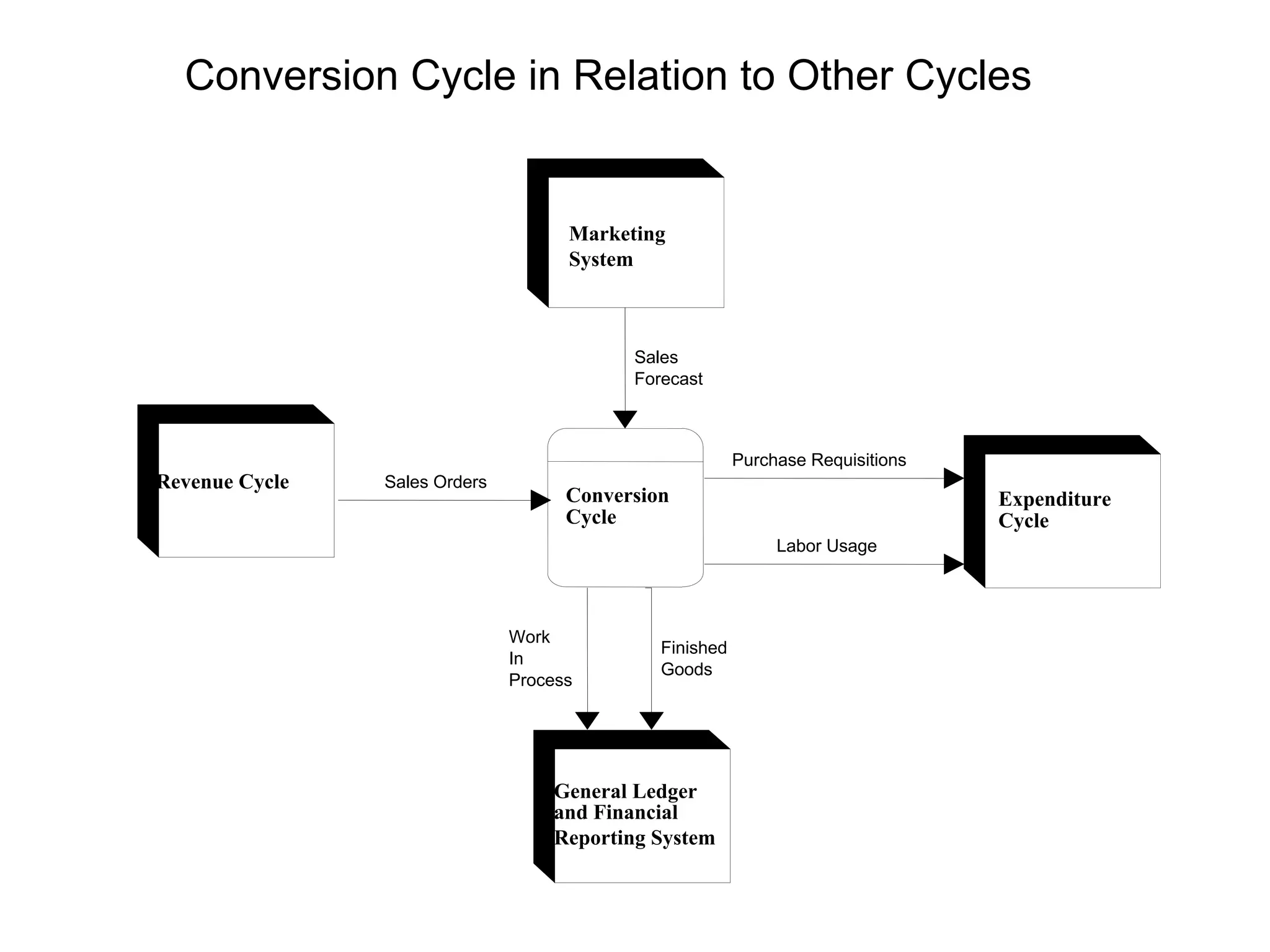

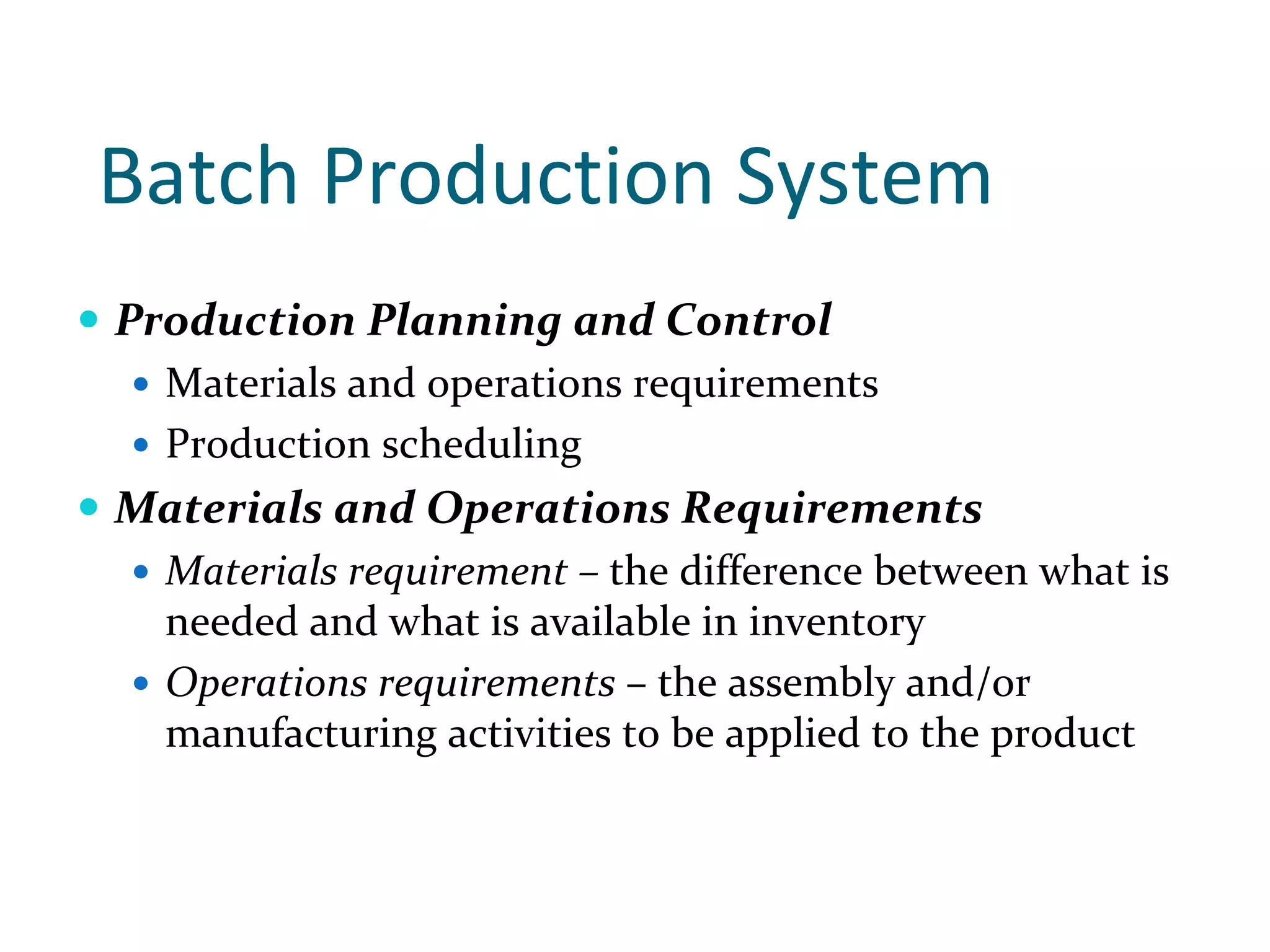

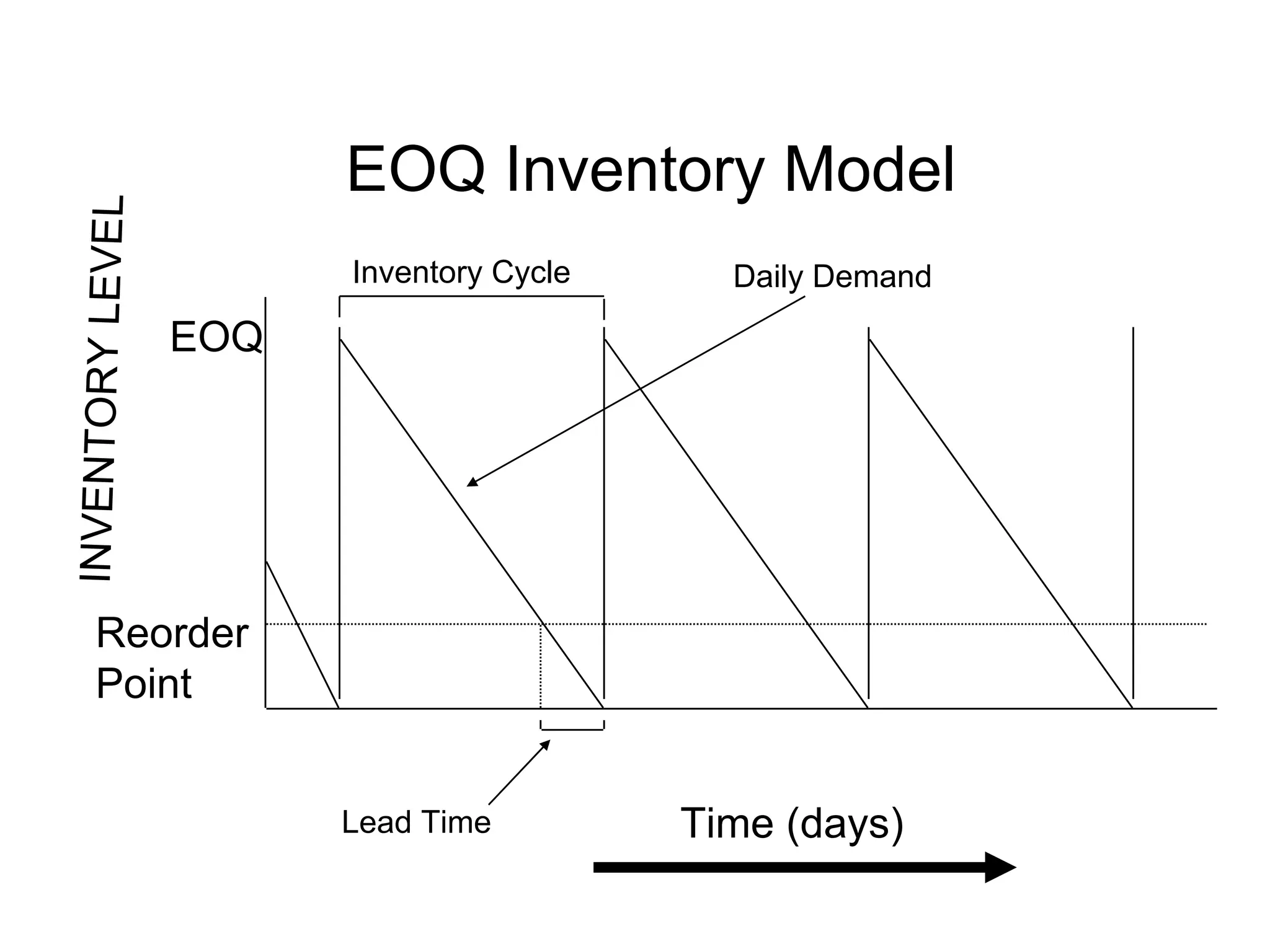

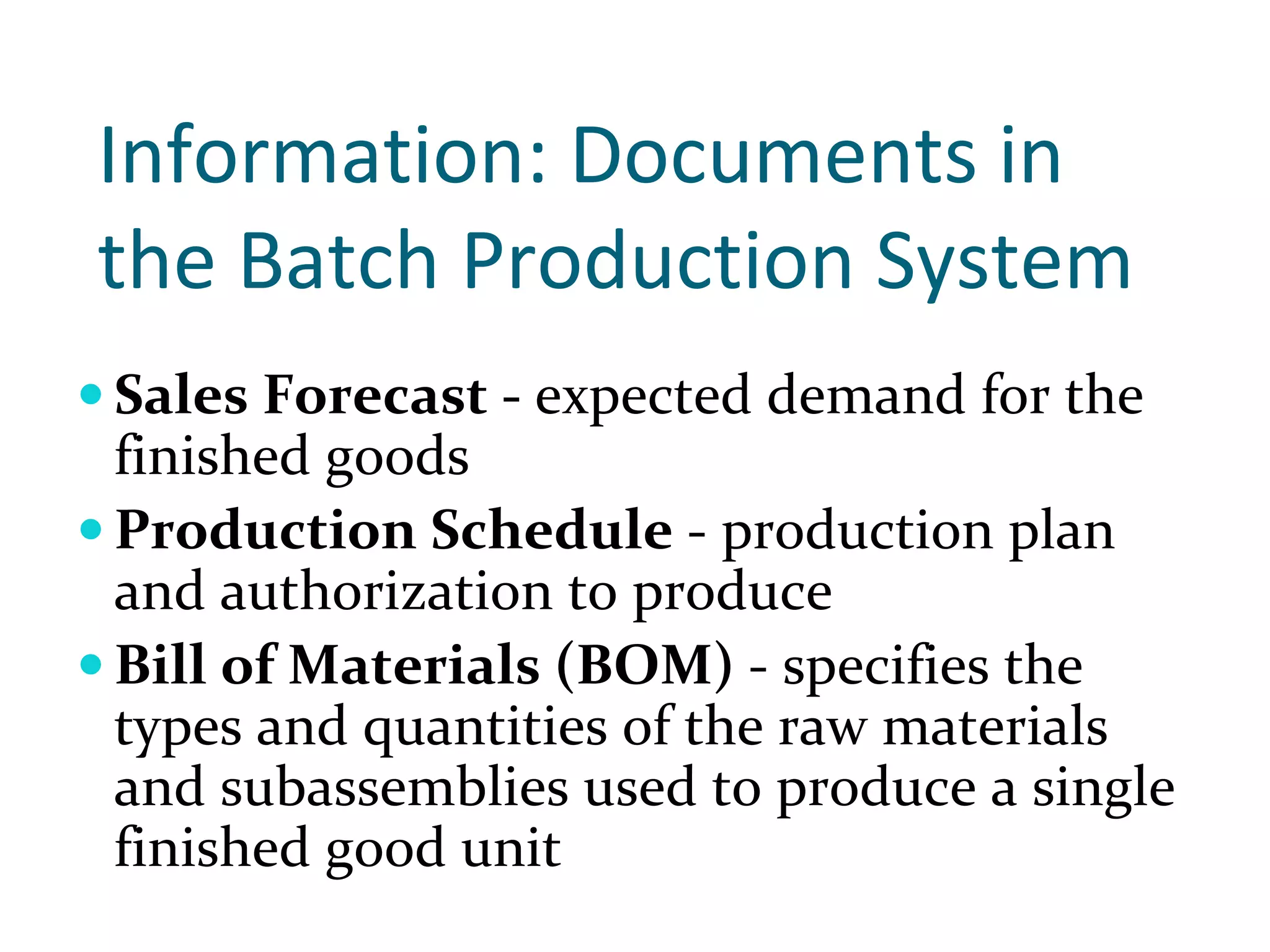

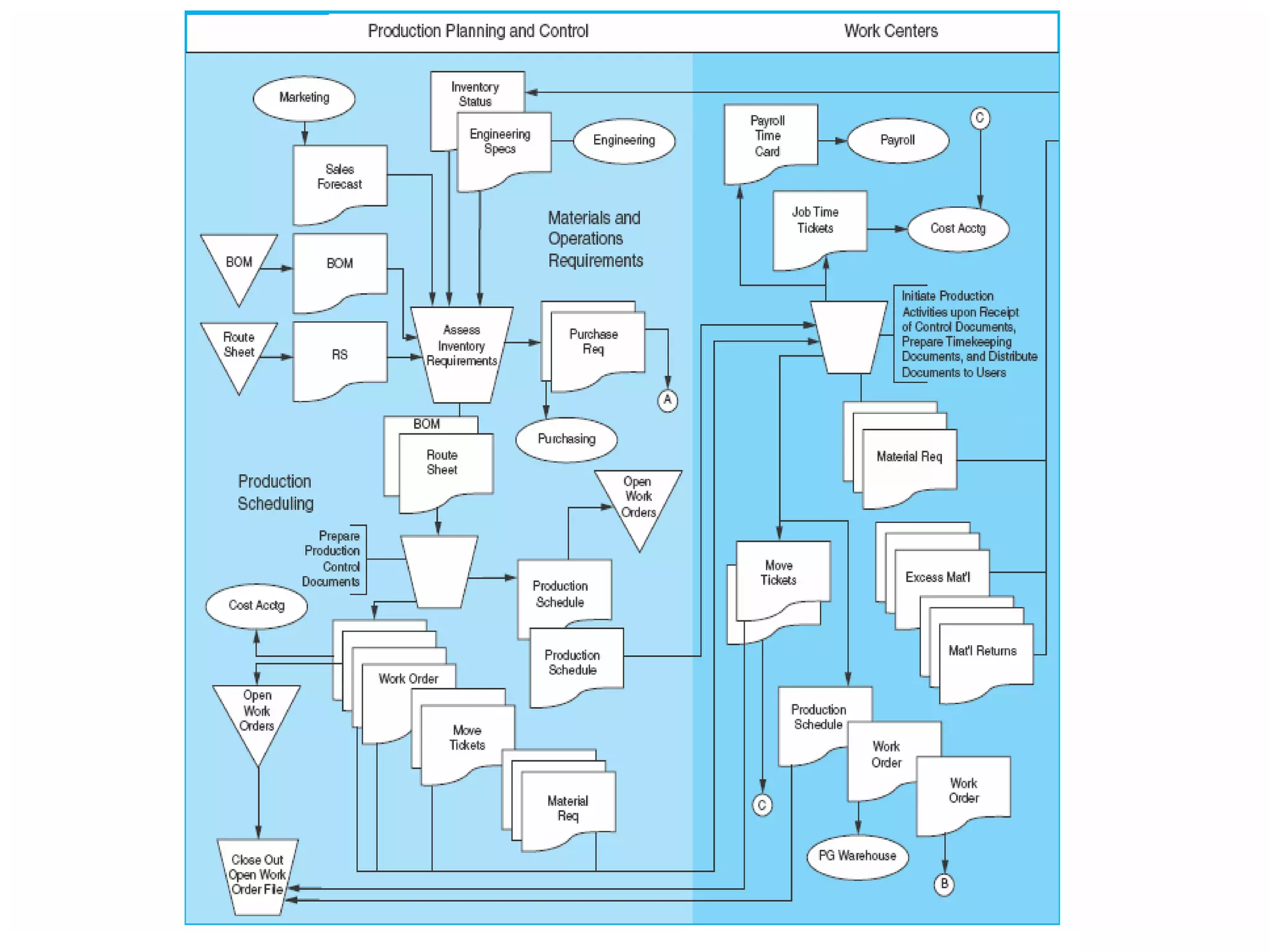

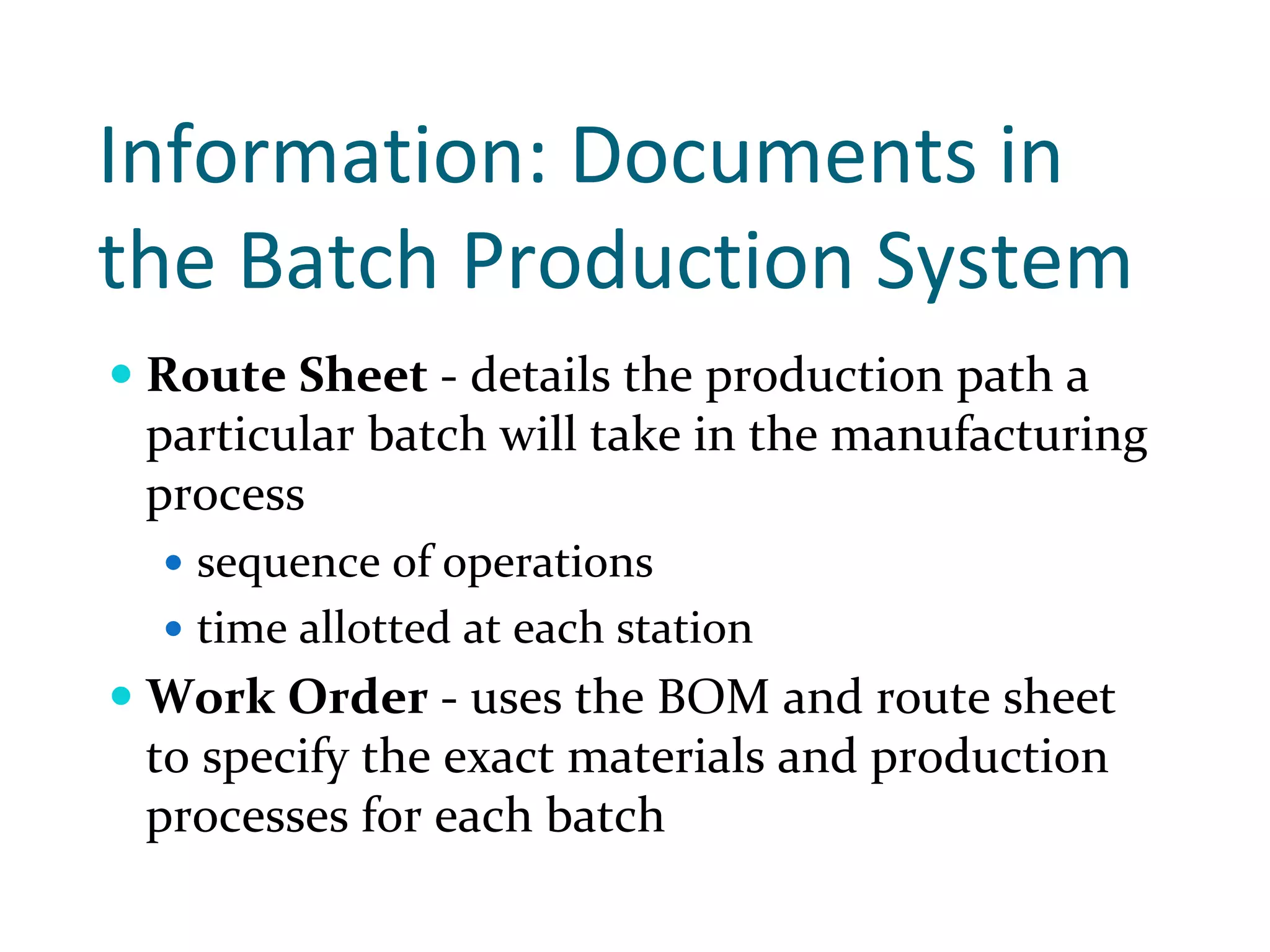

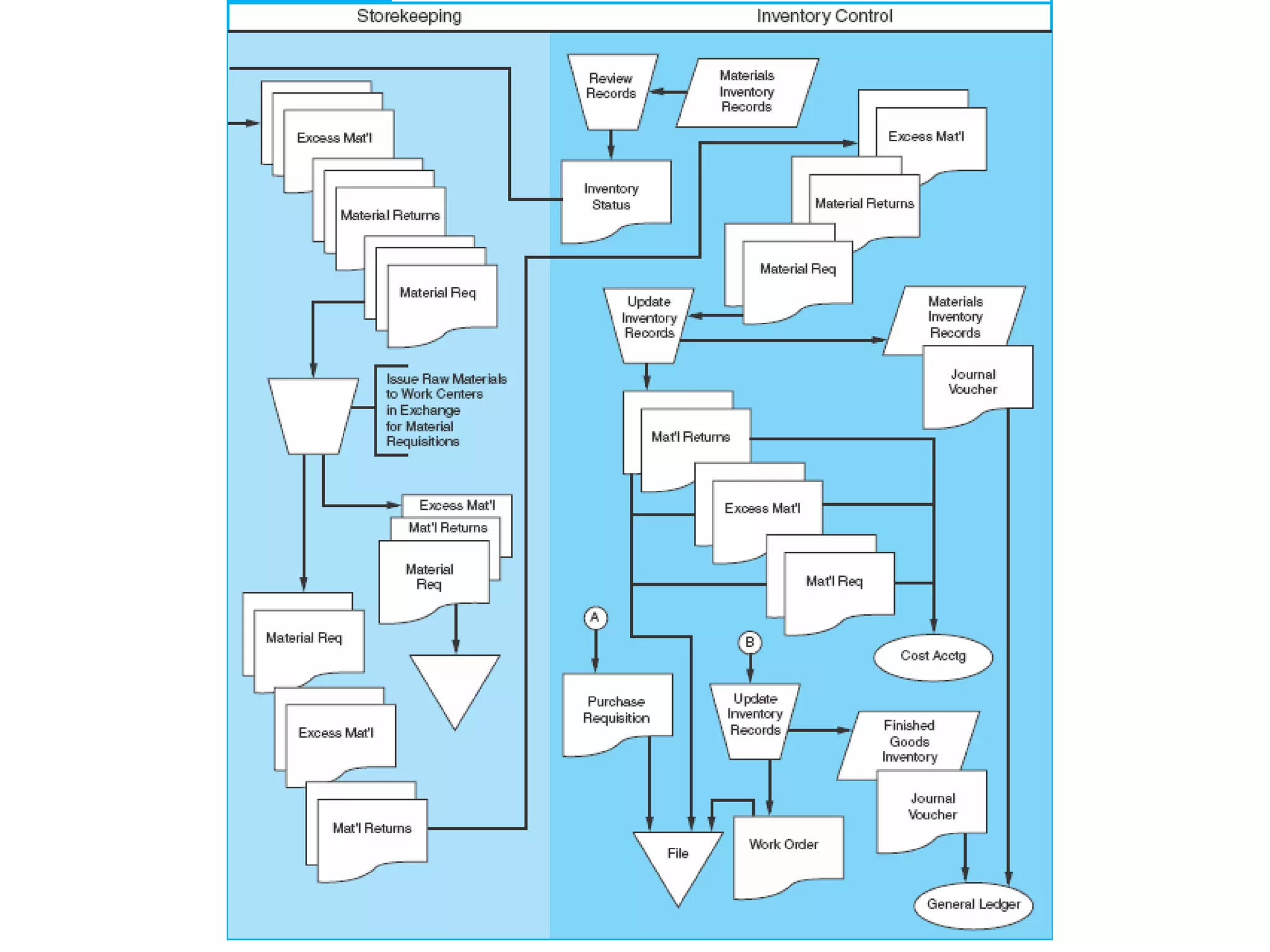

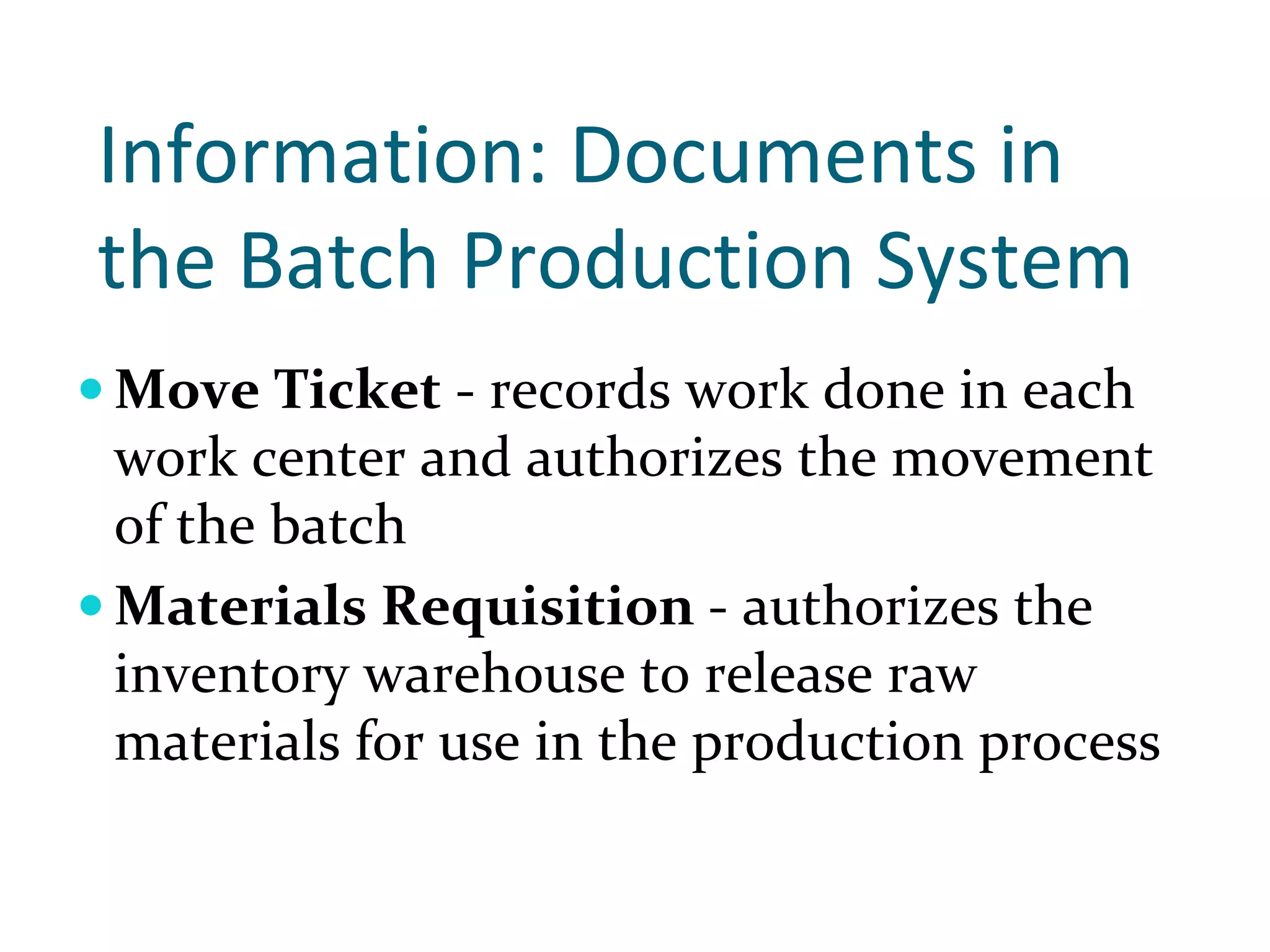

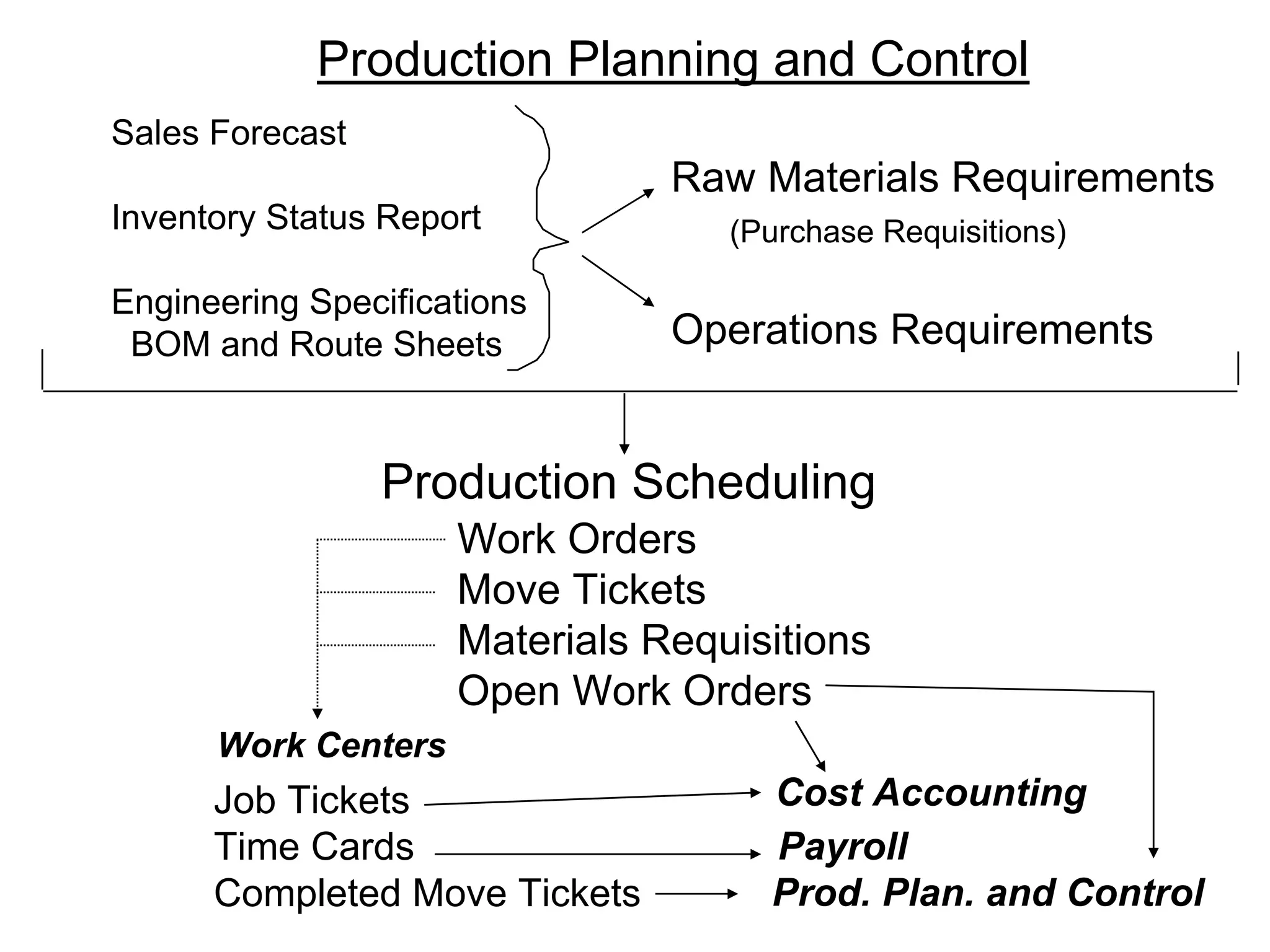

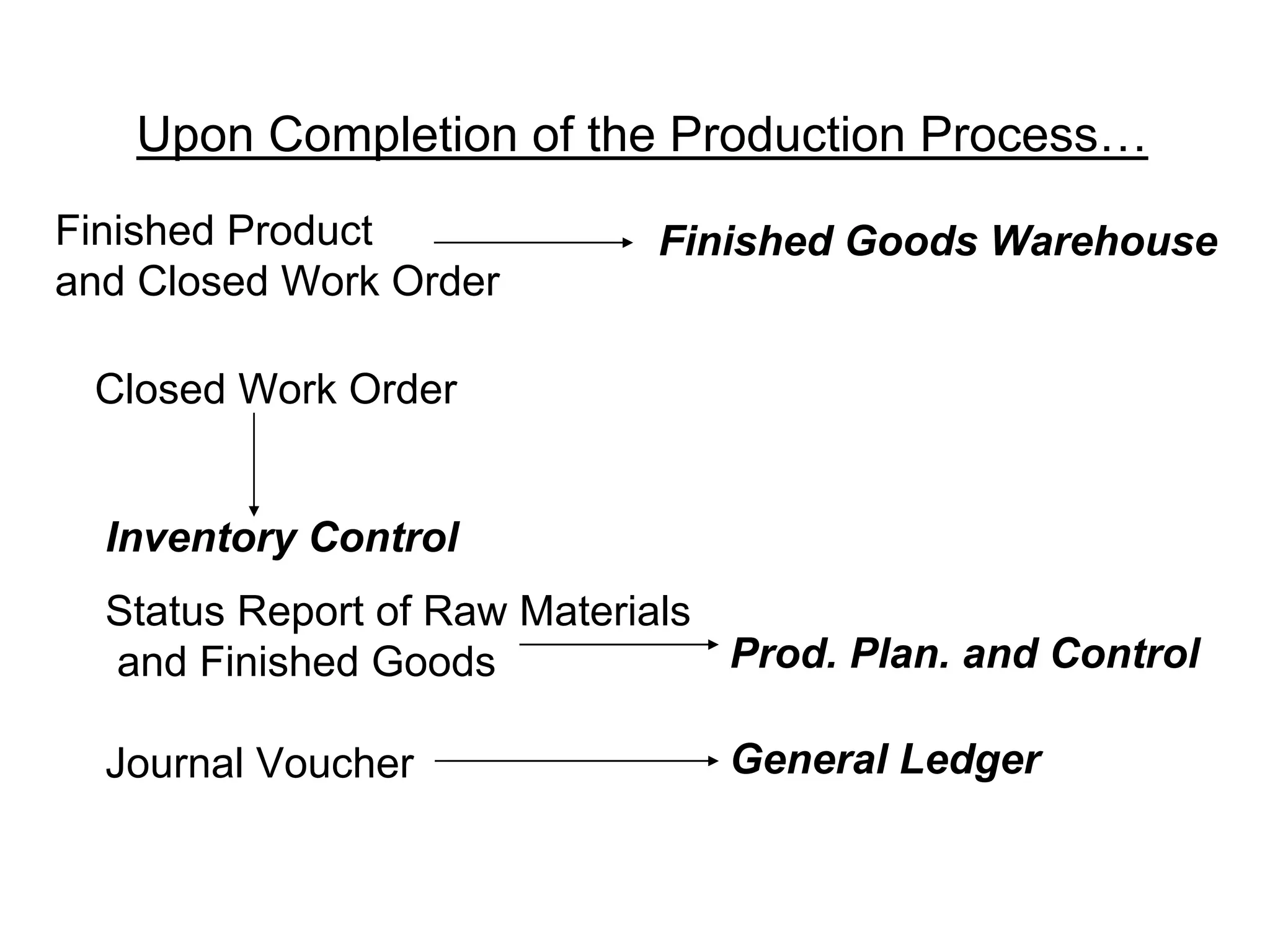

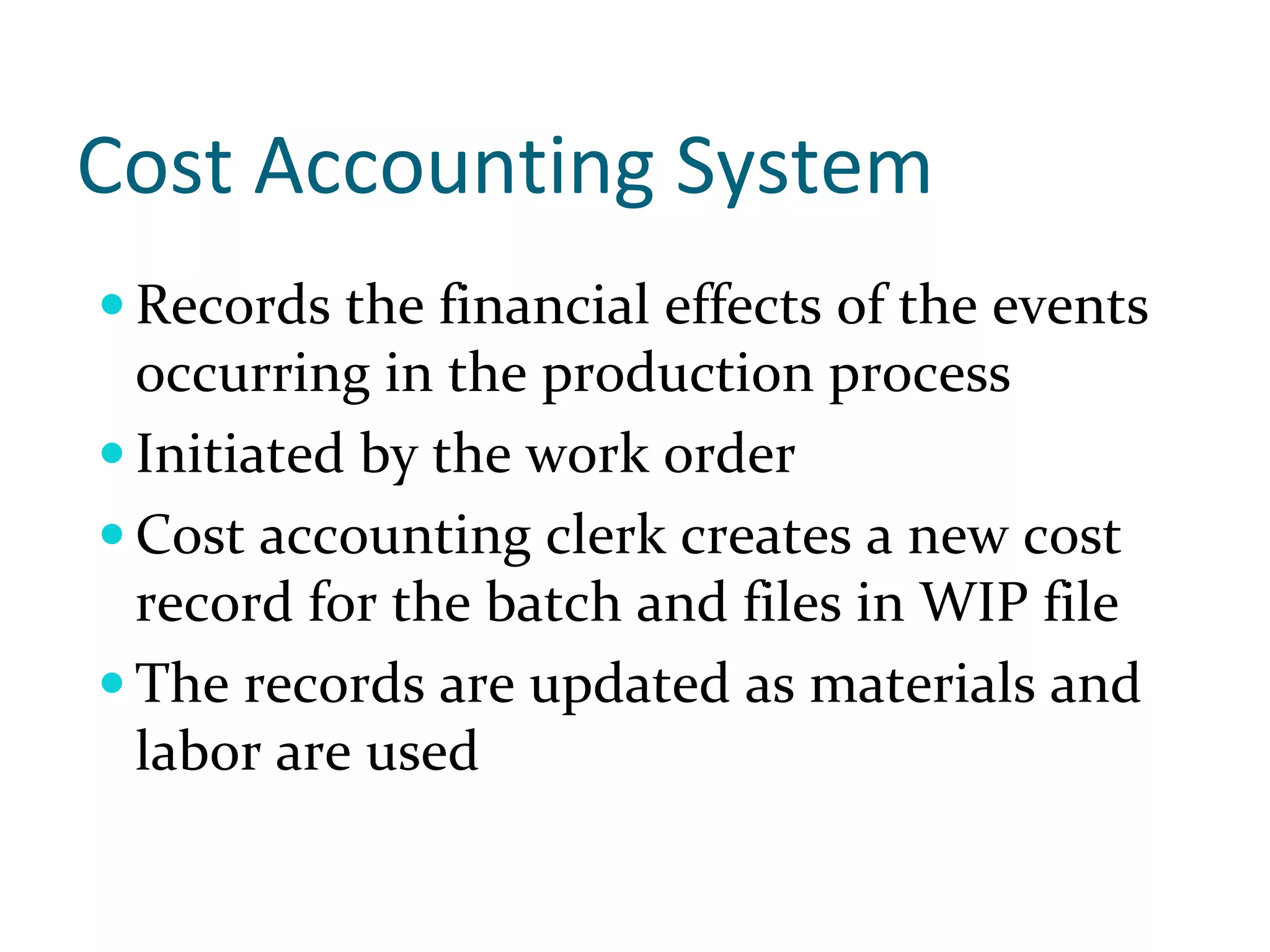

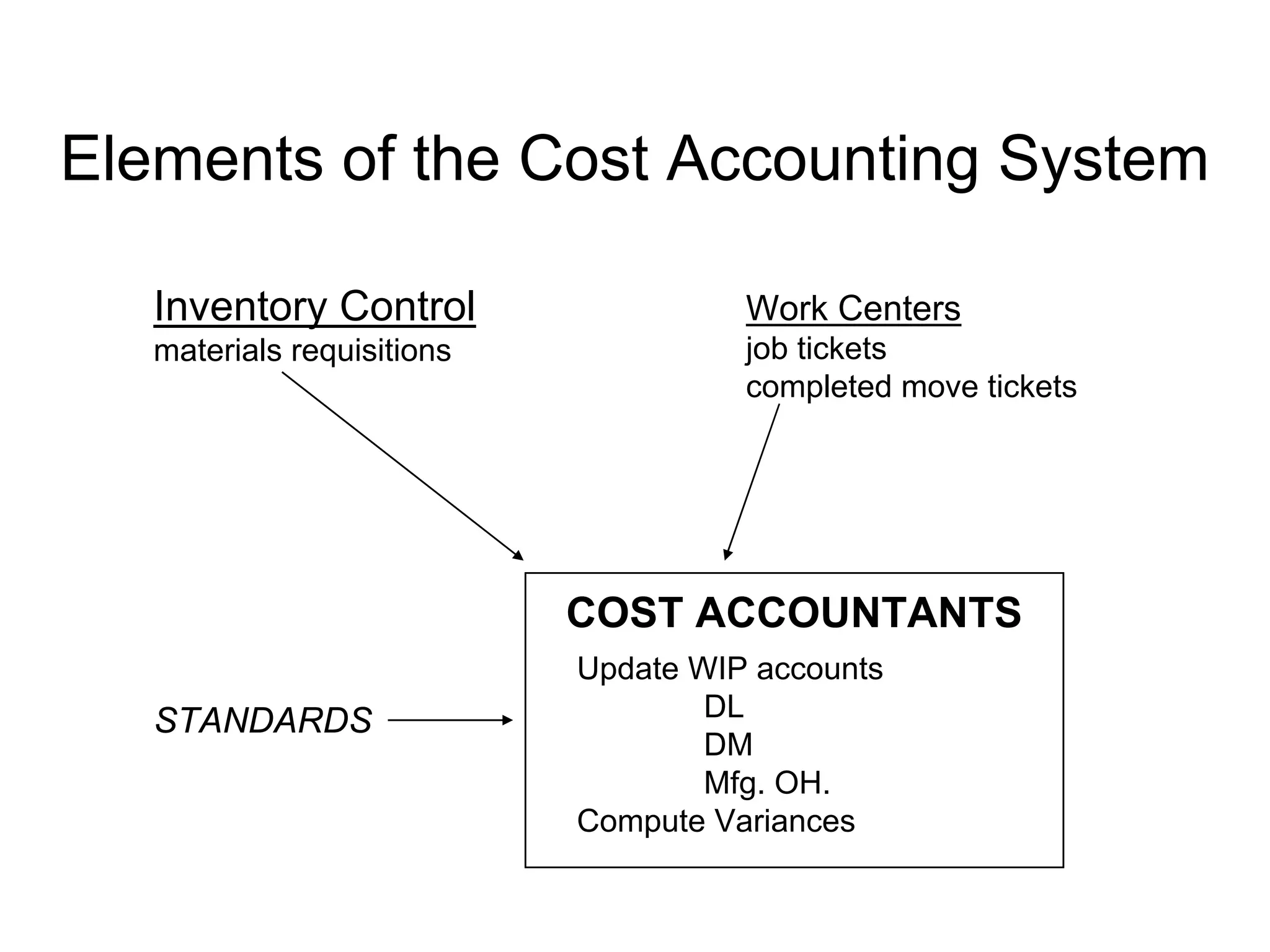

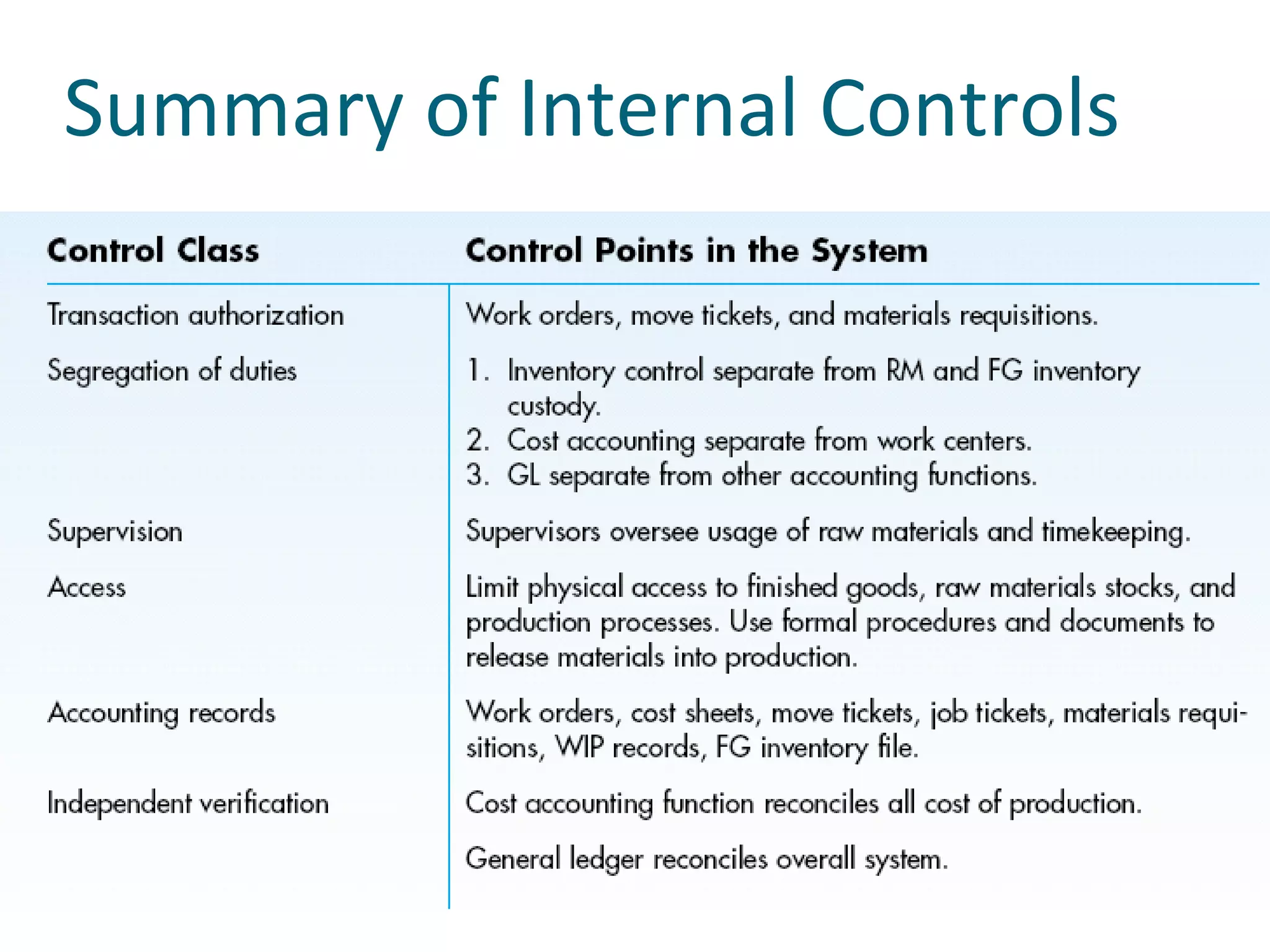

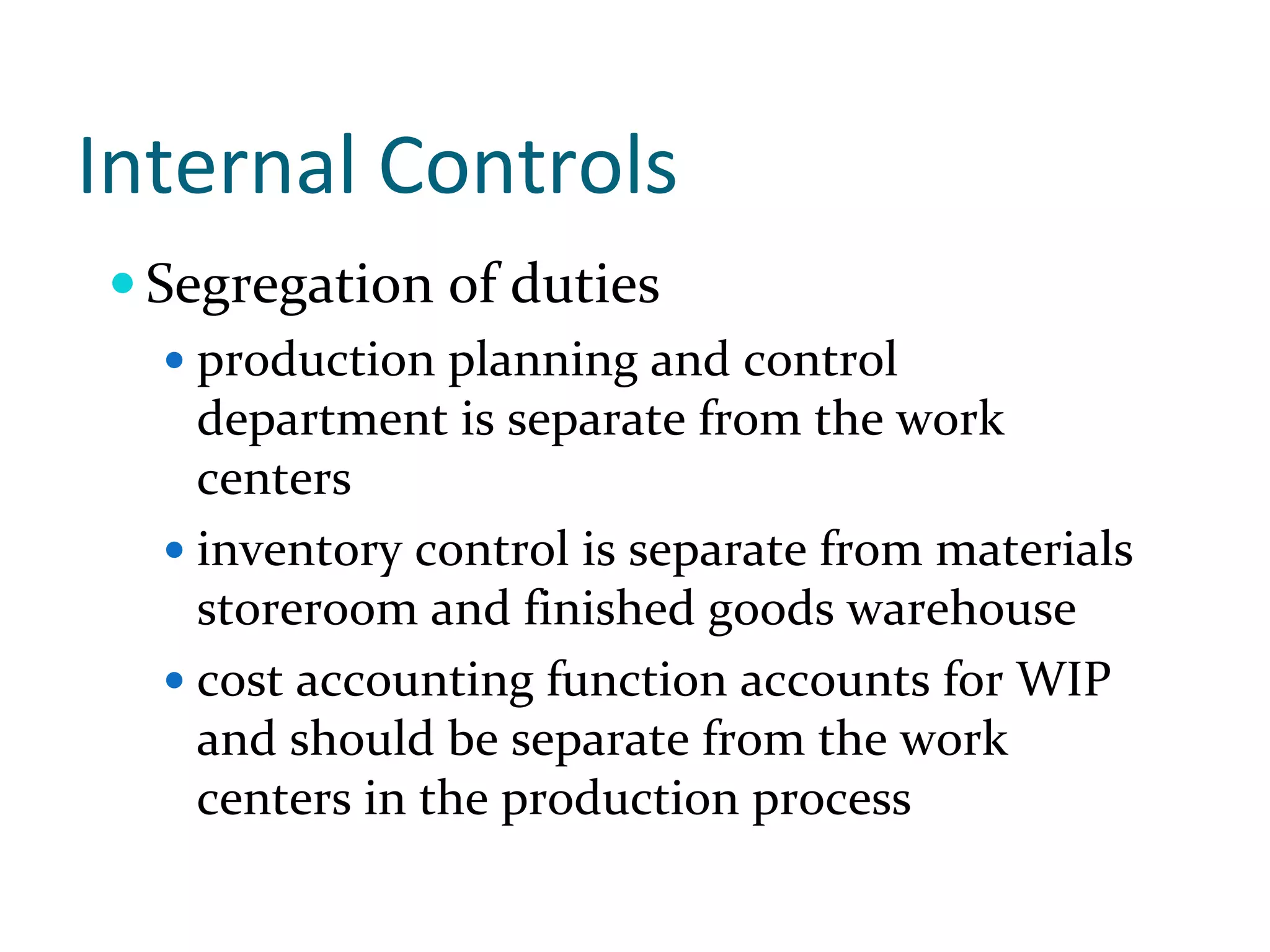

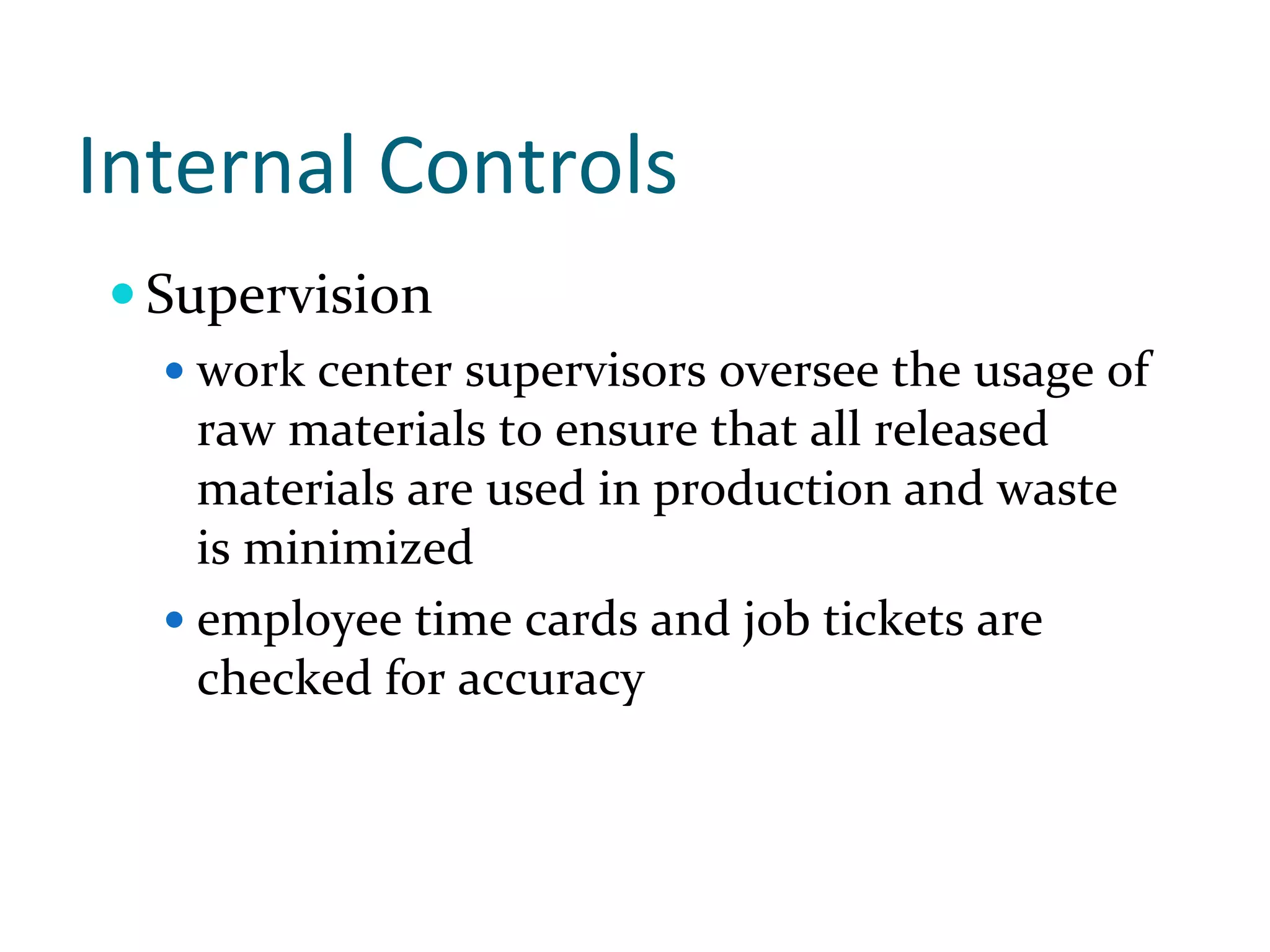

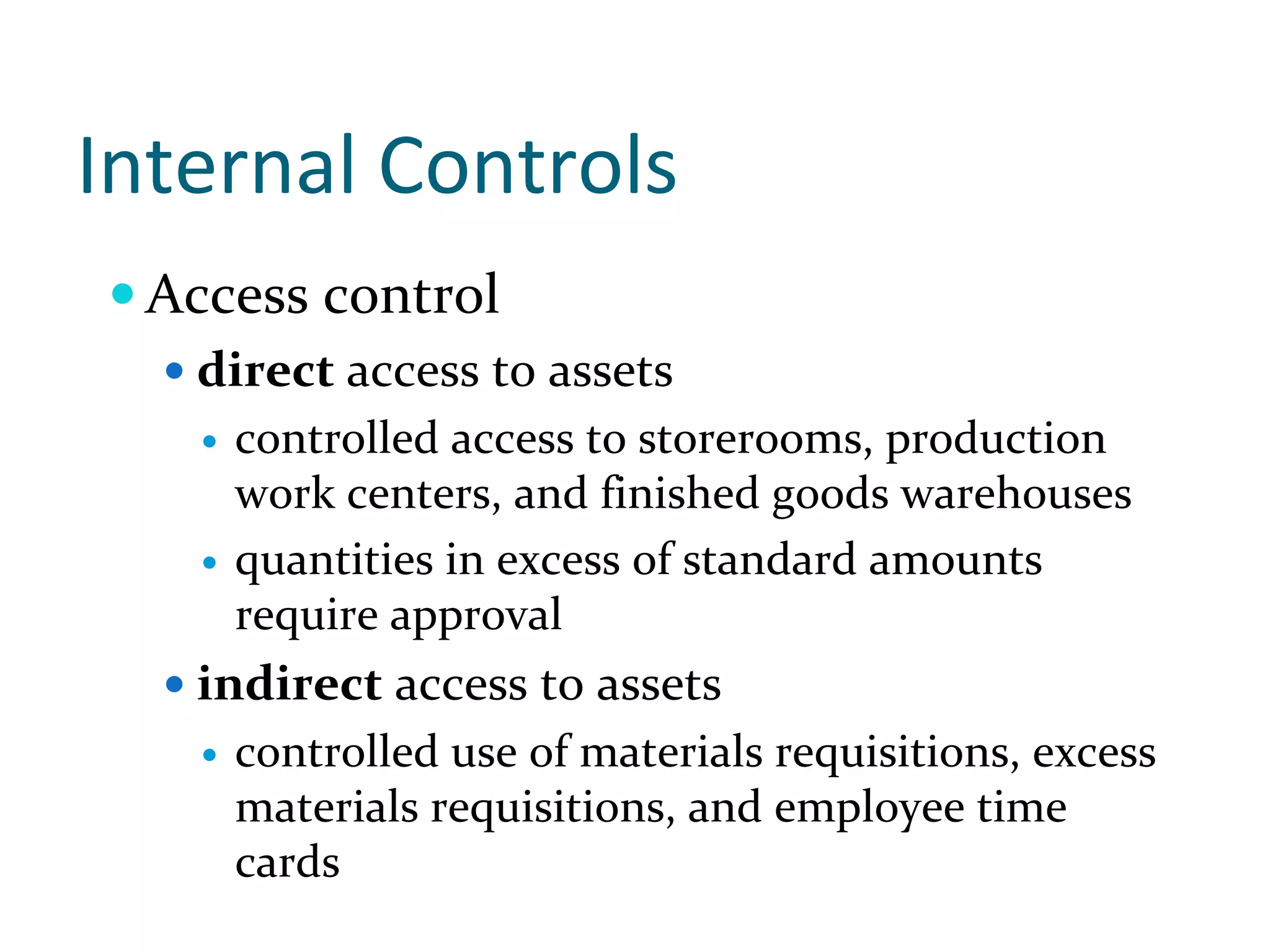

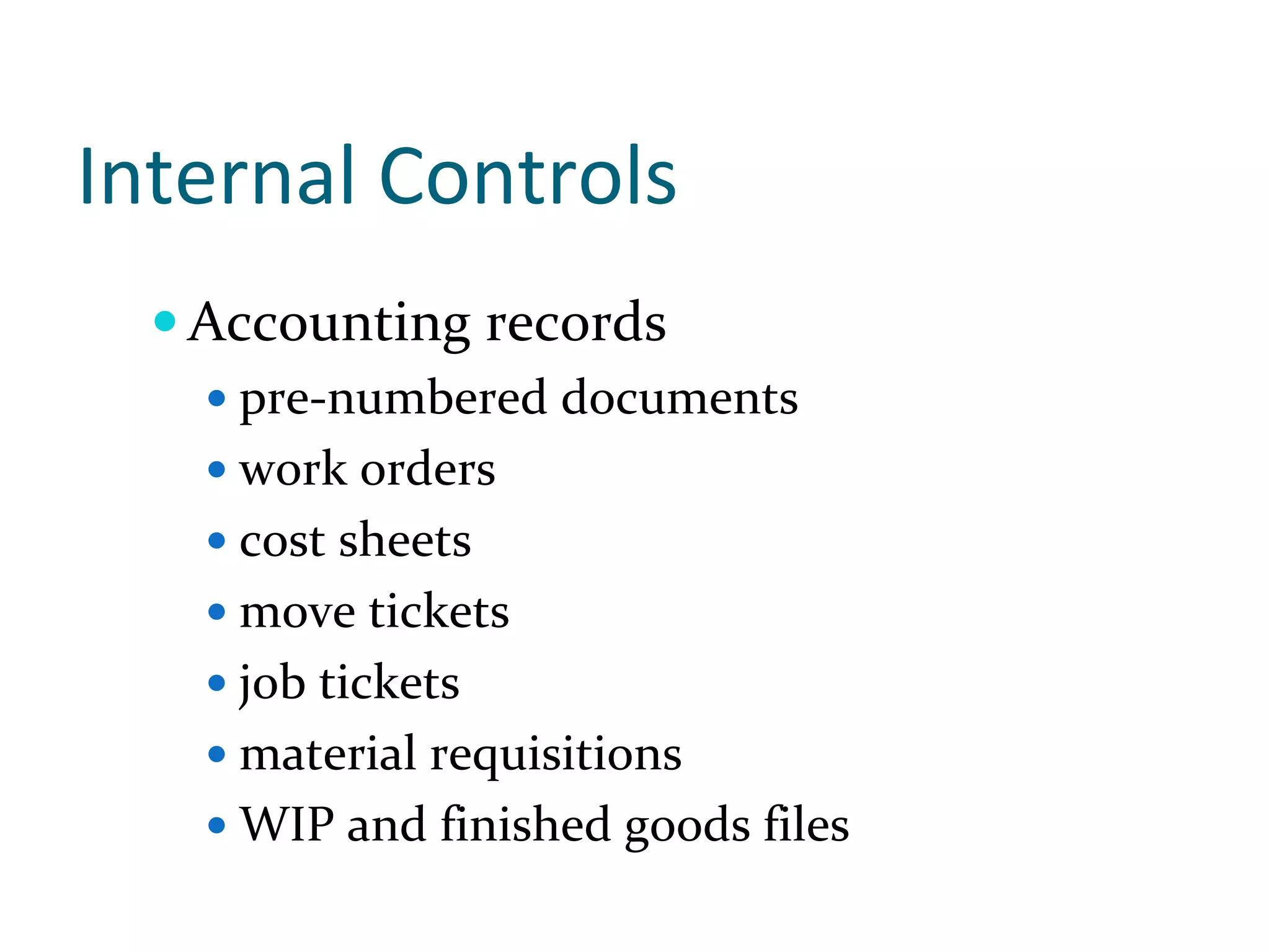

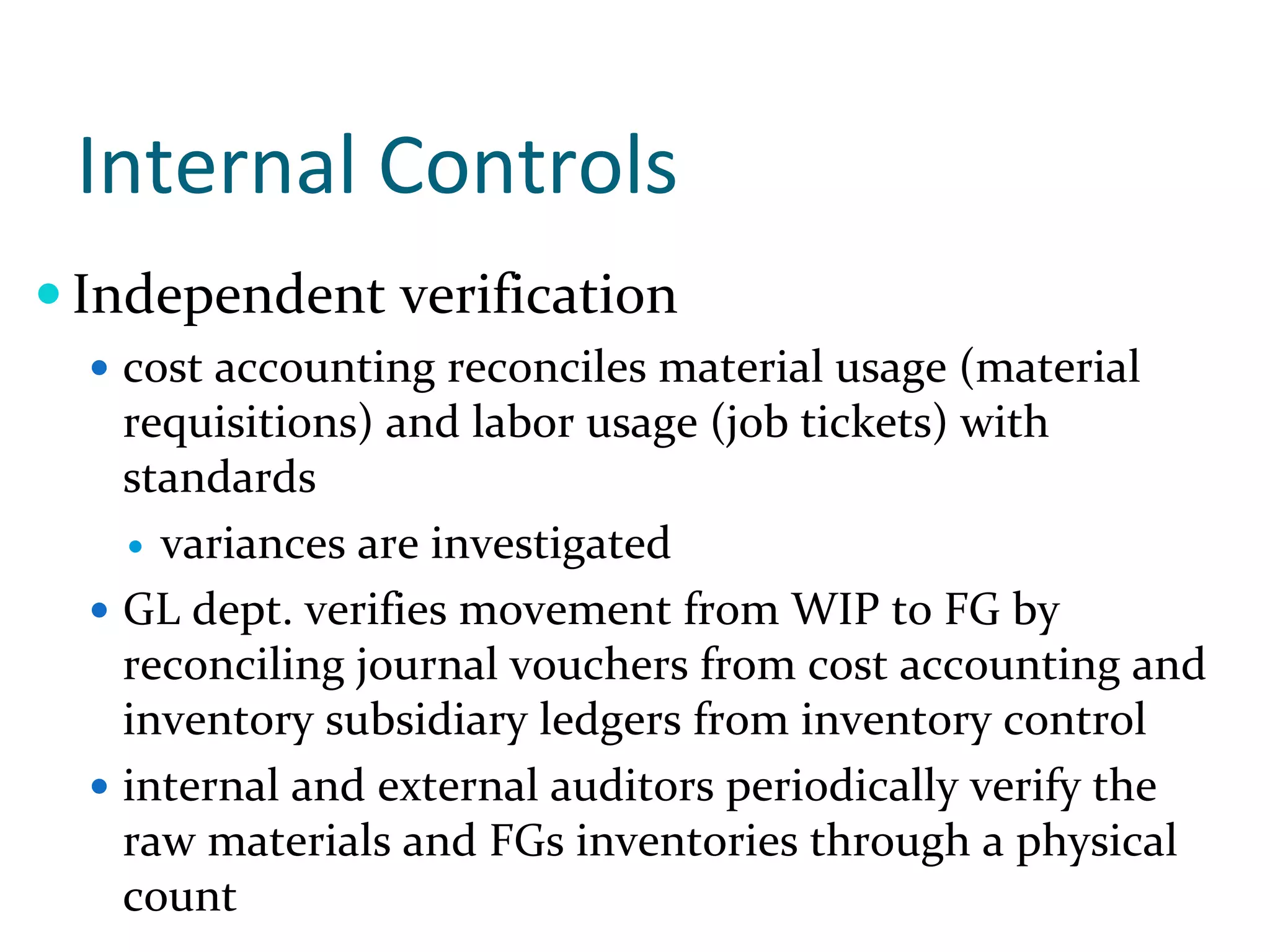

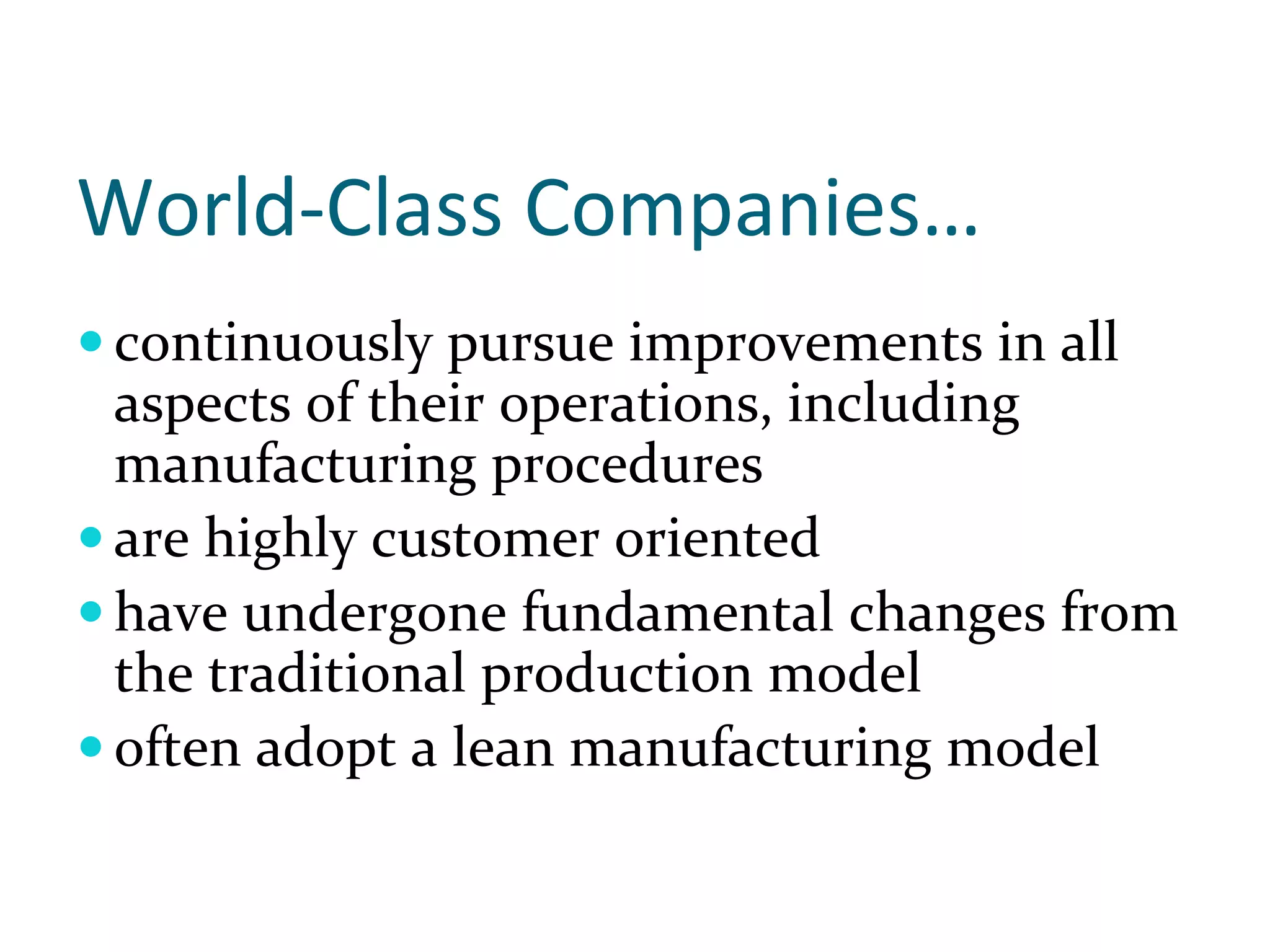

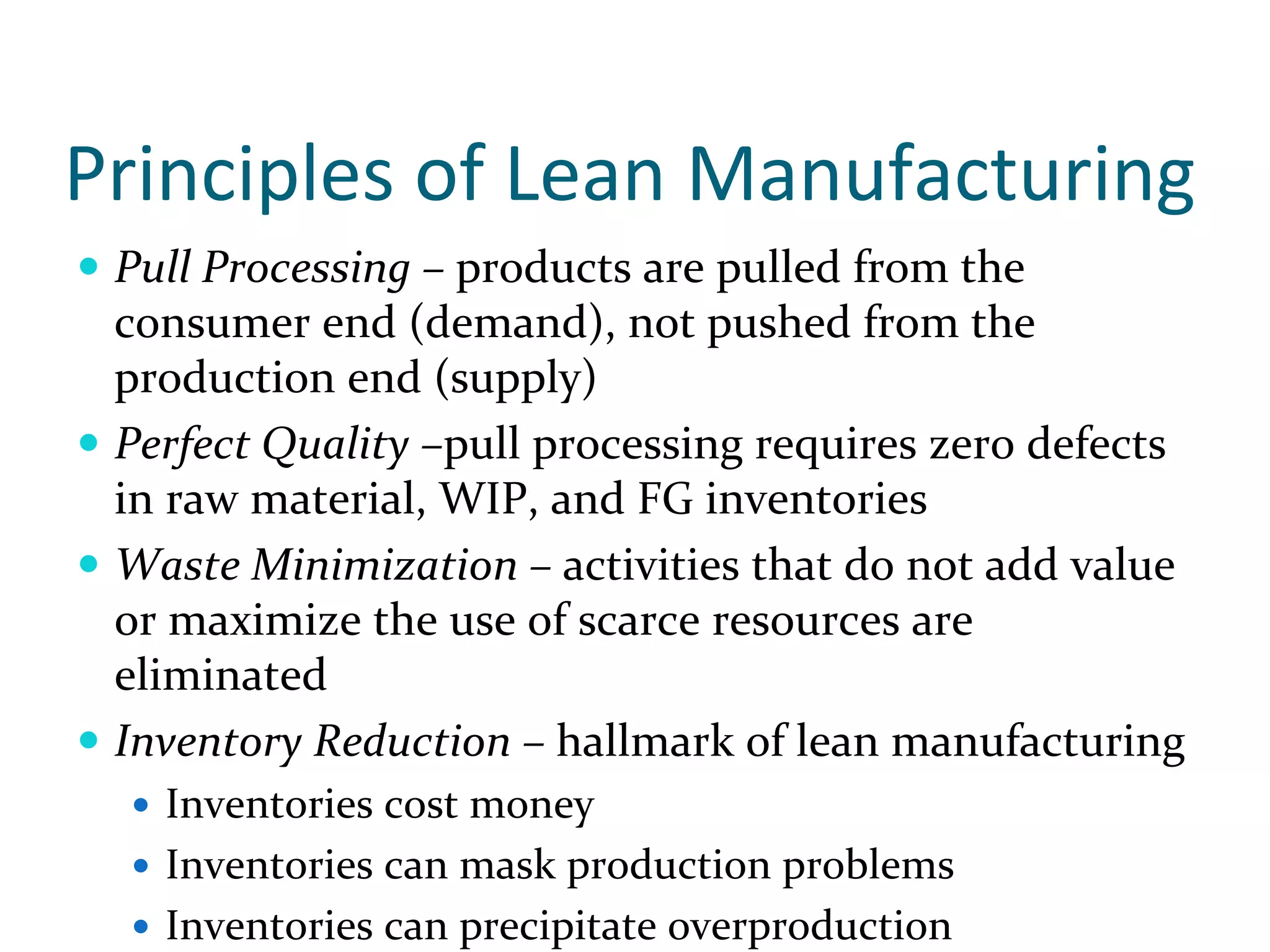

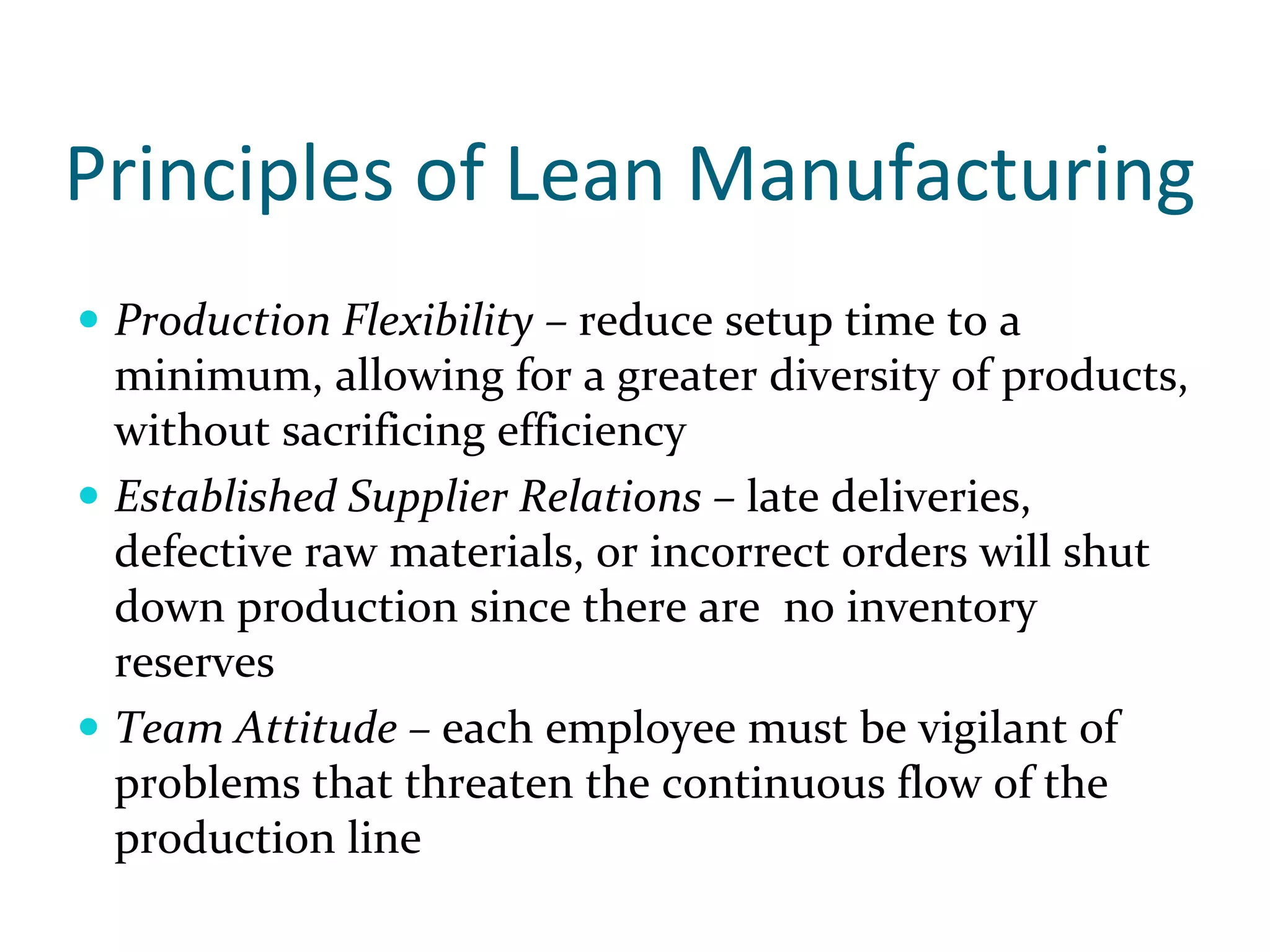

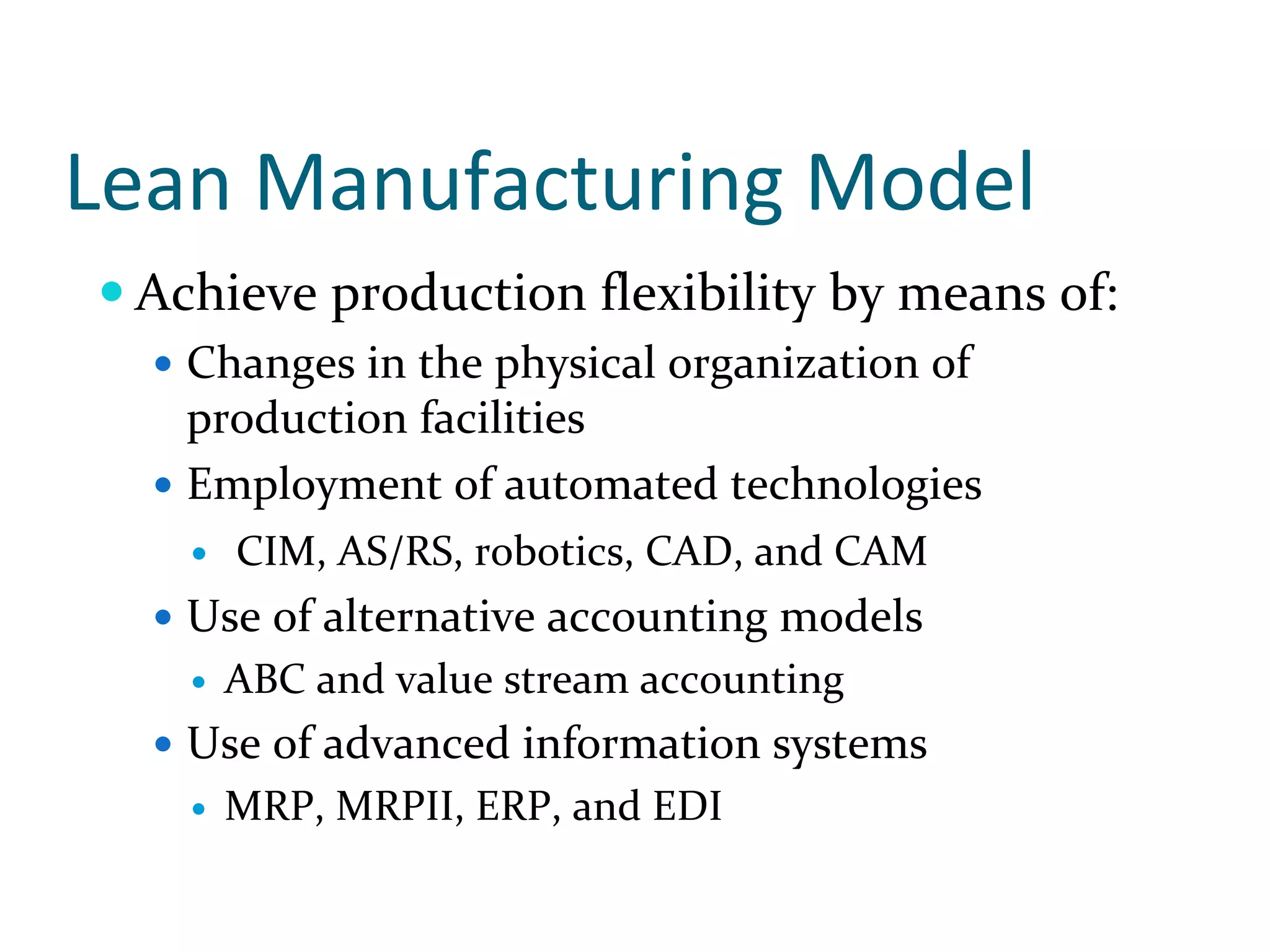

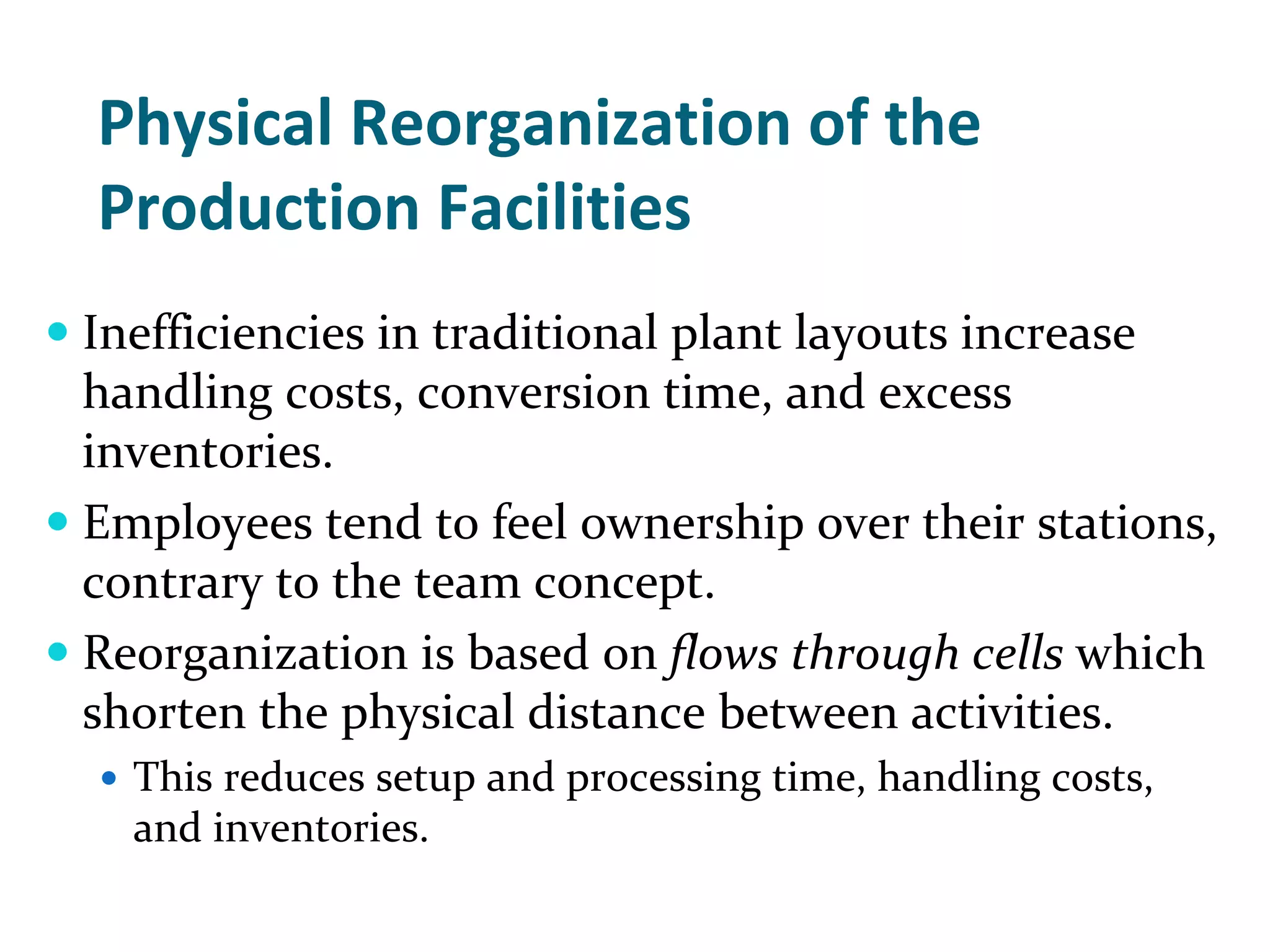

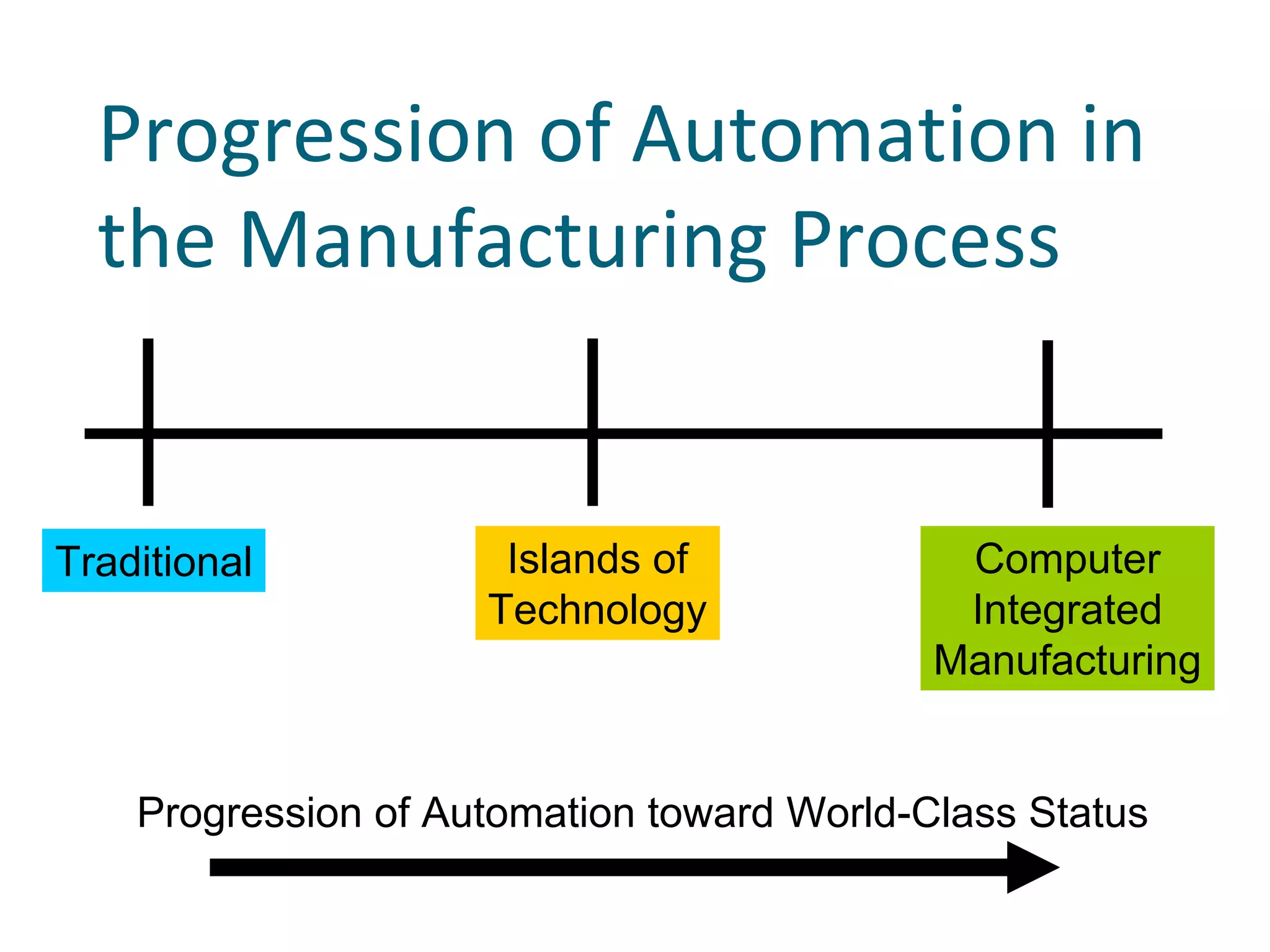

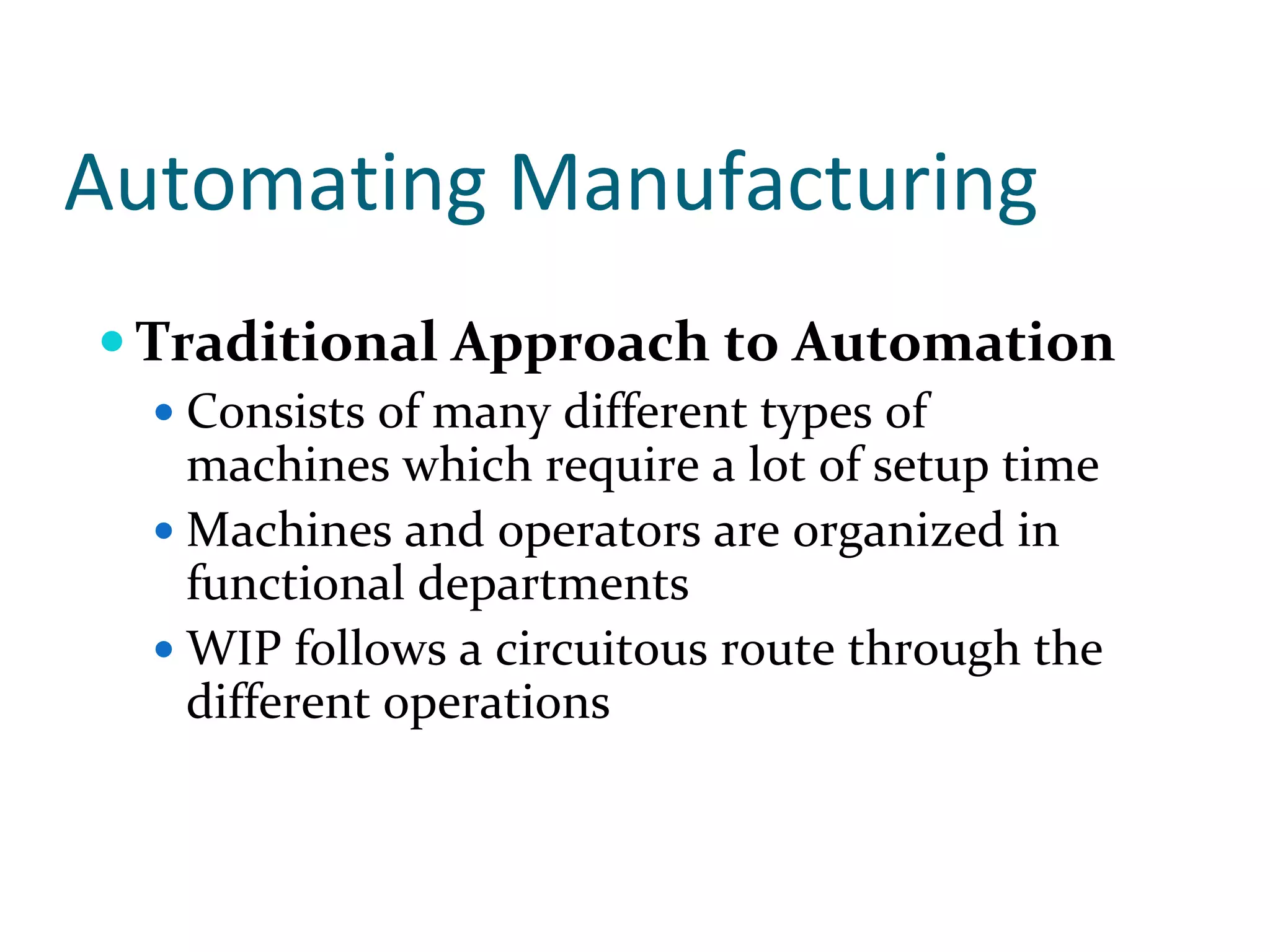

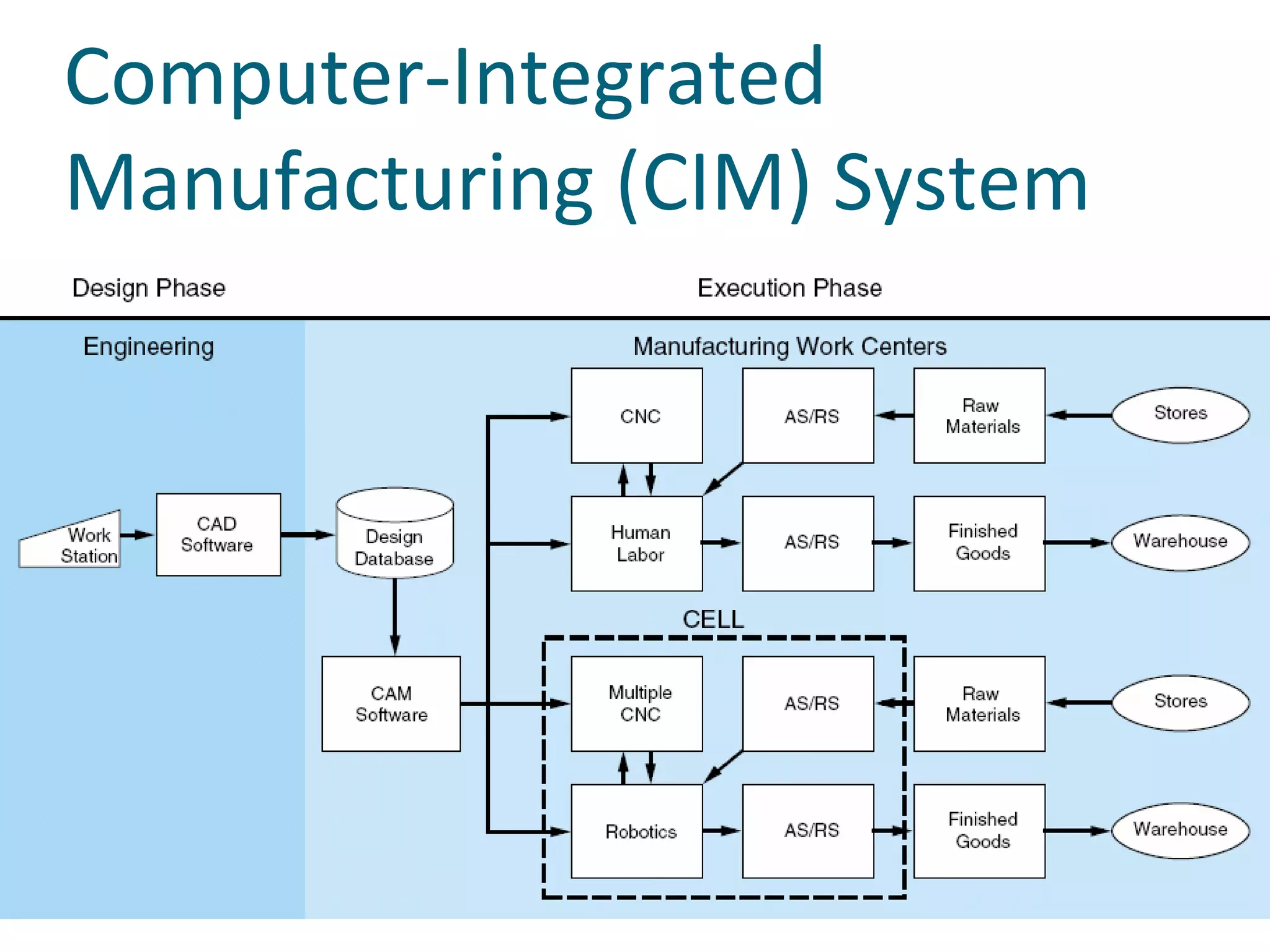

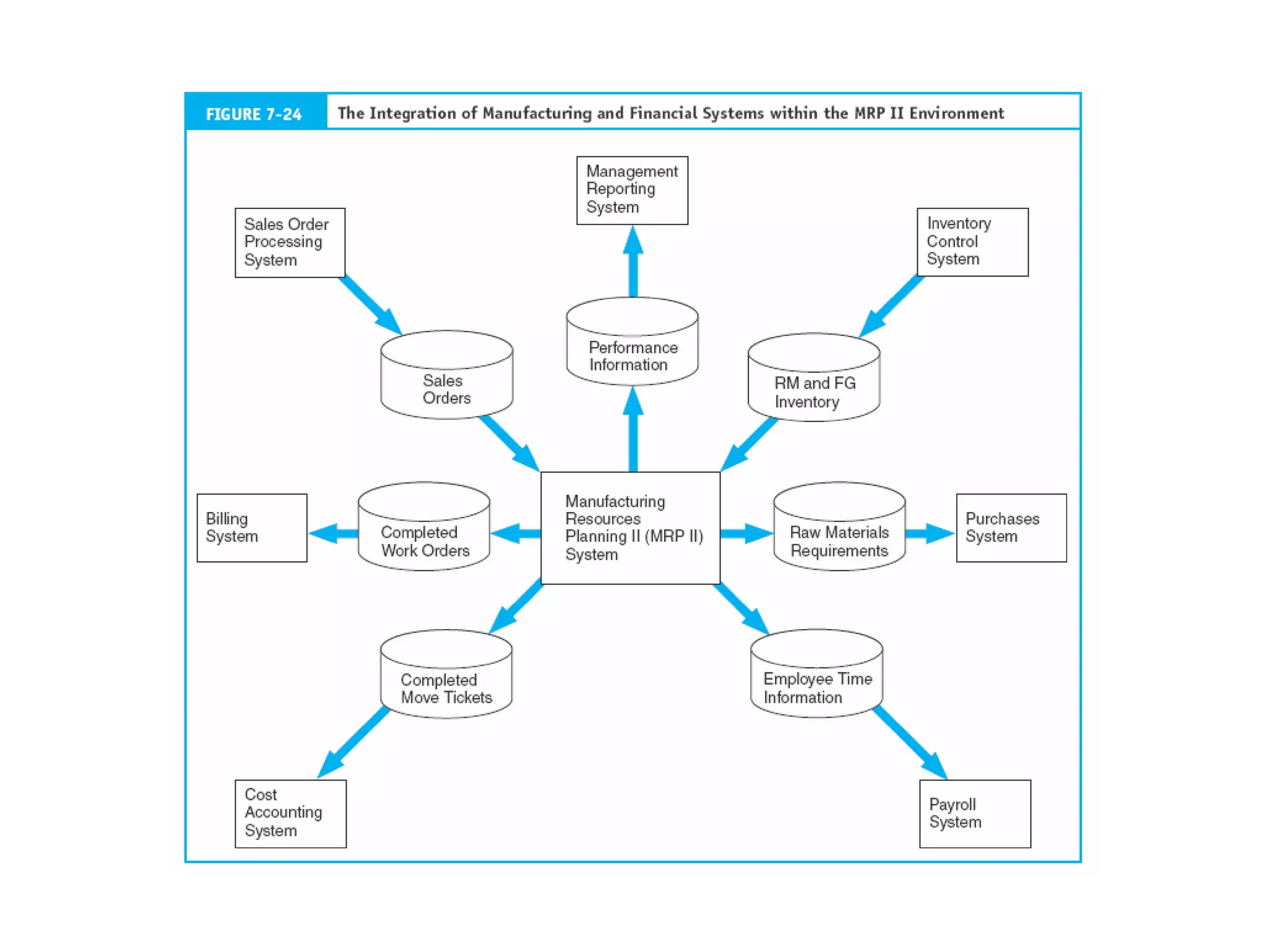

The document discusses elements of traditional batch production systems and cost accounting methods, as well as how lean manufacturing principles have transformed production models. It describes the key processes in traditional batch production, including production planning and control, physical production operations, inventory control, and cost accounting. It then outlines principles of lean manufacturing such as pull processing, perfect quality, and waste minimization. Lean manufacturing aims for continuous production flexibility through techniques like cellular layouts, automation technologies, and advanced information systems.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)