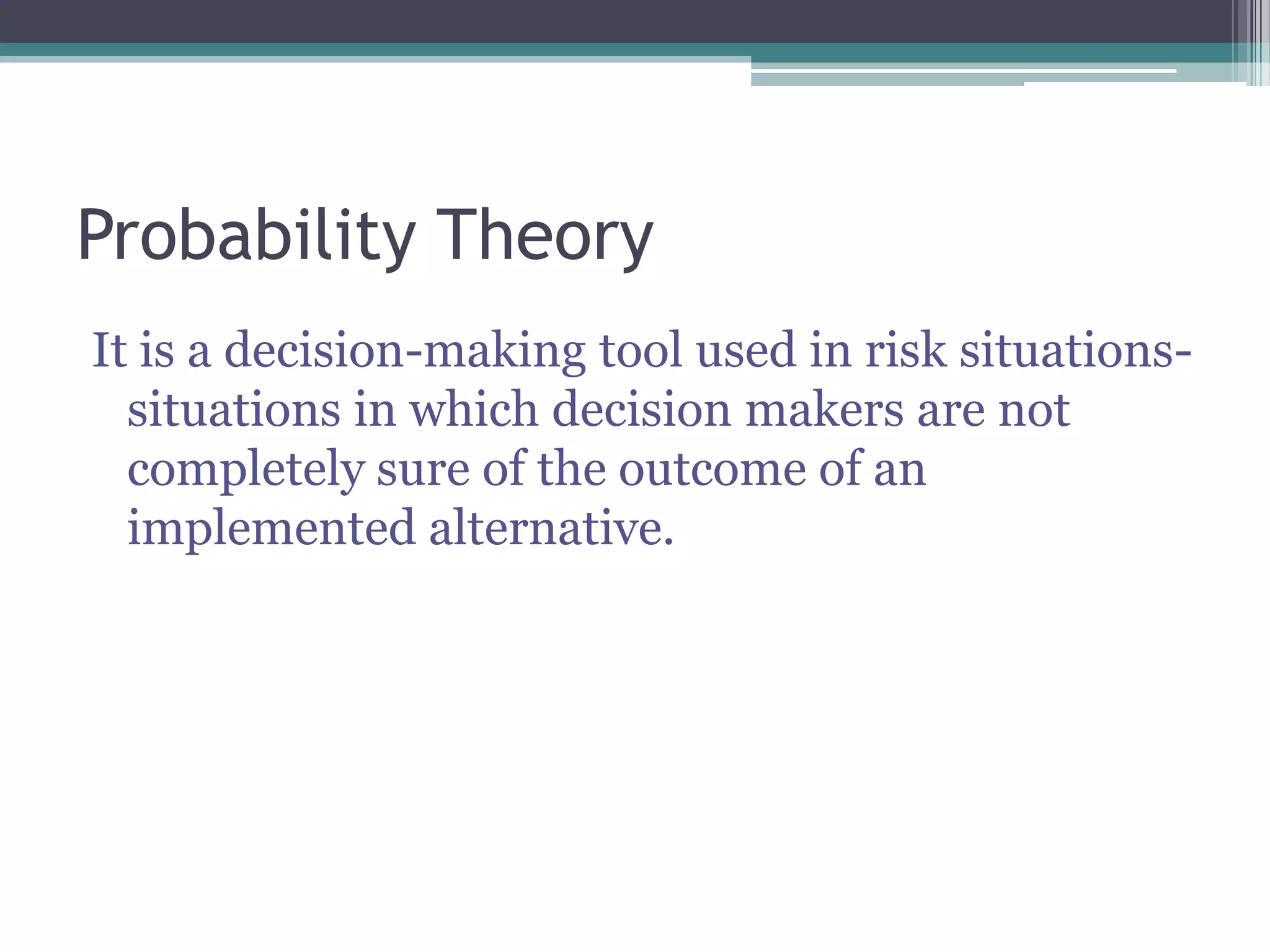

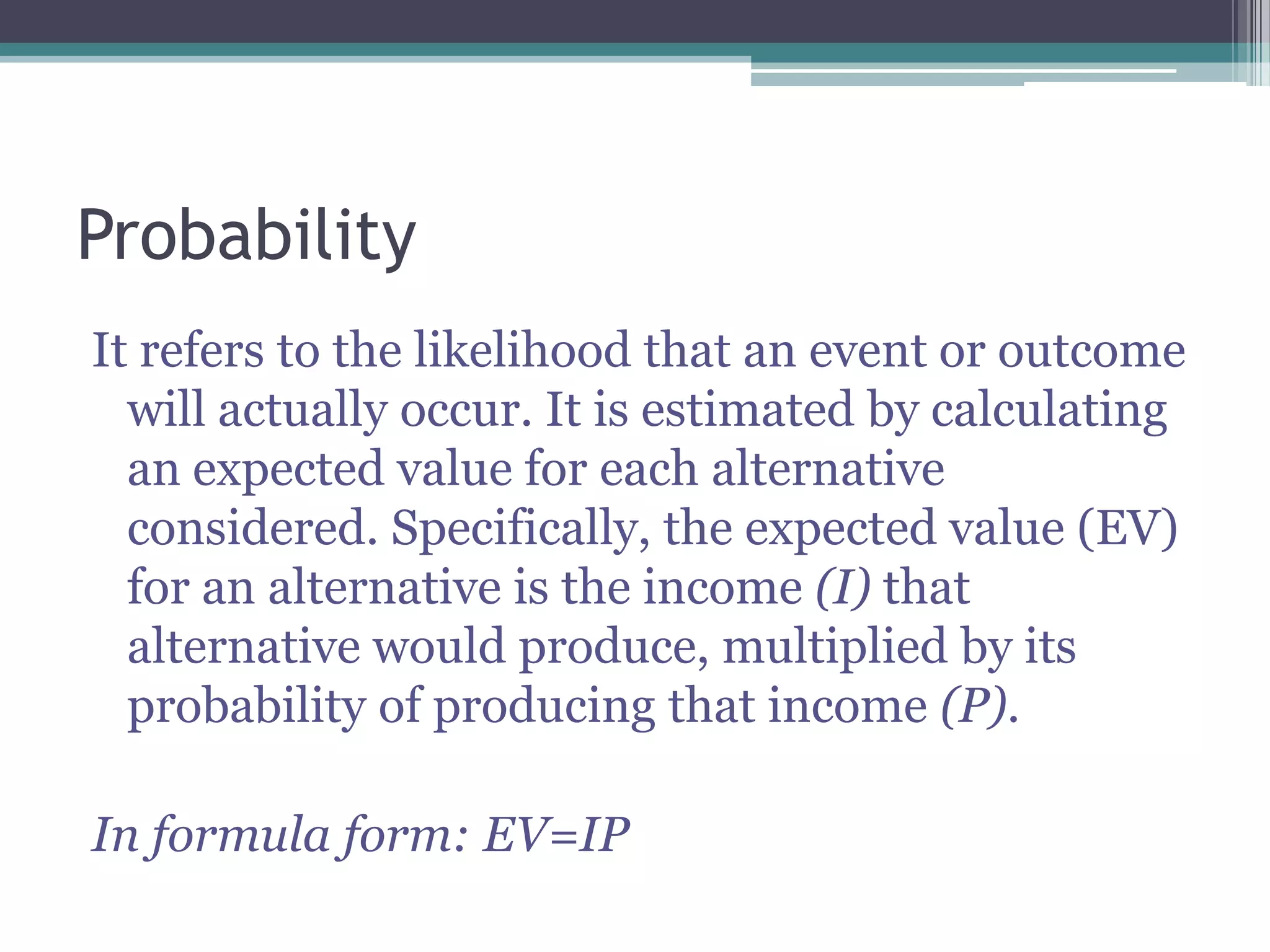

The document discusses decision making and provides information on key concepts related to the decision making process. It defines what a decision is, the different types of decisions (programmed vs non-programmed), elements of the decision making situation, conditions like risk and uncertainty, and the rational decision making process. It also covers tools that can be used, including probability theory, decision trees, and concepts like expected value. The overall document serves to outline the fundamental concepts involved in decision making.