Downloaded 34 times

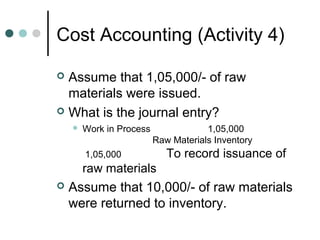

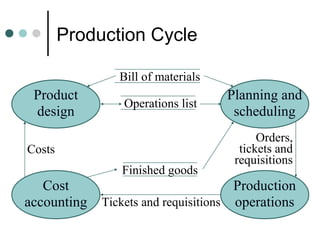

The production cycle consists of four main activities: 1) product design, 2) planning and scheduling, 3) production operations, and 4) cost accounting. The first step is product design which creates a bill of materials and operations list. The second step is planning and scheduling using methods like MRP-II or JIT. The third step is the actual production. Cost accounting, the final step, provides cost data using job-order or process costing systems by collecting data from tickets, requisitions and allocating overhead costs.