Q3 2024 Earnings Conference Call and Webcast Slides

Dena Bank

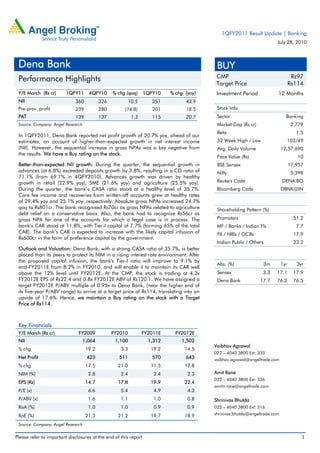

1. 1QFY2011 Result Update | Banking

July 28, 2010

Dena Bank BUY

Performance Highlights CMP Rs97

Target Price Rs114

Y/E March (Rs cr) 1QFY11 4QFY10 % chg (qoq) 1QFY10 % chg (yoy) Investment Period 12 Months

NII 360 326 10.5 251 43.9

Pre-prov. profit 239 280 (14.8) 201 18.5 Stock Info

PAT 139 137 1.3 115 20.7 Sector Banking

Source: Company, Angel Research Market Cap (Rs cr) 2,779

Beta 1.5

In 1QFY2011, Dena Bank reported net profit growth of 20.7% yoy, ahead of our

estimates, on account of higher-than-expected growth in net interest income 52 Week High / Low 102/49

(NII). However, the sequential increase in gross NPAs was a key negative from Avg. Daily Volume 12,57,690

the results. We have a Buy rating on the stock.

Face Value (Rs) 10

Better-than-expected NII growth: During the quarter, the sequential growth in BSE Sensex 17,957

advances (at 6.8%) exceeded deposits growth by 3.8%, resulting in a CD ratio of Nifty 5,398

71.1% (from 69.1% in 4QFY2010). Advances growth was driven by healthy

growth in retail (22.9% yoy), SME (21.6% yoy) and agriculture (25.5% yoy). Reuters Code DENA.BO

During the quarter, the bank’s CASA ratio stood at a healthy level of 35.7%. Bloomberg Code DBNK@IN

Core fee income and recoveries from written-off accounts grew at healthy rates

of 29.4% yoy and 25.1% yoy, respectively. Absolute gross NPAs increased 24.7%

qoq to Rs801cr. The bank recognised Rs70cr as gross NPAs related to agriculture Shareholding Pattern (%)

debt relief on a conservative basis. Also, the bank had to recognize Rs56cr as

gross NPA for one of the accounts for which a legal case is in process. The Promoters 51.2

bank’s CAR stood at 11.8%, with Tier-I capital of 7.7% (forming 65% of the total MF / Banks / Indian Fls 7.7

CAR). The bank’s CAR is expected to increase with the likely capital infusion of FII / NRIs / OCBs 17.9

Rs600cr in the form of preference capital by the government.

Indian Public / Others 23.2

Outlook and Valuation: Dena Bank, with a strong CASA ratio of 35.7%, is better

placed than its peers to protect its NIM in a rising interest rate environment. After

the proposed capital infusion, the bank's Tier-I ratio will improve to 9.1% by

Abs. (%) 3m 1yr 3yr

end-FY2011E from 8.2% in FY2010, and will enable it to maintain its CAR well

above the 12% level until FY2012E. At the CMP, the stock is trading at 4.3x Sensex 3.3 17.1 17.9

FY2012E EPS of Rs22.4 and 0.8x FY2012E ABV of Rs120.1. We have assigned a Dena Bank 17.7 76.2 76.5

target FY2012E P/ABV multiple of 0.95x to Dena Bank, (near the higher end of

its five-year P/ABV range) to arrive at a target price of Rs114, translating into an

upside of 17.6%. Hence, we maintain a Buy rating on the stock with a Target

Price of Rs114.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

NII 1,064 1,100 1,312 1,502

Vaibhav Agrawal

% chg 19.2 3.3 19.2 14.5

022 – 4040 3800 Ext: 333

Net Profit 423 511 570 643 vaibhav.agrawal@angeltrade.com

% chg 17.5 21.0 11.5 12.8

NIM (%) 2.8 2.4 2.4 2.3 Amit Rane

022 – 4040 3800 Ext: 326

EPS (Rs) 14.7 17.8 19.9 22.4

amitn.rane@angeltrade.com

P/E (x) 6.6 5.4 4.9 4.3

P/ABV (x) 1.6 1.1 1.0 0.8 Shrinivas Bhutda

RoA (%) 1.0 1.0 0.9 0.9 022 – 4040 3800 Ext: 316

RoE (%) 21.3 21.2 19.7 18.9 shrinivas.bhutda@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Dena Bank | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 performance

% chg % chg

Particulars (Rs cr) 1QFY11 4QFY10 1QFY10

(qoq) (yoy)

Interest earned 1,115 1,063 4.8 968 15.1

Interest expenses 754 737 2.3 718 5.0

NII 360 326 10.5 251 43.9

Non-interest income 107 175 (38.8) 155 (31.1)

Total income 468 501 (6.7) 406 15.2

Operating expenses 229 221 3.7 205 12.0

Pre-prov. profit 239 280 (14.8) 201 18.5

Provisions & cont. 43 82 (48.0) 41 5.4

PBT 196 198 (1.0) 161 21.8

Prov. for taxes 57 61 (6.0) 46 24.8

PAT 139 137 1.3 115 20.7

EPS (Rs) 4.8 4.8 1.3 4.0 20.7

Cost-to-income ratio (%) 49.0 44.1 50.4

Effective tax rate (%) 29.1 30.7 28.4

Net NPA (%) 1.5 1.2 1.3

Source: Company, Angel Research

Exhibit 2: 1QFY2011 actual v/s Angel estimates

Particulars (Rs cr) Actual Estimates Var. (%)

Net interest income 360 297 21.4

Non-interest income 107 126 (14.9)

Total income 468 423 10.6

Operating expenses 229 215 6.7

Pre-prov. profit 239 208 14.6

Provisions & cont. 43 40 6.1

PBT 196 168 16.6

Prov. for taxes 57 48 18.1

PAT 139 120 16.0

Source: Company, Angel Research

July 28, 2010 2

3. Dena Bank | 1QFY2011 Result Update

Advances growth well above deposits growth

In 1QFY2011, advances grew 33.8% yoy to Rs37,884cr and deposits grew by

24.7% yoy to Rs53,311cr. Sequential growth in advances (at 6.8%) exceeded

deposits growth by 3.8%, resulting in a 200bp improvement in CD ratio to 71.1%

from 69.1% in 4QFY2010. Advances growth was driven by strong growth in retail

(22.9% yoy), SME (21.6% yoy) and agriculture (25.5% yoy).

Exhibit 3: Trend in advances and deposits

Advances Deposits CD Ratio (%)

60,000 72.0

50,000 70.0

40,000 68.0

(Rs cr)

30,000 66.0

20,000 64.0

10,000 62.0

- 60.0

4QFY10

1QFY11

Q4FY08

Q1FY09

Q2FY09

Q3FY09

Q4FY09

Q1FY10

Q3FY10

Q3FY10

Source: Company, Angel Research

Exhibit 4: Trend in CASA deposits

(%) CASA Ratio

36.2

36.0

36.0

35.8 35.7

35.6

35.6 35.5

35.4

35.2

35.2

35.0

34.8

34.6

1QFY10

Q3FY10

Q3FY10

4QFY10

1QFY11

Source: Company, Angel Research

Robust NII growth

During the quarter, the bank’s NII grew by 43.9% yoy and 10.5% qoq to Rs360cr

because of a ~200bp sequential improvement in CD ratio. The reported NIM

remained stable sequentially at 2.8% in 1QFY2011, but improved from 2.4% in

1QFY2010. This was largely because of the 25bp qoq reduction in cost of deposits

to 5.67% on account of repricing of high-cost deposits. CASA deposits increased

by 26.5% yoy to Rs19,026cr, driven by 20.6% and 28.4% yoy growth in current

and savings deposits, respectively. During the quarter, the bank’s CASA ratio stood

at a healthy level of 35.7%.

July 28, 2010 3

4. Dena Bank | 1QFY2011 Result Update

Lower treasury, but healthy core fee and recoveries

Core fee income and recoveries from written-off accounts grew at healthy rates of

29.4% yoy and 25.1% yoy, respectively. However, total non-interest income

declined by 31.1% yoy to Rs107cr because of a sharp decline in treasury gains by

87.6% yoy to Rs9.8cr.

Pressure on asset quality

The bank’s absolute gross NPAs increased 24.7% sequentially to Rs801cr in

1QFY2010. The gross slippage ratio deteriorated to 2.7% (annualised) from 2.2%

in FY2010. The bank recognised Rs70cr as gross NPAs related to agriculture debt

relief during the quarter on a conservative basis. Also, the bank had to recognize

Rs56cr as gross NPA for one of the accounts for which a legal case is in process.

Consequently, gross NPA and net NPA ratios deteriorated to 2.1% (1.8% in

4QFY2010) and 1.5% (1.2% in 4QFY2010), respectively. The NPA provision

coverage ratio stood at 74.1%, including technical write-offs. The bank’s

cumulative restructuring stood at Rs1,340cr and formed 3.5% of advances and

52% of net worth. In 1QFY2011, there was a slippage of Rs15cr from restructured

accounts, taking total slippages from restructured accounts to 7% of advances.

Exhibit 5: Trend in asset quality

(Rs Cr) Gross NPAs Net NPAs Coverage Ratio (%) (%)

900 100

80

600

60

300

40

0 20

Q4FY08

Q1FY09

Q2FY09

Q3FY09

Q4FY09

Q1FY10

Q2FY10

Q3FY10

4QFY10

1QFY11

Source: Company, Angel Research Note: Coverage ratio for 4QFY10& 1QFY11 including tech.

write-offs

Investment book

Out of the total investment portfolio of Rs16,202cr, 11% is in AFS and the rest is in

HTM. During the quarter, the modified duration of AFS stood at 4.8 years and that

of HTM was 5.2 years, exposing the portfolio to rising interest rate risk.

July 28, 2010 4

5. Dena Bank | 1QFY2011 Result Update

Improved productivity

During the quarter, total operating expenses increased by 12.0% yoy to Rs229cr,

driven by 10.9% growth in employee costs and 13.8% growth in other operating

expenses. The cost-to-income ratio improved yoy to 49.0% in 1QFY2011 (44.1%

in 1QFY2010 and 50.4% in 1QFY2010). The branch network increased by 14 to

1,237. Currently, the bank has 66 licenses pending and aims to utilise all of them

during 2QFY2011E.The bank also opened 25 new ATMs during the quarter taking

the ATM network to 421.

Exhibit 6: Trend in productivity

(%) Cost-to-income ratio

60.0 56.6 56.0 55.9

53.3 52.5

50.0 50.0 50.5 50.4 49.0

50.0 45.9

42.7 44.1

40.0

30.0

20.0

10.0

-

1QFY08

2QFY08

3QFY08

4QFY08

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

Q3FY10

Q3FY10

4QFY10

1QFY11

Source: Company, Angel Research

Capital infusion expected in 2QFY2011E

During the quarter, Dena Bank’s CAR stood at 11.9%, with Tier-I capital of 7.7%

(forming 65% of the total CAR). The bank’s CAR is expected to increase with the

likely capital infusion of Rs600cr in the form of preference capital by the

government in FY2011. Further, management expects to receive Rs700cr from the

government in the form of preference capital over FY2012–13E. The cost of this

capital is expected to be linked to the repo rate, as per management’s indications.

Accordingly, we have assumed the cost of preference capital to be 7%. After the

proposed capital infusion, the bank's Tier-I ratio will improve to 9.1% by end-

FY2011E from 7.7% in 1QFY2011, enabling it to grow its advances in line with

peers.

July 28, 2010 5

6. Dena Bank | 1QFY2011 Result Update

Investment Arguments

Structurally strong CASA

Dena Bank has maintained its CASA ratio at healthy 35.7% levels (FY2010), on

account of having 63% of its branches in Gujarat and Maharashtra, where

prosperity levels are relatively high. In the last two years, the bank has maintained

a CASA market share of 1.1% despite intense competition from the private banks.

This structural advantage is reflected in the bank's one of the lowest cost of funds

at 5.9% in FY2010 compared to its peers.

Capital infusion to enable further growth

Dena Bank's CAR at 11.9%, comprising only 7.7% of equity capital, is below

optimum levels (reflected in 22x leverage of the bank for FY2010). Moreover, the

Government of India’s holding at 51% prevented the bank from diluting the

government stake further. This constraint on raising equity for growth was an

overhang on the stock. However, the government has consistently been reiterating

its intention to infuse capital in PSU banks. Against this backdrop, Dena Bank is

expected to receive Rs600cr over the next three months. Post capital infusion, the

bank's Tier-I will improve to 9.1% in FY2011E from 7.7% in Q1FY2011, enabling it

to grow its advances in line with peers.

Lower provisioning to aid bottom-line growth

Dena Bank's gross and net NPAs stood at 2.1% and 1.5%, respectively, in

1QFY2011, with cumulative restructured advances at Rs1,334cr (3.5% of loans).

As per a recent RBI circular, the bank's effective provision coverage, including

technically written-off portfolio, is 74.1% as against the mandatory 70%, due to

which an adjustment to book value for NPAs is not required. Further, this portfolio

is expected to yield outsized income from recoveries relative to peers. Given the

improving economic outlook, we believe lower incremental provisioning costs will

aid the bank in maintaining its profitability levels.

Outlook and Valuation

Dena Bank, with a strong CASA ratio of 35.7%, is better placed than its peers to

protect its NIM in a rising interest rate environment. After the proposed capital

infusion, the bank's Tier-I ratio will improve to 9.1% by end-FY2011E from 8.2% in

FY2010, and will enable it to maintain its CAR well above the 12% level until

FY2012E. At the CMP, the stock is trading at 4.3x FY2012E EPS of Rs22.4 and

0.80x FY2012E ABV of Rs120.1. We have assigned a target FY2012E P/ABV

multiple of 0.95x to Dena Bank, (near the higher end of its five-year P/ABV range)

to arrive at a target price of Rs114, translating into an upside of 17.6%. Hence, we

maintain a Buy rating on the stock with a Target Price of Rs114.

July 28, 2010 6

7. Dena Bank | 1QFY2011 Result Update

Exhibit 7: Key assumptions

Earlier estimates Revised estimates

Particulars (%)

FY2011E FY2012E FY2011E FY2012E

Credit growth 17.0 17.0 18.0 18.0

Deposit growth 16.0 16.0 16.0 16.0

CASA ratio 35.1 34.5 35.1 34.5

NIMs 2.4 2.3 2.4 2.3

Other income growth (9.1) 5.8 (9.1) 5.8

Growth in staff expenses 10.0 14.0 10.0 14.0

Growth in other expenses 10.0 14.0 10.0 14.0

Slippages 2.2 2.0 2.2 2.0

Coverage ratio 85.2 86.0 85.2 86.0

Treasury gain/(loss) (% of investments) 0.3 0.3 0.3 0.3

Source: Company, Angel Research

Exhibit 8: Change in estimates

FY2011E FY2012E

Particulars (Rs cr) Earlier Revised Earlier Revised

% chg % chg

estimates estimates estimates estimates

NII 1,295 1,312 1.3 1,481 1,502 1.4

Non-interest income 535 535 - 567 567 -

Total income 1,830 1,847 0.9 2,048 2,068 1.0

Operating expenses 933 933 - 1,063 1,063 -

Pre-prov. profit 897 914 1.9 984 1,005 2.1

Provisions & cont. 155 154 (0.6) 145 148 1.8

PBT 742 760 2.4 839 857 2.1

Prov. for taxes 185 190 2.4 210 214 2.1

PAT 556 570 2.4 629 643 2.1

Source: Company, Angel Research

Exhibit 9: P/ABV Band

Price 0.4x 0.7x 1x 1.3x 1.6x

200

160

120

80

40

0

Jan-03

Jul-04

Jan-06

Jul-07

Jan-09

Jul-10

Apr-02

Apr-05

Apr-08

Oct-03

Oct-06

Oct-09

Source: Company, Angel Research, Bloomberg

July 28, 2010 7

11. Dena Bank | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Dena Bank

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 28, 2010 11