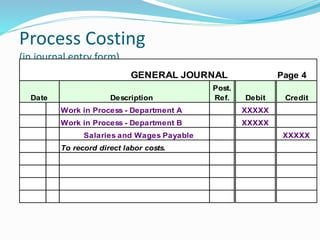

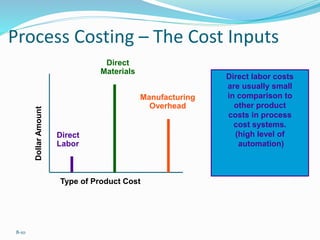

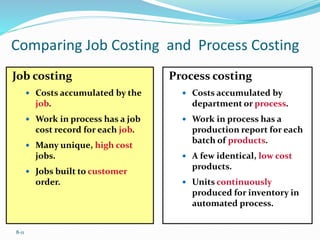

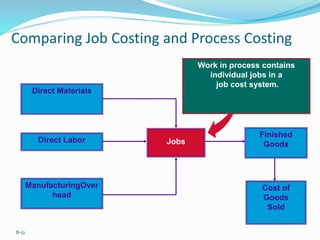

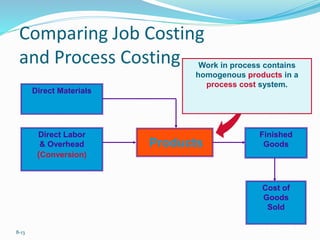

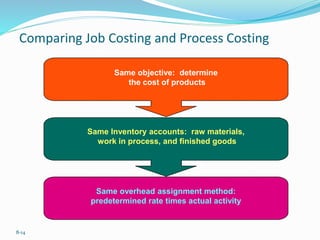

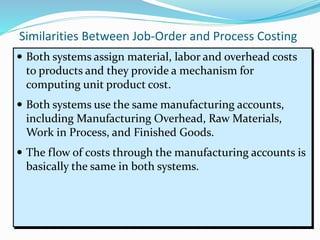

The document discusses different cost accumulation systems used in accounting, including job order costing and process costing. It explains that job order costing tracks costs for individual jobs or orders, while process costing accumulates average costs for batches of homogeneous products. The key differences and similarities between the two systems are outlined.