BPPG response - Options for Defined Benefit schemes - 19Apr24.pdf

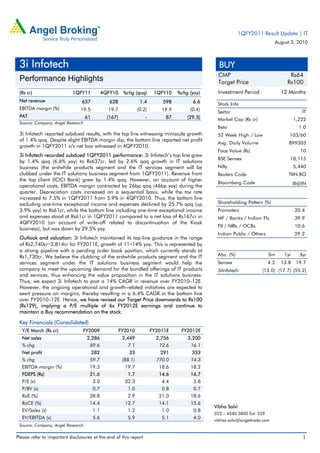

3i Infotech

1. 1QFY2011 Result Update | IT

August 3, 2010

3i Infotech BUY

CMP Rs64

Performance Highlights Target Price Rs100

(Rs cr) 1QFY11 4QFY10 %chg (qoq) 1QFY10 %chg (yoy) Investment Period 12 Months

Net revenue 637 628 1.4 598 6.6 Stock Info

EBITDA margin (%) 19.5 19.7 (0.2) 19.9 (0.4) Sector IT

PAT 61 (167) - 87 (29.5) Market Cap (Rs cr) 1,222

Source: Company, Angel Research

Beta 1.0

3i Infotech reported subdued results, with the top line witnessing miniscule growth 52 Week High / Low 103/60

of 1.4% qoq. Despite slight EBITDA margin dip, the bottom line reported net profit

Avg. Daily Volume 899303

growth in 1QFY2011 v/s net loss witnessed in 4QFY2010.

Face Value (Rs) 10

3i Infotech recorded subdued 1QFY2011 performance: 3i Infotech’s top line grew

BSE Sensex 18,115

by 1.4% qoq (6.6% yoy) to Rs637cr, led by 2.6% qoq growth in IT solutions

business (the erstwhile products segment and the IT services segment will be Nifty 5,440

clubbed under the IT solutions business segment from 1QFY2011). Revenue from Reuters Code TIIN.BO

the top client (ICICI Bank) grew by 1.4% qoq. However, on account of higher

Bloomberg Code III@IN

operational costs, EBITDA margin contracted by 26bp qoq (46bp yoy) during the

quarter. Depreciation costs increased on a sequential basis, while the tax rate

increased to 7.5% in 1QFY2011 from 5.9% in 4QFY2010. Thus, the bottom line

excluding one-time exceptional income and expenses declined by 25.7% qoq (up Shareholding Pattern (%)

3.9% yoy) to Rs61cr, while the bottom line including one-time exceptional income Promoters 20.4

and expenses stood at Rs61cr in 1QFY2011 compared to a net loss of Rs167cr in MF / Banks / Indian Fls 39.9

4QFY2010 (on account of write-off related to discontinuation of the Kiosk

FII / NRIs / OCBs 10.6

business), but was down by 29.5% yoy.

Indian Public / Others 29.2

Outlook and valuation: 3i Infotech maintained its top-line guidance in the range

of Rs2,740cr–2,814cr for FY2011E, growth of 11–14% yoy. This is represented by

a strong pipeline with a pending order book position, which currently stands at

Rs1,730cr. We believe the clubbing of the erstwhile products segment and the IT Abs. (%) 3m 1yr 3yr

services segment under the IT solutions business segment would help the Sensex 4.2 13.8 19.7

company to meet the upcoming demand for the bundled offerings of IT products 3iInfotech (13.0) (17.7) (55.2)

and services, thus enhancing the value proposition in the IT solutions business.

Thus, we expect 3i Infotech to post a 14% CAGR in revenue over FY2010–12E.

However, the ongoing operational and growth-related initiatives are expected to

exert pressure on margins, thereby resulting in a 6.4% CAGR in the bottom line

over FY2010–12E. Hence, we have revised our Target Price downwards to Rs100

(Rs129), implying a P/E multiple of 6x FY2012E earnings and continue to

maintain a Buy recommendation on the stock.

Key Financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net sales 2,286 2,449 2,756 3,200

% chg 89.6 7.1 12.6 16.1

Net profit 282 33 291 333

% chg 59.7 (88.1) 770.0 14.3

EBITDA margin (%) 19.3 19.7 18.6 18.2

FDEPS (Rs) 21.6 1.7 14.6 16.7

P/E (x) 3.0 32.3 4.4 3.8

P/BV (x) 0.7 1.0 0.8 0.7

RoE (%) 28.8 2.9 21.0 18.6

RoCE (%) 14.4 12.7 14.1 15.6

Vibha Salvi

EV/Sales (x) 1.1 1.2 1.0 0.8

022 – 4040 3800 Ext: 329

EV/EBITDA (x) 5.6 5.9 5.1 4.0

vibhas.salvi@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. 3i Infotech | 1Q FY2011Result Update

Exhibit 1: 1QFY2011 – Consolidated financial performance

Y/E March (Rs cr) 1QFY11 4QFY10 % chg 1QFY10 % chg FY2010 FY2009 % chg

(qoq) (yoy)

Total revenue 637 628 1.4 598 6.6 2,449 2,286 7.1

Operating costs 513 504 1.7 479 7.2 1,966 1,851 6.2

EBITDA 124 124 0.1 119 4.1 483 434 11.2

Interest 37 38 (1.7) 34 9.5 145 95 52.5

Depreciation & amortisation 26 1 - 29 (9.9) 81 70 16.2

Other income/(expense) 6 4 47.6 4 45.2 20 19 6.0

Income before income taxes 67 90 (25.1) 61 10.6 277 288 (4.0)

Income Taxes 5 5 (3.8) (2) - 11 22 (50.3)

Net income before minority

62 84 (26.4) 63 (1.4) 266 266 (0.2)

interest

Exceptional income - 11 (100.0) 28 (100.0) 28 26 7.3

Extraordinary expenses - (260) - - - (260) 0 -

Minority interest & share of

1 2 (54.1) 4 (77.8) (0) 10 (101.1)

assc. profits

PAT (before extra.ord. items) 61 93 (34.4) 87 (29.5) 294 282 4.2

PAT (after extra.ord. items) 61 (167) (136.6) 87 (29.5) 33 282 (88.1)

Diluted EPS (before extra.ord.

3.1 4.8 (34.4) 4.4 (29.5) 15.0 14.4 4.2

items)

Diluted EPS (after extra.ord.

3.1 (8.5) - 4.4 (29.5) 1.7 21.0 (91.9)

items)

EBITDA margin (%) 19.5 19.7 19.9 19.7 19.0

Net Profit margin (%) 9.6 14.8 14.5 12.0 12.3

Effective tax rate (%) 7.5 5.9 (3.7) 4.0 7.6

Source: Company, Angel Research

Top-line growth driven by IT solutions business

3i Infotech’s top line grew by 1.4% qoq (6.6% yoy) to Rs637cr, led by 2.6% qoq

growth (decline of 1.2% yoy) in the IT solutions business (the erstwhile products

segment and the IT services segment will be clubbed under the IT solutions

business segment from 1QFY2011).

The company has not witnessed any ramp downs in standalone IT products

business during the quarter, but it faced delays from Western Europe, Middle East

and far east markets. The clubbing of IT products with IT services was only for

redefining the product business to extract better value proposition.

However, the transaction services business witnessed a 0.5% qoq decline (22.2%

yoy growth) mainly due to volume decline witnessed in transaction services in the

US market.

Revenue from the company’s top client (ICICI Bank) grew 1.4% qoq. 3i Infotech

witnessed four new deal wins from the core banking domain. Growth remained

stable across geographies on a qoq basis, with good wins in the IT solutions

business; however, on a yoy basis, developed markets grew by 13.8%, while

emerging markets declined by 3.8%.

August 3, 2010 2

3. 3i Infotech | 1Q FY2011Result Update

Exhibit 2: Segment-wise gross revenue and margins

(Rs. cr) 1QFY11 4QFY10 1QFY10 % chg qoq % chg yoy

IT solutions

Revenue 394 384 398 2.6 (1.2)

Gross profit 173 177 183 (2.4) (5.5)

Gross margin (%) 44.0 46.2 46.0 (2.2) (2.0)

Transaction services (BPO)

Revenue 244 245 199 (0.5) 22.2

Gross profit 86 80 55 7.2 56.2

Gross margin (%) 35.1 32.6 27.5 2.5 7.7

Total

Revenue 637 628 598 1.4 6.6

Gross profit 259 257 238 0.6 8.7

Gross margin (%) 40.6 40.9 39.8 (0.3) 0.8

Source: Company Data, Angel Research; Note: Henceforth, the erstwhile products segment

and the IT services segment will be clubbed under the IT solutions segment

Subdued margins and one-time items drag the bottom line

Despite a 10% wage hike effective in 1QFY2011, 3i Infotech was able to maintain

EBITDA margin at 19.5%, thereby witnessing a slight dip of 26bp qoq (46bp yoy).

Depreciation cost grew on a sequential basis, while the tax rate increased from

5.9% in 4QFY2010 to 7.5% in 1QFY2011. Thus, the bottom line excluding one-

time exceptional income and Kiosk write-off declined by 25.7% qoq (up 3.9% yoy)

to Rs61cr, while bottom line including one-time exceptional income and Kiosk

write-off stood at Rs61cr in 1QFY2011 compared to a net loss of Rs167cr

reported in 4QFY2010 (on account of write-off related to discontinuation of the

Kiosk business), but was down by 29.5% yoy.

Exhibit 3: Gross margin and EBITDA margin trend

50

45

40

35

(%)

30

25

20

15

1QFY08

2QFY08

3QFY08

4QFY08

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Gross margins EBITDA margins

Source: Company Data, Angel Research

August 3, 2010 3

4. 3i Infotech | 1Q FY2011Result Update

Investment Arguments

Re-defining business to derive better value proposition

The clubbing of the erstwhile products segment and the IT services segment under

the IT solutions business segment would help 3i Infotech to meet the upcoming

demand for the bundled offerings of IT products and services. Further, through the

company’s global delivery centres, these integrated offerings are expected to get

a boost in demand, which will enhance the value proposition in the IT solutions

business by undertaking several cross-selling and up-selling opportunities. Further,

through the acquisitions of Regulus and JP Morgan Retail Lock box in the

transaction services segment, the company has now access to large BFSI clients in

the US market and can pitch for more integrated IT offerings in this segment.

Management’s FY2011E guidance maintained

Management continued to maintain its top-line growth guidance in the range of

Rs2,740cr–2,814cr for FY2011E, a yoy increase of 11–14%. This is represented by

a strong pipeline with a pending order book position (representing assured

revenue stream for the next seven months), which currently stands at Rs1,730cr,

comprising 60% of IT solutions business revenue and the remaining of transaction

services business. Growth in the IT solutions business is expected to be stronger

compared to that in the transaction services business. Though the transaction

services business remained subdued during 1QFY2011, it is expected to witness

growth through client acquisitions and vendor consolidations going forward.

Outlook and valuation

We expect 3i Infotech to post a 14% CAGR in revenue over FY2010–12E.

However, the ongoing operational and growth-related initiatives are expected to

exert pressure on margins, thereby resulting in a 6.4% CAGR in bottom line

(adjusted for one-time items) over FY2010–12E. Hence, we have revised our

Target Price downwards to Rs100 (Rs129), implying a P/E multiple of 6x FY2012E

earnings and continue to maintain a Buy recommendation on the stock.

Exhibit 4: Key assumptions

FY2011E FY2012E

Growth in IT solutions 15.0 20.0

Growth in transaction services 9.2 9.0

USD-INR rate (realised) 46.5 47.0

Revenue growth (in INR terms) 12.6 16.1

EBIDTA margin (%) 18.6 18.2

Tax rate (%) 10.0 15.0

EPS growth (%) (2.8) 14.3

Source: Company, Angel Research

August 3, 2010 4

5. 3i Infotech | 1Q FY2011Result Update

Exhibit 5: Change in estimates

FY2011E FY2012E

Parameter Earlier Revised Var. Earlier Revised Var.

(Rs cr) estimates estimates (%) estimates estimates (%)

Net revenue 2,734 2,756 0.8 3,197 3,200 0.1

EBIDTA 529 513 (3.1) 606 582 (3.9)

PBT 329 323 (1.8) 413 392 (5.3)

Tax 40 32 (18.1) 62 59 (5.3)

PAT 290 291 0.5 351 333 (5.3)

Source: Company, Angel Research

Considering the company’s strong order book and improved business

environment, we have slightly increased our top-line estimates. However, we

believe the ongoing operational and growth-related initiatives are expected to

exert pressure on margins, thereby resulting in lower-than-earlier expected growth

in profitability for FY2011E and FY2012E.

Exhibit 6: One-year forward P/E band

300

250

13x

Share Price (Rs)

200

10x

150

7x

100

4x

50

0

Oct-05

Oct-06

Oct-07

Oct-08

Oct-09

Feb-06

Feb-07

Feb-08

Feb-09

Feb-10

Jun-05

Jun-06

Jun-07

Jun-08

Jun-09

Jun-10

Source: Company, Angel Research

Exhibit 7: Recommendation summary

Company Reco. CMP Tgt. price Upside FY2012E FY2012E FY2010-12E FY2012E FY2012E

(Rs) (Rs) (%) P/BV (x) P/E (x) EPS CAGR (%) RoCE (%) RoE (%)

3i Infotech Buy 64 100 57.0 0.7 3.8 208.9 15.6 18.6

Educomp Buy 607 734 21.0 2.7 13.2 26.9 21.0 22.3

HCL Tech Accumulate 391 420 7.3 3.2 14.6 17.9 40.9 24.1

Infosys Neutral 2,785 2,900 4.1 4.6 20.2 12.6 33.1 25.0

Infotech Enterprises Buy 155 192 23.8 1.3 8.0 12.1 18.1 17.0

Mphasis Buy 594 872 46.9 2.4 9.2 14.9 41.6 29.2

NIIT Buy 66 83 25.3 1.7 11.5 16.6 12.1 15.8

TCS Accumulate 833 920 10.4 5.3 19.0 11.7 53.2 30.4

Tech Mahindra Buy 722 950 31.5 2.2 13.6 (0.5) 56.9 18.5

Wipro Accumulate 413 470 13.9 3.5 16.7 14.7 28.0 23.0

Source: Company, Angel Research

August 3, 2010 5

6. 3i Infotech | 1Q FY2011Result Update

Profit & Loss Statement (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Gross Sales 2,286 2,449 2,756 3,200

Less: Excise duty - - - -

Net Sales 2,286 2,449 2,756 3,200

Other operating income 19 20 22 26

Total operating income 2,305 2,469 2,778 3,226

% chg 88.4 7.1 12.5 16.1

Total Expenditure 1,845 1,966 2,243 2,618

Cost of Equipment 1,007 1,061 1,213 1,424

SGA 278 299 342 394

Cost of IT 513 553 634 736

Other 47 51 55 64

EBITDA 460 503 535 608

% chg 65.8 9.4 6.3 13.8

(% of Net Sales) 19.3 19.7 18.6 18.2

Depreciation & Amortisation 70 81 63 75

EBIT 390 422 472 533

% chg 54.1 8.2 11.9 12.9

(% of Net Sales) 17.0 17.2 17.1 16.7

Interest & other Charges 101 145 149 141

Other Income - -

(% of PBT) - - - -

Share in profit of Associates - - - -

Recurring PBT 289 277 323 392

% chg 58.4 (85.9) 630.1 21.1

Extraordinary Expense/(Inc.) (24.9) 232.6 - -

PBT (reported) 314 44 323 392

Tax 22 11 32 59

(% of PBT) 6.9 24.7 10.0 15.0

PAT (reported) 292 33 291 333

Add: Share of earnings of

- - - -

associate

Less: Minority interest (MI) (10.4) 0.1 - -

Prior period items - - - -

PAT after MI (reported) 282 33 291 333

ADJ. PAT 257 266 291 333

% chg 59.7 (88.1) 770.0 14.3

(% of Net Sales) 12.3 1.4 10.6 10.4

Basic EPS (Rs) 21.6 2.0 14.5 16.6

Fully Diluted EPS (Rs) 21.6 1.7 14.6 16.7

% chg 59.7 (88.1) 770.0 14.3

August 3, 2010 6

7. 3i Infotech | 1Q FY2011Result Update

Balance Sheet (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

SOURCES OF FUNDS

Equity Share Capital 131 169 200 200

Preference Capital 100 100 100 100

Reserves & Surplus 916 848 1,337 1,627

Shareholders’ Funds 1,146 1,117 1,637 1,928

Minority Interest 21 8 8 8

Total Loans 2,202 2,159 1,810 1,464

Deferred Tax Liability (39) (113) - -

Total Liabilities 3,331 3,172 3,455 3,399

APPLICATION OF FUNDS

Gross Block 800 645 720 795

Less: Acc. Depreciation 233 270 333 409

Net Block 567 374 386 386

Capital Work-in-Progress 126 54 14 14

Goodwill 1,700 1,811 1,811 1,811

Investments 4 10 10 10

Current Assets 1,423 1,524 1,792 1,842

Cash 320 190 351 289

Loans & Advances 332 504 534 559

Other 772 831 908 995

Current liabilities 488 602 559 664

Net Current Assets 935 922 1,233 1,178

Mis. Exp. not written off

Total Assets 3,331 3,172 3,455 3,399

Cash Flow (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Profit before tax 288 277 323 392

Depreciation 85 81 63 75

Change in Working Capital 92 (102) (7) 18

Less: Other income (104) (149) - -

Direct taxes paid 46 63 32 59

Cash Flow from Operations 524 342 347 426

(Inc)./ Dec in Fixed Assets (1,044) (419) (35) (75)

(Inc)./ Dec. in Investments 0 - - -

(Inc)./ Dec. in loans and

advances (0.11) 0 (30) (25)

Other income 2 4 - -

Cash Flow from Investing (1,041) (415) (65) (100)

Issue of Equity 1 310 271 -

Inc./(Dec.) in loans 626 (126) (349) (346)

Dividend Paid (Incl. Tax) 30 30 42 42

Others (fx effect) (27) (211) - -

Cash Flow from Financing 570 (57) (121) (388)

Inc./(Dec.) in Cash 53 (130) 161 (62)

Opening Cash balances 267 320 190 351

Closing Cash balances 320 190 351 289

August 3, 2010 7

9. 3i Infotech | 1Q FY2011Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement 3i Infotech

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 3, 2010 9